Introduction to investing

Here's our quick introduction to investing - how it works and why you should consider it, all broken down in plan English.

Chris Eastwood

5 April 2023

6 min read

The whole point of a pension is to save up enough money to stop working one day. We believe this is the best way to save for the future, so it's important to familiarise yourself with what happens to your money while it's in a pension.

This is a brief beginner's guide to investing, to help you feel informed. You can refer to our glossary of pension terms for context.

A pension is a savings vehicle, and all the money you put into it gets a massive boost (25% or even 67% depending on how much you earn) from the government through tax relief. This is the biggest boost of any savings product out there, which makes pensions such a great way to save for later life. The obvious catch is that you can’t touch the money until you are 55 years old.

But your money should get another, even bigger boost. Everything that you save up into a pot is then invested. This aims to grow your money more than by leaving it in a bank account.

Investing your money sensibly can help it grow by around 5-7% per year on average over the long term. That might not sound like a lot, but if your money grows at 7% every year for 30 years, it would have grown by 760% over that time thanks to compound returns. So based on that 7% growth:

Investing is just buying something with the aim that you will end up with more money than you spent. If you save your money into a pension, it is then invested by a professional investment manager (also called asset manager, or we call this money manager for simplicity), in order to make your money grow. The money manager invests your money in a broad mix of stocks and bonds, each of which may go up and down in value.

Obviously, the aim is that overall and over a long period of time, you have many more investments that go up rather than down, so overall your money goes up significantly in value.

Historically speaking money grows significantly if invested across the stock market for a long period of time. Over the last 100 years the stock market has gone up on average by 10% per year! But the ups and downs from year-to-year can be pretty big, so money managers try to dampen the effects of the downs while still capturing as much as possible of the ups, through diversification.

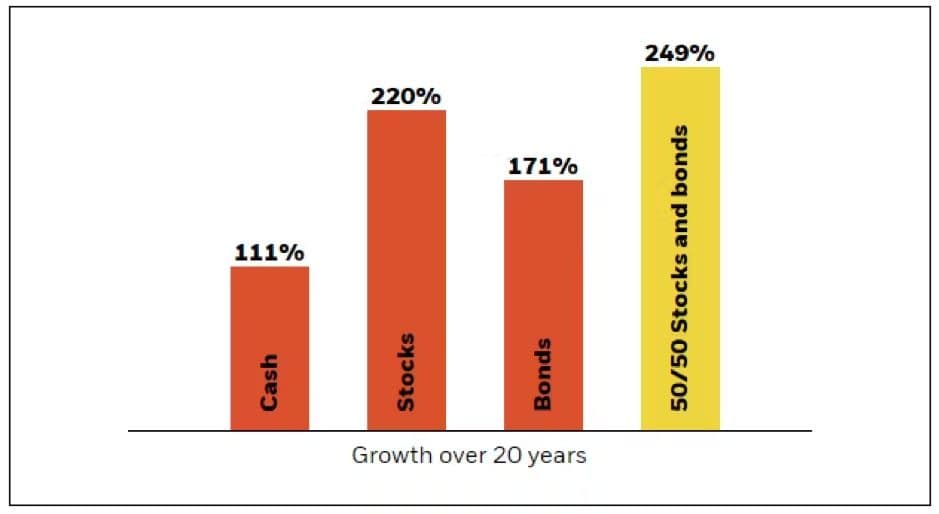

The chart below from our partners at BlackRock shows the difference in growth over the last 20 years from having your money in a bank account ('cash') vs. investing it in stocks or bonds. Interestingly, the best growth is from a 50/50 split with stocks and bonds. This shows the benefits of both risk and diversification.

Source: BlackRock

This possibility of your investment going up or down in value is known as risk, but risk is good. It’s what helps you earn more than just earning interest in the bank account. Take a look at this introduction to understanding the role that risk can play in investing.

What is important is how your money is invested, and how this risk is managed by professional money managers, like BlackRock. This is so you have the best chance possible of your savings growing by a good average return over the long term.

There are many thousands of different ways your savings can be invested. We have partnered with BlackRock, the world’s largest asset manager, to invest your money in line with four fundamental principles that we really believe in:

1. Passive investing

Rather than investing in individual companies within a particular market (which would be called active investing), passive investing means picking a particular market (e.g. FTSE 100) and buying a little piece of every stock or bond within that market.

2. Diversification

One of the best ways to manage risk is through diversification. The money manager does this by investing your pot across a wide range of stocks, bonds and other investments, across multiple different countries and markets. By doing this, you are reducing the chance that all of the individual investments all go up or down at the same time (this is called correlation), and increasing the chance that your money grows in a more stable way each year.

3. Low cost

This is the main thing that is in your control when you are investing. Investment management fees are generally a percentage deduction from your pot each year, so the bigger the percentage, the lower your pot will be. It is all about balancing the chance of large gains against the cost.

The total fees for Penfold are 0.75% per year (with no hidden nasty fees), which compares to a reasonable expectation of long term growth rate of 5-7% per year (although this is not guaranteed).

4. Managed risk

Diversification is great, but you also need to determine how to split the investment between assets (stocks, bonds) and between markets (different countries and industry sectors). This is done through allocation. Higher risk plans tend to have a higher allocation to stocks (generally high risk), and lower risk have a higher allocation to bonds (generally low risk). Managed risk means that this split between stocks and bonds isn’t set in stone, but can shift a little based on what’s happening in the investment markets. This is what should shield you from ups and downs that are greater than you were expecting. This sort of thing is usually quite expensive, but BlackRock’s advanced technology within the MyMap funds keeps it all low cost.

Create an account with us today and start saving for your future.

With pensions, as with all investments, your capital is at risk and the value of your pension with Penfold may go up as well as down. You may get back less than you put in.