Private and personal pensions for the 21st century

Welcome to a new kind of private pension. Set it up in minutes, top up or pause payments, and combine old pensions with a few quick taps. It's that simple. Leave the future to us, so you can get back to living today.

Your pension pot value can go up or down, but staying invested can help it grow

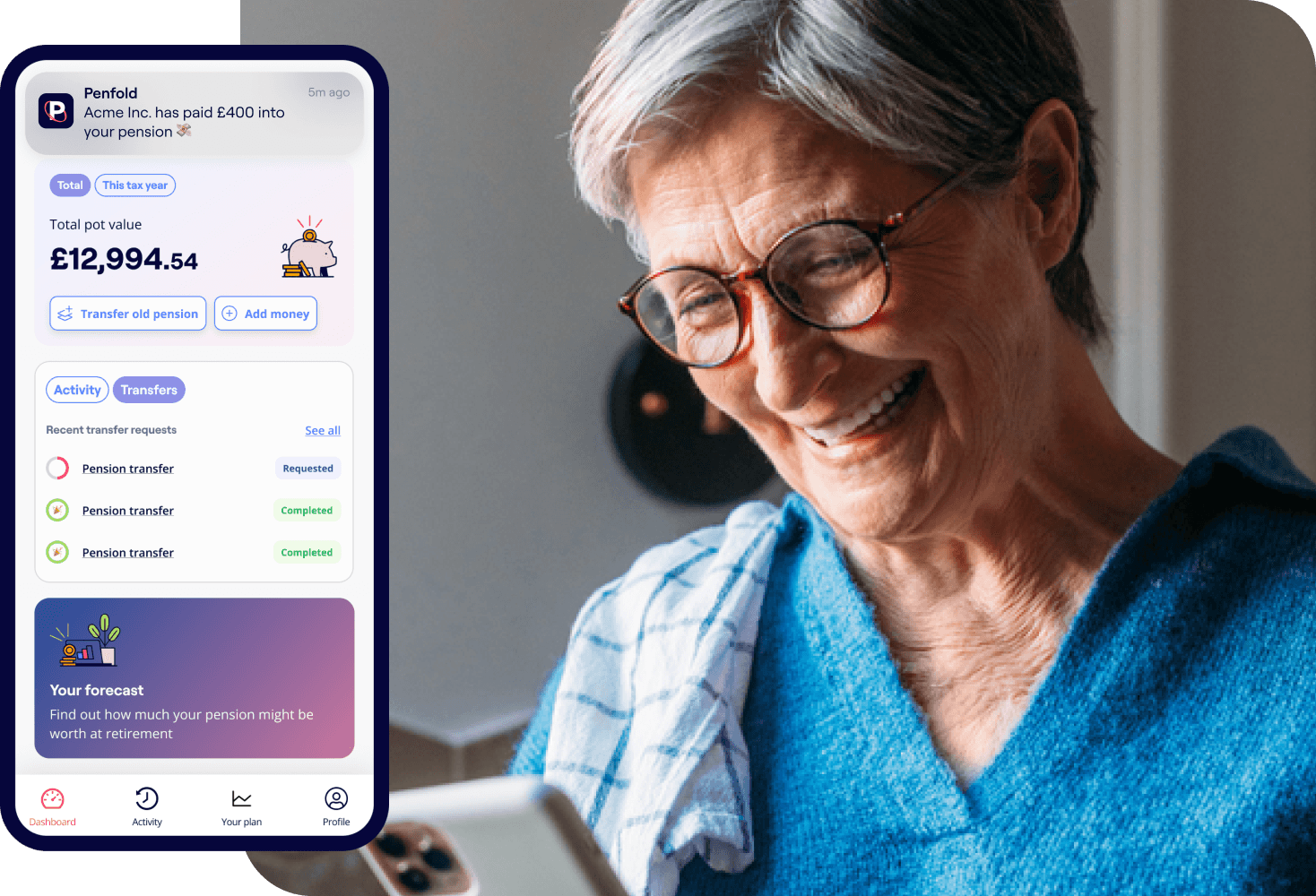

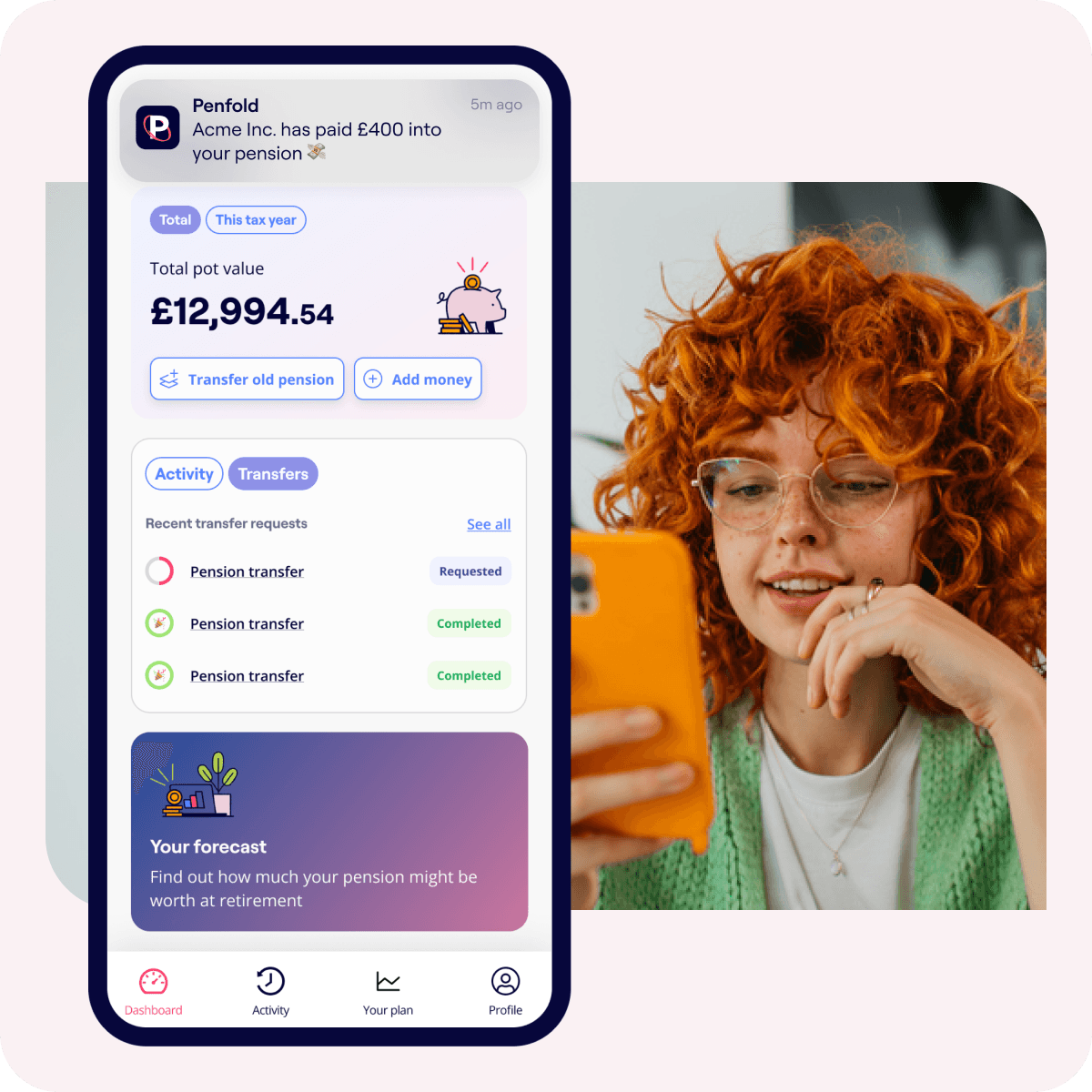

All your pensions in one place

Combining your pensions with Penfold is easy, free of charge, and our expert pension transfer team will take care of the process.

If you already have details of an old pension, you can start a Penfold pension with a transfer.

Alternatively, use our Find My Pension tool to track down the details of existing workplace pension pots. Simply enter the name of your old employer and we'll do the rest.

Save your way

Life is full of twists and turns. Penfold's private pension adjusts to all of them.

Adjust, top-up, or pause your contributions any time – instantly online or with our app.

Private pension savers receive a 25% government tax bonus on pension contributions. We'll automatically claim this and add it to your account.*

*Subject to annual allowance. Tax treatment depends on individual circumstances and may change in the future.

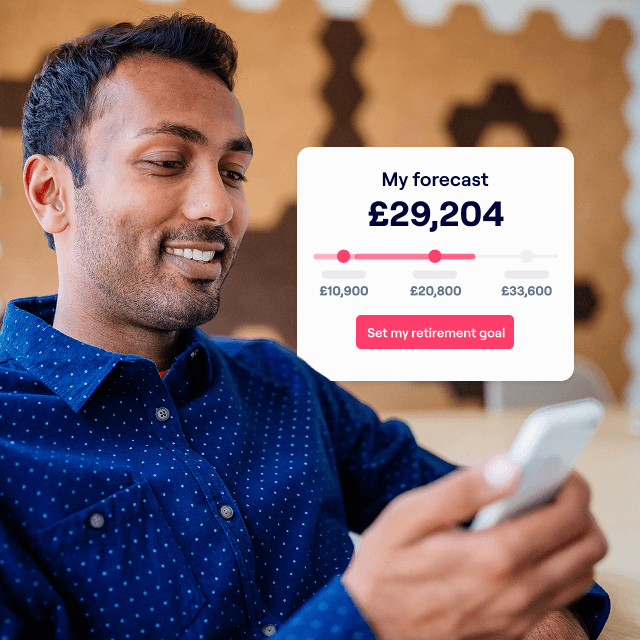

Reach your retirement goals

Not sure how much you’ll need when you stop working? Forecast your future income and get on track with your retirement goals in three simple steps:

- See your future income: Real time reporting on what your pension will be worth when you retire.

- Set goals: Use in-app tools to see how you can achieve the lifestyle and spending power you’d like

- Get on track: Use our calculator and set yearly targets to reach your retirement goal

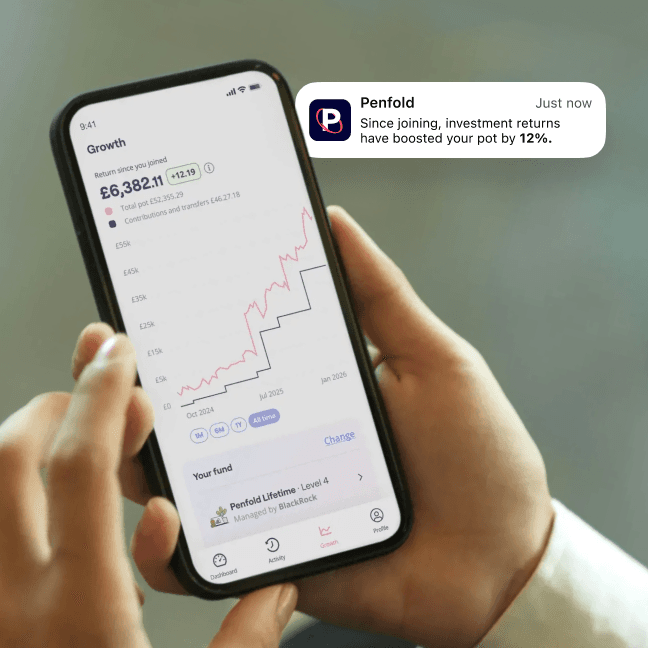

Grow your wealth

Enjoy an automatic 25% tax relief top-up every time you contribute to your private pension with Penfold. Subject to annual allowance. Tax treatment depends on individual circumstances and may change in the future.

If you’re self-employed or a director of a limited company you can make tax-efficient contributions through your business bank account.

Our plans aim to balance risk control with good returns, at a cost-effective price. We also give full visibility into your pension with a live view of how your pension is performing.

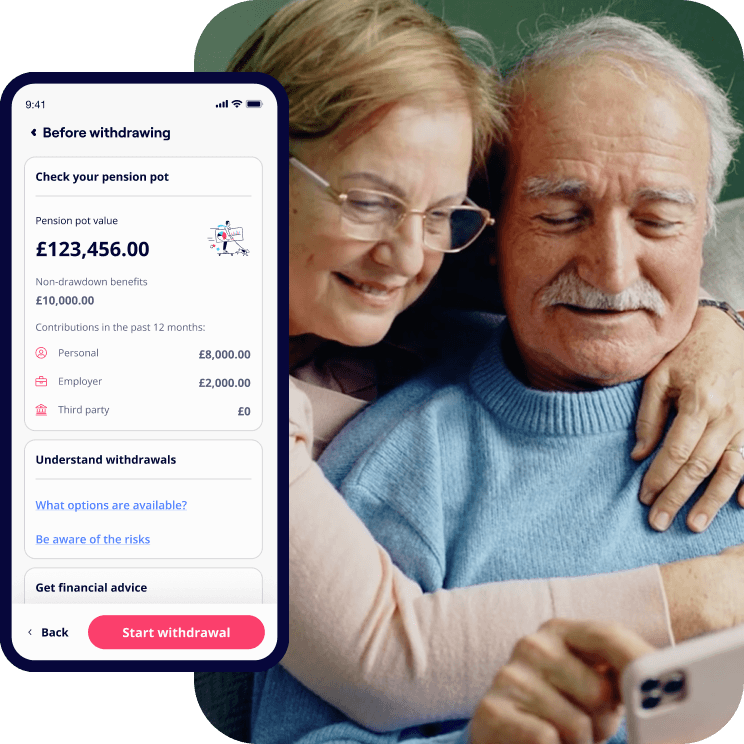

Start your retirement the right way

Penfold makes withdrawing your pension simple. Access your money however you like – choose drawdown, an annuity or even taking a lump sum in one go.

Our service is completely flexible to your needs – tweak your monthly withdrawals as often as you like, for free. There are no minimum withdrawals or restrictions on how you spend your hard-earned savings.

Our expert team are on-hand to support and help you make the right decisions for retirement. We'll guide you through the entire process, step by step.