The tax-efficient pension for directors and limited companies

Company director pension contributions can help you make the most of your 60K annual tax-free pension allowance, while your company benefits from corporation tax, NI and income tax savings.

Our limited company pension is quick to set up. And simple to use. Helping you make the most tax-efficient pension contributions, in line with your company cash flow.

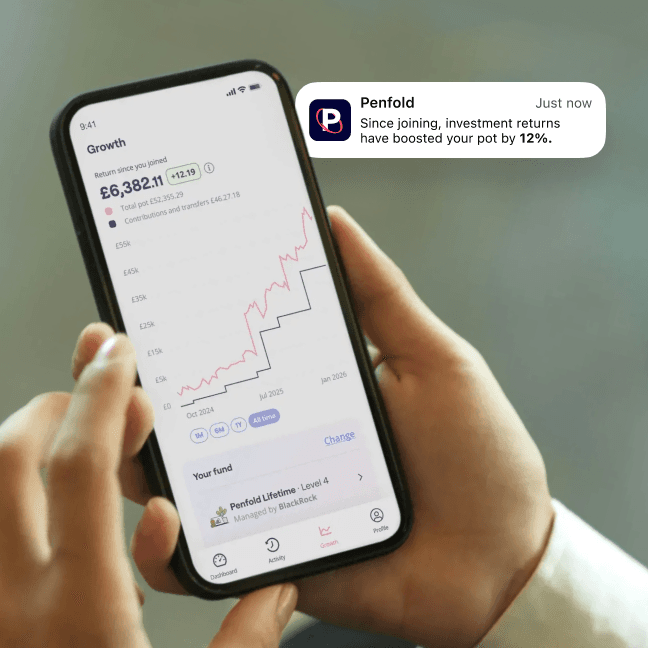

Your pension pot value can go up or down, but staying invested can help it grow

Make tax-efficient pension contributions from your limited company

Make tax-free contributions: Director pension contributions made directly from the company are tax-free.

If you're not making limited company pension contributions, you're missing out on a valuable corporation tax reducing business expense.

Reduce your corporation tax: Company pension contributions can result in a 19–25% saving on your corporation tax bill.

If your business makes a profit below £50,000, you can save the small profits rate of 19%. So every £1,000 paid into your pension cuts your corporation tax bill by £190.

Use your pension allowance: Businesses can contribute to a limited company directors' pension directly, without the 60K tax-free limit. There's no salary restriction on employer/company contributions.

Pension contributions are usually capped at £60k or the equivalent of your yearly salary (whichever is lower). But as a limited company director, your business can contribute into your pension without the upper limit.

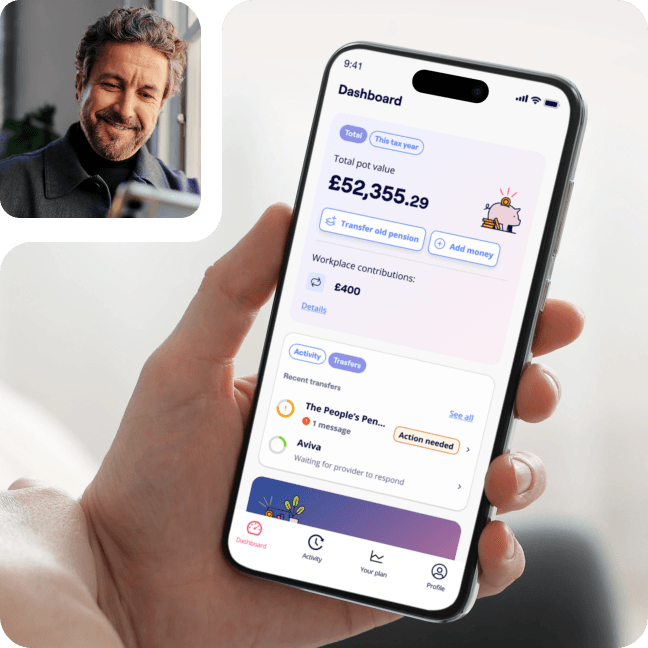

Combine your pensions with our pension transfer service

Keep all your pensions in one place. Transferring pensions to Penfold is easy, free, and managed by our expert team.

Got old pension pots? It's simple to combine your pensions. Just add your pension policy number and provider name, and our experts take care of your pension transfers.

Missing pension details? Use our Find My Pension service to find the provider and contact details. We just need the name of your previous employer to search for old pensions.

It's important to compare providers' fees and any guaranteed benefits when deciding on whether to transfer and be sure that the investments available are suitable for you. If your employer is paying into your pension currently, transferring that pot may mean you lose out on their contribution.

Friendly and expert support

Our UK-based pension experts are on hand.

We're here to support you through the life of your pension planning. From setting up tax-efficient pension schemes, end of tax-year planning and company contributions, we're here to help.

Drop us a message on chat, email or call any time. No waiting lines. No call centres.

We can even help you make pension withdrawals. Choose to drawdown, an annuity or even take a lump sum. Our experts support you as you take the decisions to plan and enjoy a happy retirement.

We've helped hundreds of company directors with their pension arrangements.

Want more information about company director pensions? Read our dedicated director pension guide.