Why Your Pension Pot Goes Up (And Sometimes Down)

Learn why your pension pot goes up and down, what it means for your savings, and why staying calm during market dips can be the smartest move.

Murray Humphrey

7 April 2025

7 min read

Ever opened your Penfold app, clocked your pension value… and done a double take?

We get it – seeing your pot change without adding (or withdrawing) a penny can feel confusing. But don’t worry, it’s totally normal. Let’s break down what’s going on behind the scenes – and how to respond when things dip.

Unlike a savings account, your pension doesn’t just sit still generating interest.

Each contribution from you, your employer, and the government (through tax relief) buys “units” in your chosen pension fund. These units are invested across things like stocks, bonds, and sometimes cash – depending on how your plan is set up.

At Penfold, our plans are actively managed. That means your mix of investments can shift in response to what’s going on in the world – helping to reduce risk and boost potential returns.

So when the market moves, your pension does too.

Your pension pot can fall in value for lots of reasons – a wobble in the stock market, political news, inflation jitters, or wider global events like a war or pandemic. It’s not always fun to see, but it is completely normal.

The value of your pot is shaped by three things:

It’s that third one – performance – that causes the ups and downs.

The short answer? Usually, nothing at all.

Investing is a long game – especially when it comes to pensions. That means temporary dips aren’t something to panic about. Things like the COVID-19 pandemic, the Russia-Ukraine war, or the US Tariff announcements can cause temporary dips in investments. And as with all investments, your capital is at risk so pensions can go down in value as well as up and you could get back less than you invest.

But it’s important to remember that changes in your pension value are completely normal. It’s all part of the investing process. Over time, markets have a habit of bouncing back. Reacting in the moment could mean locking in losses or missing out on future growth.

And most of the time, it’s better to simply do… nothing. Just giving your pension pot time to recover can be the wisest move. Remember, you’re likely saving for upwards of 40 years so are looking for long-returns not quick wins. Investing is a marathon, not a sprint.

When markets wobble, it’s totally natural to feel like you should do something – and switching to a lower-risk plan might feel like the sensible move. But here’s the thing: that decision could actually lock in your losses.

Let’s say your pension has taken a dip. If you switch to a lower-risk plan while your investments are down, you’re effectively selling those investments at a discount – before they’ve had a chance to bounce back. That means you miss the recovery, and your pot never gets the chance to regain its value.

It’s a bit like leaving a rollercoaster at the lowest point – just before the next climb.

Markets tend to move in cycles. Periods of decline (known as bear markets) are often followed by periods of growth (bull markets). Historically, recoveries have lasted longer than downturns – and delivered strong gains for those who stayed the course.

If you’re getting closer to retirement, you’ve got less time to ride out market drops. You might want to shift to a less volatile, and less likely to dip, plan. That’s why our default Penfold Plan gradually shifts to more stable investments as you approach retirement age – helping protect the pot you’ve built up.

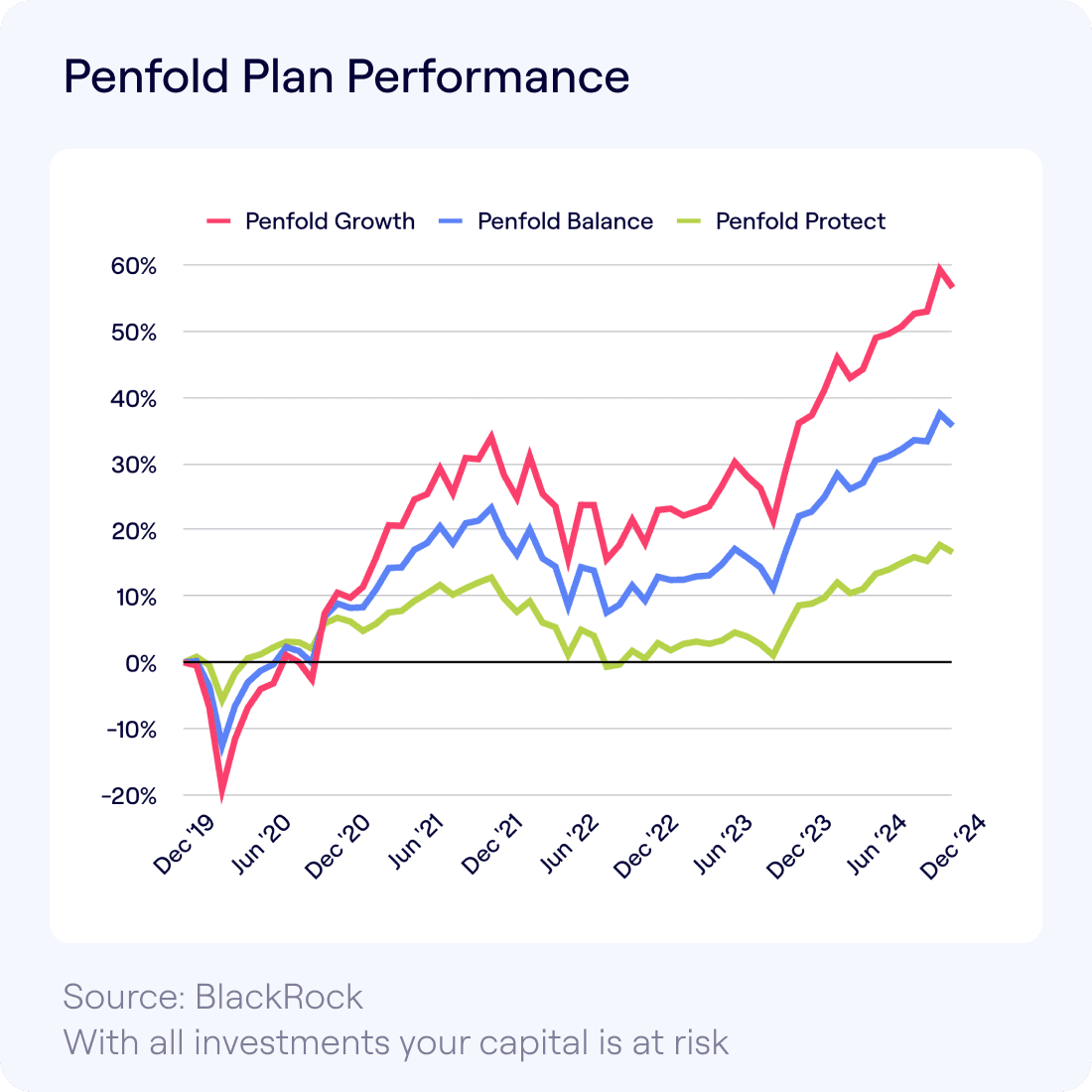

Here’s a look at the simulated performance returns of our core investment Penfold Plans – Growth, Balance, and Protect – since late 2019.

Past performance is not a reliable indicator of future returns. All investments carry risk and your investment value can go up or down. Returns may increase or decrease as a result of currency fluctuations.

Let’s be honest – 2020 was a bumpy ride for everyone. Each plan took a dip in early 2020 (thanks, COVID) – but the recovery tells a powerful story:

Each plan is built for different comfort levels with risk. But they all show the same core truth: short-term drops don’t mean long-term disaster. If you’d pulled out during one of those dips, you’d have missed the recovery.

This information should not be regarded as financial advice

Simulations are based on data provided by BlackRock of how the portfolio might have performed had these building blocks of the plan existed together over the last five years. It’s important to note that it cannot be definitively said exactly how this plan would have performed in the past. Simulations should not be taken as a guarantee of expected past or future performance, but are designed to be illustrative only. For the full list of assumptions used to generate these simulations, take a look at: Penfold Plan assumptions.

Because future investment returns are uncertain, we use three scenarios of projected growth; low (2%), mid (5%) and high (8%) – with an assumed price inflation of 2%.

Using a 2% average, a monthly contribution of £250 over 40 years could see your pension grow to nearly £183,915, thanks to the magic of compounding. A 5% average in the same scenario could see you save £383,095. And a high level of returns at 8% could grow to £878,570.

Our default fund, the Penfold Plan - Penfold Growth, has seen an average simulated annual growth of 11.4% from inception to December 2024.

While it’s important to acknowledge the risks, it’s equally crucial to recognise the potential for long-term growth. Diversified investing over the long term has an incredibly low chance of diminishing your initial investment. In the world of pensions, time is your ally.

Your journey to retirement is filled with ups and downs – and we’re not just talking about your pension pot. But remember, investing can be a rewarding path.

If your pot value has dipped and you’re not sure what to do, start here:

At Penfold, we believe your pension should feel like a source of confidence, not confusion. We’re here to guide you through these fluctuations, ensuring you’re well informed and ready for whatever the financial weather brings.

Our app makes it easy to track your pot, check performance, and feel in control – no matter what the market’s doing. And if you ever want to talk things through, our friendly team is just a message away.

Saving for retirement is a long-term adventure. We’ll be with you every step of the way.