Pension performance update: October 2022

What happened to pensions in October? Read our summary of investment markets across the globe and what it means for your savings.

Murray Humphrey

1 November 2022

7 min read

For many savers, October offered some green shoots of recovery in investment markets. Thanks to companies sharing better-than-expected earnings and more clarity on the economy’s future, equity investment markets rose on the whole for the first time in months. Here’s what happened to pensions in October.

We’ll start with an overview of how stock markets performed on the whole in the US and UK.

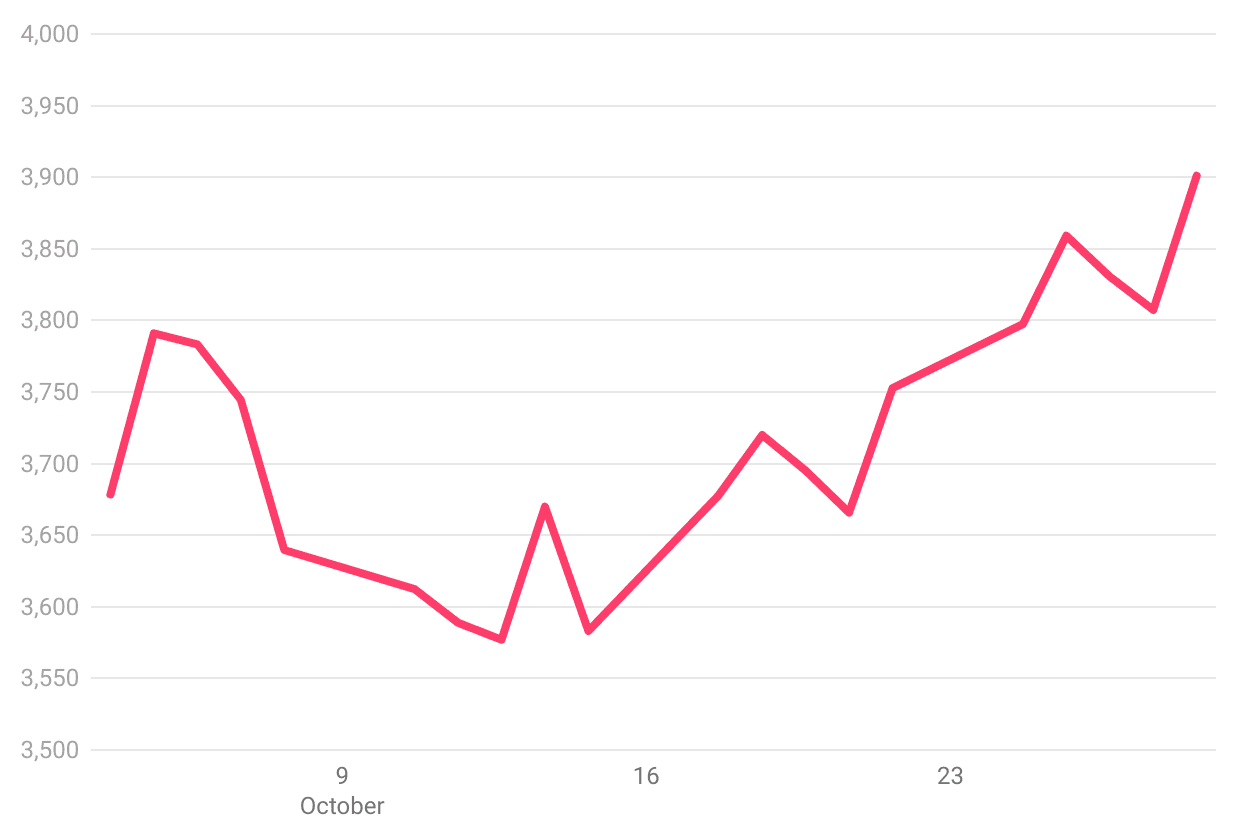

In October, the S&P 500, an index combining the value of the 500 most valuable companies in the US, grew by 6%. The S&P 500 is still down nearly 19% since the start of 2022.

Source: Google

As a large portion of our pension plans invest in North American companies, the S&P 500 provides a fairly reliable indication of how our plans have performed. Of course, it’s worth remembering that all of Penfold’s plans are diversified - to help protect our savers from market falls as much as possible. Your pension also invests in different commodities all over the globe, meaning the price of the S&P 500 won’t necessarily be a 1-to-1 correlation with your pension’s value.

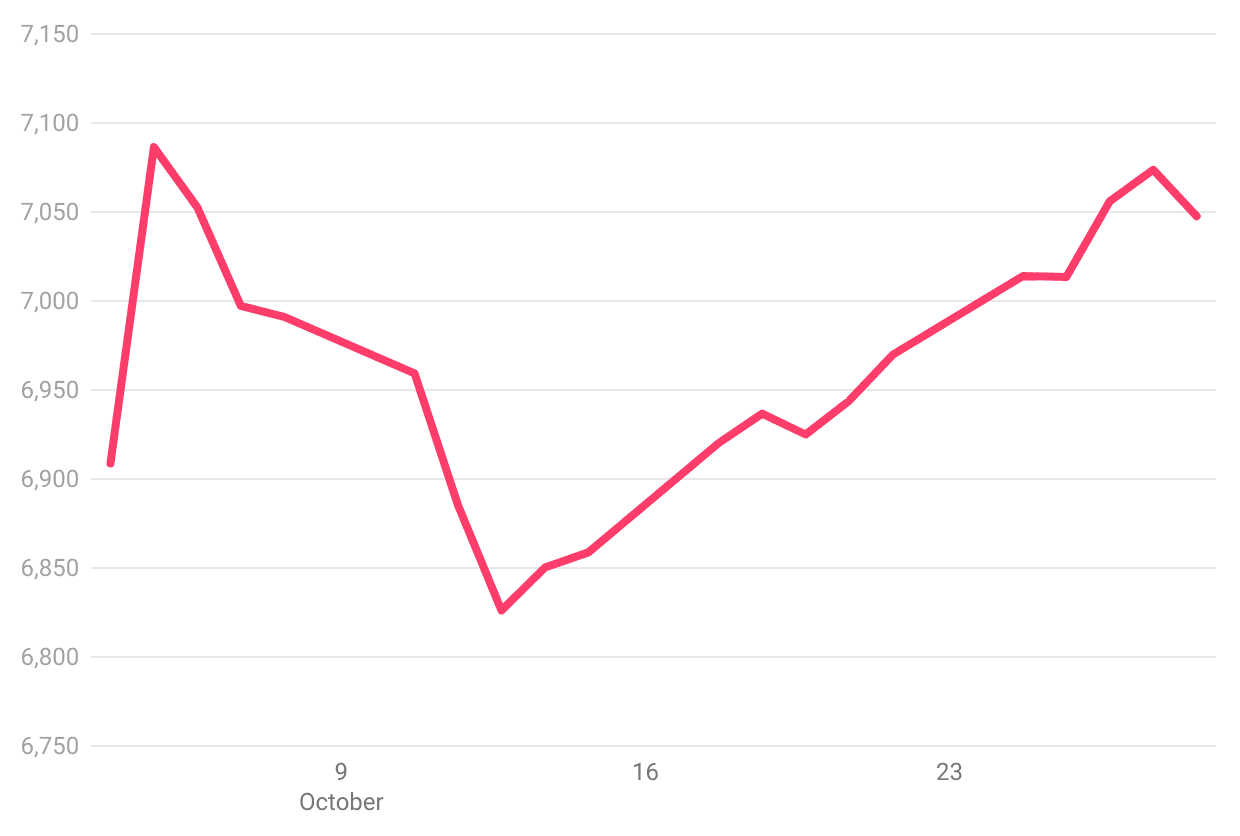

The FTSE 100, (the top 100 companies in the UK) rose by 2% from the start of the month - highlighting how much the UK is lagging behind North American markets. The UK’s major index is down 6% over the year.

Source: Google

Only 3.75%-12.5% of Penfold’s plans are made up of UK equities (depending on the plan you picked), so the FTSE’s value has less of a substantial impact on your pension’s performance.

Next, we’ll look at the underlying issues impacting investments last month.

While October did see some relief for savers, the broad trends of the year haven’t gone away. Inflation is still very high (currently 10.1% in the UK) meaning the cost of everyday goods and services is going up. Central banks across the US and Europe continue to try to stop price rises via their main inflation-fighting tool - the bank rate. At the end of October, the Bank of England increased the bank rate again to 3% - the biggest single rise since 1989 with further rises possible in 2023. The Monetary Policy Committee also warned the UK could be facing the “longest recession ever” as the fight to curb inflation goes the distance.

This month the Bank of England increased the base rate to 3% - the biggest single rise since 1989.

As we touched on, much of Penfold savers’ pension growth hinges on stock performance in North America. The story in the US remains largely unchanged. The Fed (the United States central bank) is still fighting inflation with another rate hike of 0.75%, taking their bank rate to 4%. This is the highest the central bank rate has been since 2008.

However, it’s worth knowing that the situation does seem more positive in America compared to the UK at the moment. Many US companies posted better earnings than expected in October and there also appears to be some sentiment that in the future, bank rates will rise at a lower rate.

As we covered in a previous update, increasing central interest rates tend to have a negative impact on stock markets:

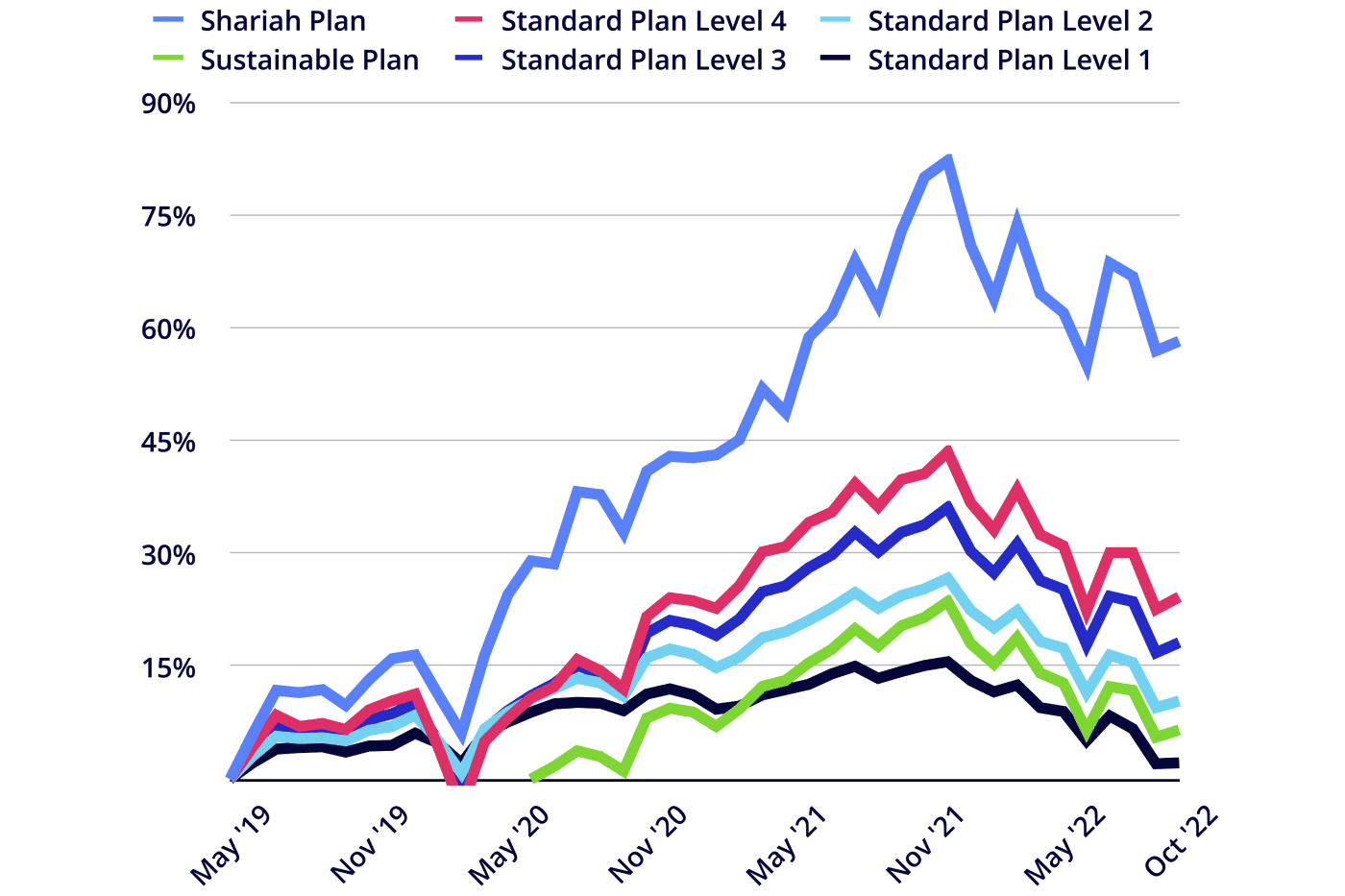

On the whole, Penfold’s pension plans were up in October, fuelled by a small rally in global stock markets.

Source: BlackRock & HSBC

Everything you pay into your Penfold pension is invested into a pension fund - a basket of different assets like stocks, bonds and more. What exactly is in your pension fund depends on your chosen plan. ‘Higher risk’ plans have a larger allocation to more volatile investments like company stocks.

Our investment strategy means that our fund managers are constantly reacting to market trends and tweaking where your pension contributions seeking to:

Over the long term, pensions still offer a fantastic way for savers to grow wealth. In fact, investing when markets are down can offer savers better value for money, as you’re paying less for that company stock than you would’ve done a few months ago.

Savers can also benefit from something called pound cost averaging. Essentially, investing regularly rather than trying to “time” the markets helps bring the average price you pay down. No more worrying about when’s the best time to ‘buy-in’.

For example, let’s say you have £3 to invest. You could buy 3 shares at once for £1 each or, you could spread out your investment to help your money go further if there is a dip in the market. Buying those same shares over a 3-month period for £1, 80p and then £1 means on average, you’ve paid 93p per share. You’ve got the same investment for 7p less.

Don’t let the headlines panic you - your pension is normally a very long-term investment, designed to ride out market dips and deliver real, inflation-beating returns in the future.

While it can be alarming to see your pension value drop, remember investing is a big part of why your pot has grown in the past.

Market downturns can be a tricky time for those looking to retire and start using their pension. If you’re starting to think about retirement, you can still access your pension from 55 - but you may notice that the value of your pot has dipped a little recently.

While market downturns are a normal and expected part of the investor journey, it can be frustrating to see your savings decrease at the time you need them. Remember, part of the reason your pot is the size it is today is investment growth. If you’ve been saving into your pension for a long time, chances are you’ve still made a healthy return.

If you’re concerned about your pension, here are a few things you may want to consider:

Hopefully, you have a long and happy retirement ahead of you. Being careful with the way you access your money today can help your money go further tomorrow. If you’re concerned about accessing your pension, we recommend speaking to a financial advisor or contacting Money Helper, a government-backed service for free, unbiased advice on your options.

October bucked recent trends and saw a small rally in stock markets. A few positive company quarterly earnings updates alongside a wider coming to terms with anti-inflation measures meant investors felt a little more confident in the markets.

While these are difficult times for pension savers and all investors, try to remember that global market downturns have happened before - and bounced back. In every bear market (period of economic decline) in history, investment markets have recovered and come back even stronger.

For more peace of mind, check out our recent blogs on what happened to pension funds following the mini-budget and what to do if the value of your pension pot is down.

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.