What is a pension fund?

Pension funds, managed by fund managers, grow via investments, dividends & interest. Types include managed & tracker funds. Read our guide for more detail.

9 May 2026

5 min read

Everything you (or your employer) pay into your pension is invested into a fund. The value of your pension pot at retirement depends on how much you've contributed, how long it has been invested and how your fund has performed.

In this article, we'll look at what a pension fund is, pension fund performance, and how to find the best pension fund for you.

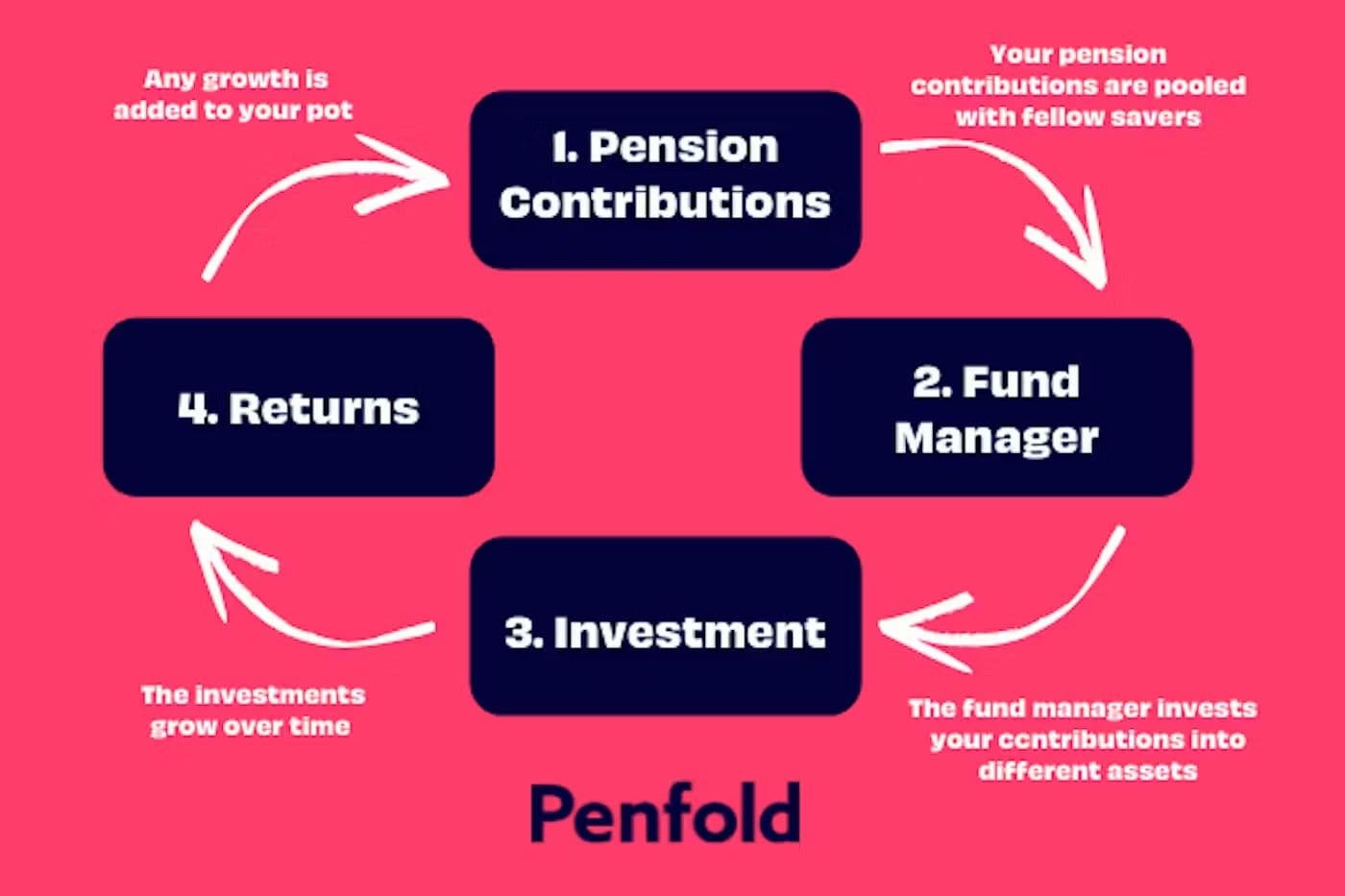

A pension fund is a special type of investment fund, created by a fund manager to help your pension grow.

They work by combining the pension contributions of different savers into one giant pot, which is then invested into a range of financial assets, including equities (company shares), bonds and gilts, property, and even cash. The pension customers bear the investment risk.

Every time you pay money into your pension, the fund manager uses your contribution to buy 'units' of whichever fund you're invested in. A unit is simply a small portion of ownership in the fund. The more units you have, the bigger your stake.

The exact makeup of a pension fund varies by provider and objective. Some funds make riskier, more aggressive investments in the hope of generating better returns, while others target safer investments.

The fund manager's job is to make sure all investments are made with these goals in mind to achieve the best return possible for you.

Over time, the value of each fund unit will hopefully grow. This growth comes from stock price increases, interest earned on fixed interest investments, and dividends paid out from shares.

However, because these investments are susceptible to market forces, it's vital to remember that the value of your pot can go down as well as up.

As with most types of investment, pension funds come in many shapes and sizes, varying by investment style, goals, industry sector, or geographical location.

Here are two of the most common kind of pension fund.

Managed pension funds are put together by a fund manager (or group of fund managers) and actively managed to try to achieve the best returns.

The fund manager will change the exact makeup of the fund on a regular basis, taking into account recent performance and real-world events.

Tracker pension funds are passively managed. Rather than picking investments to chase high returns, these funds aim to automatically follow a wider index such as the FTSE 500. They tend to have lower fees than actively managed funds.

"Pension growth comes from stock price increases, interest earned on fixed interest investments and dividends paid out from shares"

With Penfold, you have a few different options for your pension.

Our pension plans are actively managed, run by HSBC and BlackRock, two of the biggest fund managers on the planet. They look after these plans for you, taking away any stressful decisions on where to invest. You can see the full details of our pension plans here.

Exclusive to Penfold, our default Penfold Plan offers 100% FSCS protection, pursues sustainability goals and is custom built to help boost your pension pot.

Our Standard plan is managed by BlackRock. It's our simplest plan which invests your money across stocks, bonds and commodities, adjusting your risk level as you get older and into retirement. You can also tailor it to different risk levels.

Our Sustainable Plan is managed by BlackRock. It invests in countries and companies with sustainability goals, adjusting your risk level as you get older and into retirement. You can also tailor it to different risk levels.

Our Sharia-compliant plan is managed by HSBC. Approved by an independent Sharia committee, this plan invests 100% in shares that are fully compliant with Sharia law.

Our plans have a pre-chosen selection of funds within them which you cannot change yourself. To this extent, Penfold is not a Self-Invested Personal Pension. Find out more about Self-Invested Personal Pensions.

Most pension providers should let you switch between the different funds they offer.

As always, it's important to weigh up all the options and think about the pros and cons of each fund before switching. Moving funds normally takes a few days and you may also miss out on growth while your pension is between investments.

If you'd like to transfer your pension fund to a different provider, you'll need to request a formal pension transfer.

With Penfold, you can switch plans at any time for free. Simply sign in online or in our app and head to 'Your Plan'.

When you die, your pension fund can be inherited by a named beneficiary. How this works depends on the type of pension you have and whether you've used your pot to buy an annuity. You may also have to pay tax on anything you pass on.

When choosing your pension fund, you may also want to know where exactly your money is going. Your pension provider should be able to send you detailed information about each fund, outlining its investment objectives, charges and other information, such as where it invests (normally broken down into country and type of asset or sector).

With Penfold, you can see a complete breakdown of the investments in your chosen pension fund online, including which companies you're investing in. You can even use the power of your pension to vote on company policies!

Penfold are not financial advisers. The information above applies general rules of thumb when it comes to investing. If you’re unsure whether investing is right for you, consider seeking advice from a financial adviser who can help you with your personal financial circumstances.

As with all investments, your capital is at risk so your pension value may go down as well as up in value and you may get out less than what you invested.