Pension performance update: September 2022

What happened to pensions in September? Read our summary of investment markets across the globe and what it means for your savings.

Murray Humphrey

3 October 2022

6 min read

September was another volatile month for investors, with stocks and bonds rallying early on, only to fall again as October arrived. As with last month’s update, global economies continued their fight against inflation. Central banks were forced into a balancing act of combatting the cost of living crisis while encouraging enough growth to avoid recession.

Here’s a quick recap of what happened in September.

First, an overview of the markets in the US and UK.

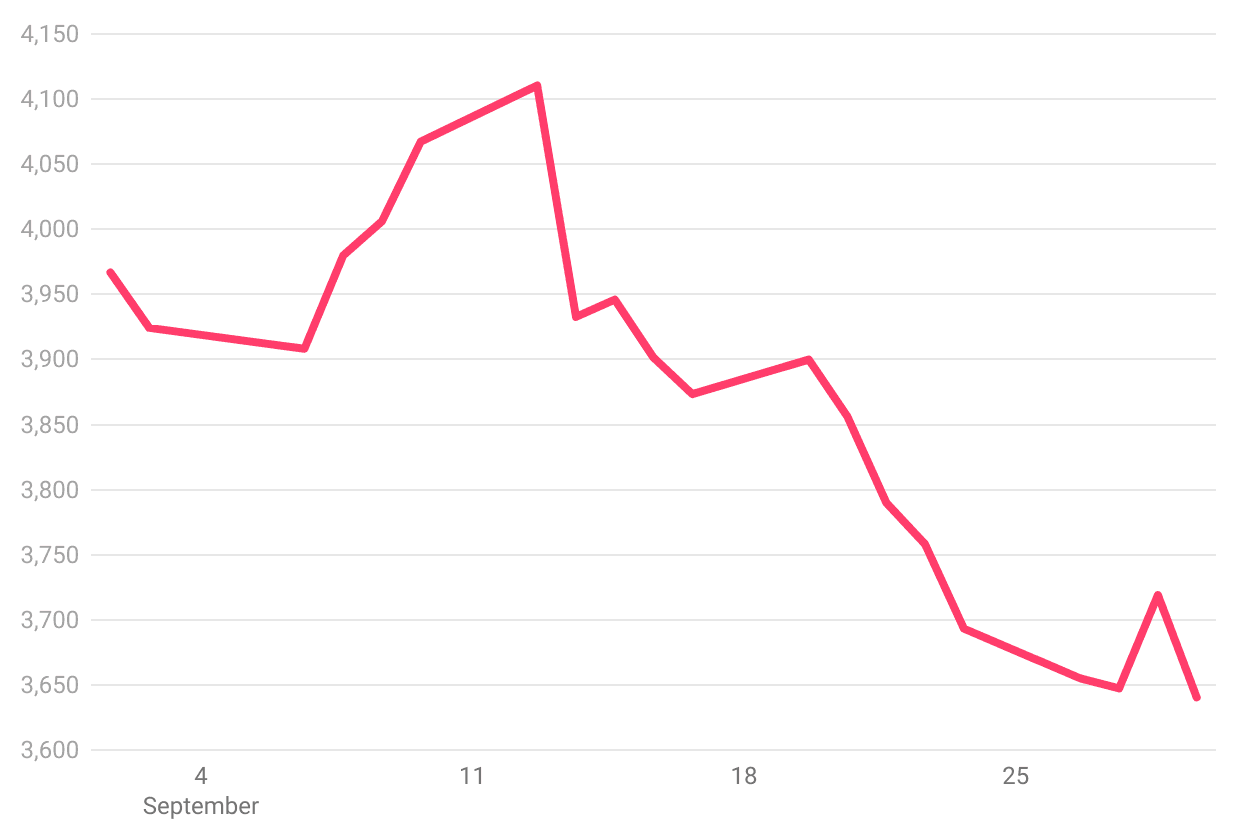

In September, the S&P 500, an index combining the value of the 500 most valuable companies in the US, declined by 8.2%.

Source: Google

The S&P 500 is now down 24% since January, hitting its lowest point of the year - the 4th time it’s set a new low this calendar year. As a large portion of our pension plans invest in North American companies, the S&P 500 provides a fairly reliable indication of how our plans have performed.

Of course, it’s worth remembering that all of Penfold’s plans are diversified - to help protect our savers from market falls as much as possible. Your pension also invests in different commodities all over the globe, meaning the price of the S&P 500 won’t necessarily be a 1-to-1 correlation with your pension’s value.

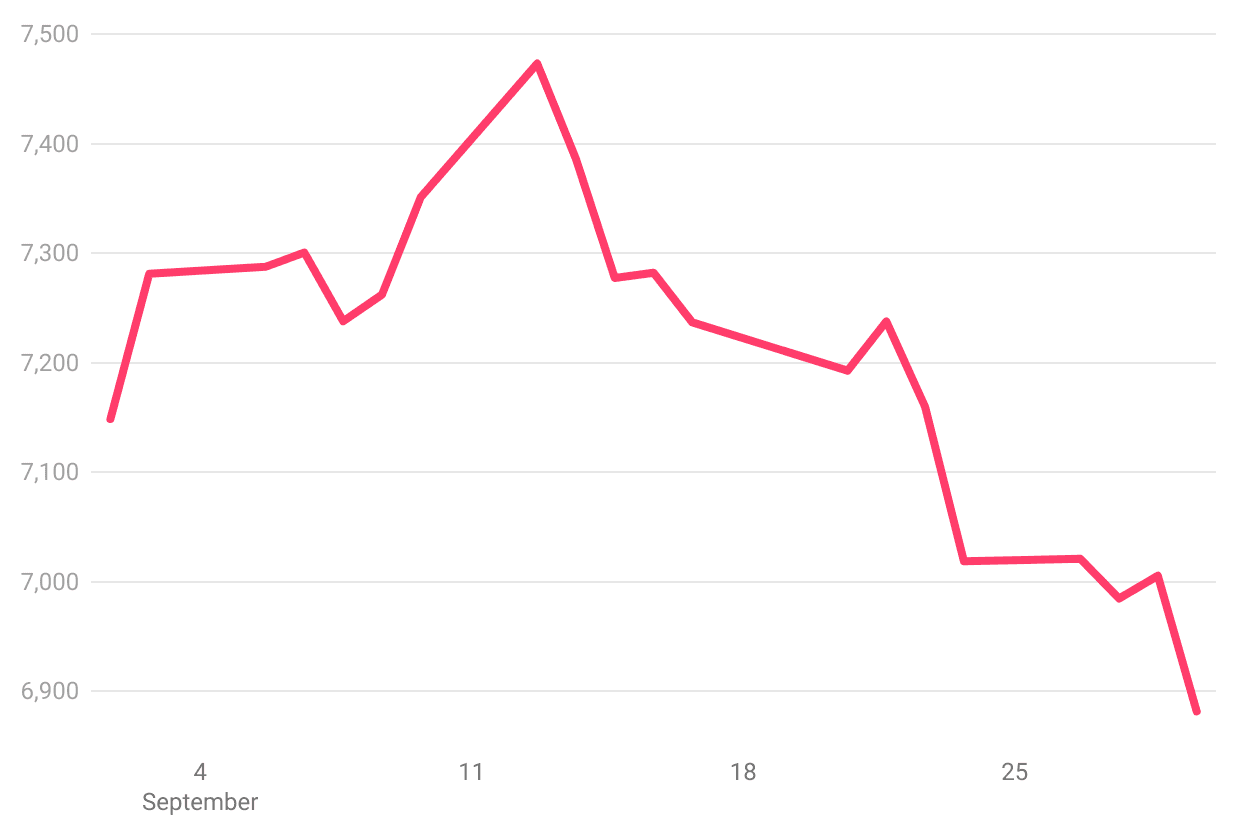

Source: Google

On home soil, the FTSE 100, (the top 100 companies in the UK) finished down again - dropping 3.7% since the start of September. The UK’s major index has now fallen 8.3% over the year.

However, as only 3.75%-12.5% of Penfold’s plans are made up of UK equities (depending on the plan you picked), the FTSE’s value has less of a substantial impact on your pension’s performance.

Next, let’s take a closer look at what happened in September and what it all means for the future. As we’ve mentioned in our last few performance updates, the main issue facing the world’s investment markets (as well as the economy as a whole) is inflation.

Base interest rates (how much central banks charge financial institutions to borrow) are up across the globe. In the US, the Fed (central bank) recently raised its rate by 0.75% in September to 3.25% - the highest it has been for 15 years. This is the 5th time the US has raised rates this year.

Unsurprisingly this saw widespread market drops with many investors selling in fear of a global recession. Check out our previous update for a breakdown of why higher rates often cause equity (stock) markets to drop in value.

Conversely, the value of US government bonds rose, as savers looked for ‘safe haven assets’ they could rely on in times of economic uncertainty.

The UK however was a different story. As you have no doubt read, there was a major disruption to the UK economy at the end of the month in response to the ‘mini-budget’ laid out by UK chancellor Kwasi Kwarteng.

The British pound briefly dropped to its lowest level ever against the dollar, signalling investor concern about the viability of the government’s new fiscal policy. There was also a mass sell-off in UK gilts (‘IOU’s from the government to the investors).

This prompted the Bank of England to step in to help protect defined benefit pension schemes via something called Quantitative Easing - essentially, making wholesale purchases of these UK gilts to prop up their value in the short term.

Penfold, as a defined contribution scheme, relies far less on these government bonds and was largely unaffected. You can read more about this in our recent blog.

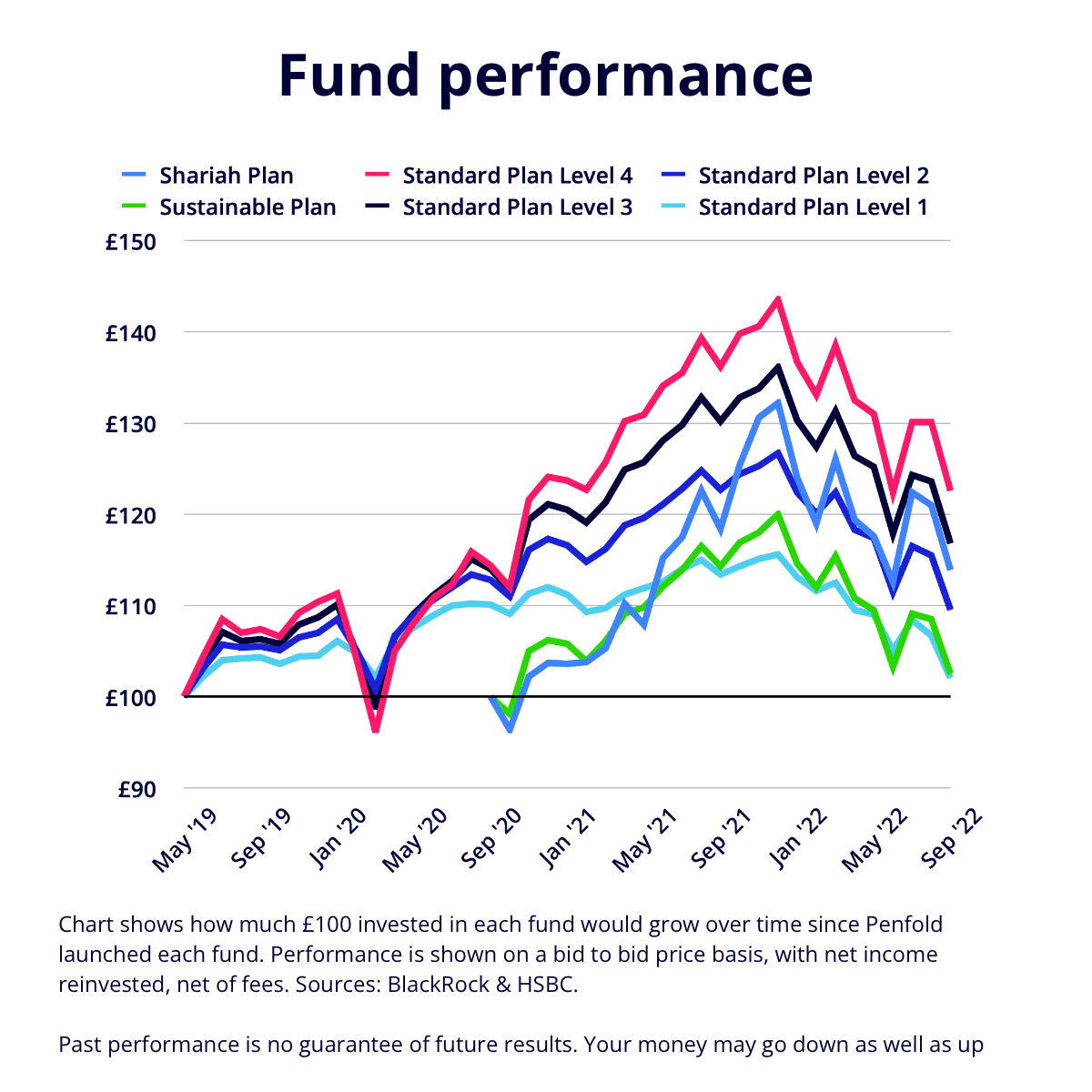

The overall trend for pension savers in September was more volatility. As a portion of your pension is invested in global stock markets (as well as government bonds), wider economic trends mean that our investment plans (like any pension plans right now) struggled this month. Here’s what it all meant for your Penfold pension in the short term.

Source: BlackRock & HSBC.

While many savers are understandably concerned about recent performance, it’s important to try to maintain perspective. As a Penfold saver, one of the consequences of making your pension more accessible via our dashboard and app is that you’re more aware of any volatility in your savings month to month.

Pension ups and downs have always been the norm but in previous years, pension savers simply wouldn’t have been aware this was happening. Extra visibility can sometimes mean we lose sight of the big picture. Just because we can see the value of our pot change day-to-day, doesn’t mean we need to change how we’re saving. Sometimes, doing nothing is the best option.

Here’s something to think about: any Penfold saver who had invested £1,000 back in May 2019 would still have made a return on their investment - despite saving through a global pandemic, energy and supply chain shortage and now a cost of living crisis. That original £1,000 would be worth around £1,230 today (minus fees).

Our investment strategy means that our fund managers are constantly reacting to market trends and tweaking where your pension contributions go to both:

September continued the recent trend of market volatility as governments tried to strike a balance between fighting inflation and a recession. While these are difficult times for pension savers and all investors, try to remember that global market downturns have happened before - and bounced back.

In every bear market (period of economic decline) in history, investment markets have recovered and come back even stronger. Over the long term, pensions still offer a fantastic way for savers to grow wealth.

In fact, investing when markets are down can offer savers better value for money, as you’re paying less for that company stock than you would’ve done a few months ago.

Savers can also benefit from something called dollar cost averaging. Essentially, investing regularly rather than trying to “time” the markets helps bring the average price you pay down. No more worrying about when’s the best time to ‘buy-in’. For example, buying a company stock 3 times for £1, 80p and then £1 means on average, you’ve paid 93p per share.

Penfold savers who are close to retirement may instead like to consider if one of our other plans (such as our Standard Level 1 or Level 2) may be more appropriate.

Don’t let the headlines panic you - your pension is a very long-term investment, designed to ride out market dips and deliver real, inflation-beating returns in the future.

For more peace of mind, check out our recent blogs on what happened to pension funds following the mini-budget and what to do if the value of your pension pot is down.

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice