Do I Need to Declare Pension Contributions on My Tax Return?

Filling out your Self Assessment tax return? Learn when and how to declare pension contributions – and whether you’re owed extra tax relief.

Murray Humphrey

15 January 2026

8 min read

It’s always worth checking whether you’re owed extra pension tax relief, especially if you pay tax above the basic rate. Many people miss out simply because they don’t realise they need to include pension contributions on their Self Assessment tax return.

In this guide, we’ll explain:

Not everyone does. Just because you pay into a pension doesn’t automatically mean you need to include those contributions on your Self Assessment tax return.

The key rule is this: You usually only need to include pension contributions if you’re claiming more than basic rate (20%) tax relief. Let’s break this down.

If you’re employed

If you pay into a workplace pension arranged by your employer, in most cases you won’t need to enter your pension contributions on your tax return.

That’s because many workplace pensions either:

If you only pay basic rate income tax, there’s usually nothing extra to claim, so nothing to add to your return.

That said, it’s still worth double-checking how your scheme works. If you’re unsure, your pension provider or employer can confirm whether tax relief is being applied correctly.

If you’re self-employed

If you’re self-employed and pay into a personal or private pension, your pension provider will normally:

If you only pay basic rate tax, you won’t usually need to include your pension contributions on your tax return.

If you pay higher-rate (40%) or additional-rate (45%) income tax, declaring your pension contributions on your Self Assessment can be essential.

Why? Because pension providers only ever claim basic rate (20%) tax relief automatically.

If part of your income is taxed above the basic rate, you may be entitled to extra tax relief – and the only way to get it is by declaring your pension contributions to HMRC.

This typically applies when:

HMRC then refunds the extra relief either by:

👉 For a deeper dive, see our guide How to claim higher rate tax relief on pension contributions

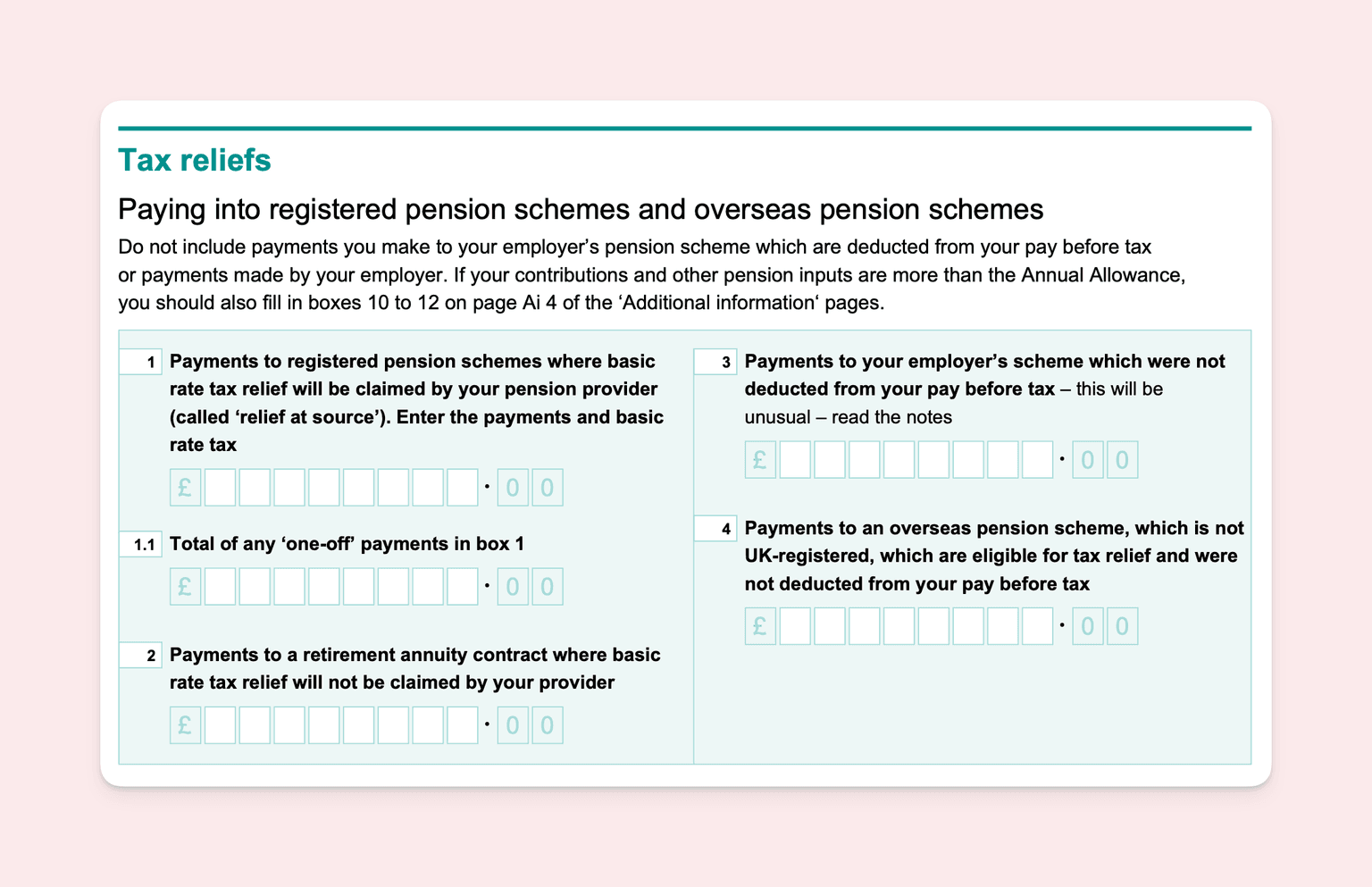

Your private pension contributions for the year are entered on the main Self Assessment form (SA100), in the section titled “Tax reliefs.” This section also covers things like:

For personal pension contributions made under the ‘Relief at Source’ system, use Question 1 of the SA100 form. This box is specifically for contributions to registered pension schemes operating under relief at source. You should enter the total amount of your personal contributions for the tax year, plus the basic rate tax relief added by your pension provider.

For example, if you paid £800 into your pension, and your provider claimed £200 as basic rate tax relief (20%), you would report £1,000.

Question 1.1 Total of any ‘one-off payments’ refers to the sum of any lump-sum contributions made to your pension during the tax year. These one-off payments are distinct from your regular pension contributions and might include:

If you contribute to a retirement annuity contract or an employer’s scheme not deducted from pay before tax, these contributions are reported in Question 2 and 3, respectively. These boxes are used for pension contributions where tax relief is not claimed at source and needs to be reclaimed.

For contributions to eligible overseas pension schemes, use Question 4. This is relevant if you're claiming tax relief for contributions to a pension scheme outside the UK that qualifies under HMRC guidelines.

If you have any one-off or unusual pension contributions, or if there are specific details you need to highlight, use the ‘Additional Information’ section on the SA100 form. This section can be helpful for providing context or clarity to your reported figures.

When declaring pension contributions, always use the gross amount for the tax year – including any basic rate tax relief. You can usually find this figure on:

With Penfold, you can check your total contributions in your dashboard. The figure above “Saved this year” includes any tax relief already added. You can also download a full transaction history from the Activity tab.

It’s important to remember that any contributions you add to your tax return should be gross and include any basic rate tax relief. Essentially, you need to tell the government how much has been added to your pension in total for this tax year. Once you’ve entered this, it’s time to start thinking about claiming back any extra tax relief you’re owed.

To claim additional tax relief, you’ll need to enter your total gross pension contributions for the tax year - including the 20% basic rate tax bonus. Once you’ve calculated your annual pension contributions, submit your tax return and HMRC will process your additional tax relief. Remember, you can also claim tax relief for previous years if you missed out on the past.

Your tax refund will take the form of:

You don’t need to put your tax rebate into your pension. You’re free to use your rebate as you please - although adding to your pot is a great way to help it grow.

Missed the deadline? You may still be able to write to HMRC to claim pension tax relief separately. For more details on this, head to the government’s dedicated page on claiming a tax refund.

For most people, the annual pension allowance is £60,000, or 100% of earnings (whichever is lower).

The only exception is the tapered annual allowance, which affects very high earners. If you earn more than £200,000 a year, we recommend visiting the government’s site on calculating tapered annual allowance to avoid any surprise tax charges.

Here’s the main takeaway: if you exceed this allowance, you may face a pension annual allowance tax charge, which must be reported on your tax return.

Do employer pension contributions count towards the annual allowance?

Yes, all contributions into your pension, whether they are from you, your employer or a third party count towards your annual allowance.

The Carry Forward Rule allows you to use unused pension allowance from the previous three tax years, potentially increasing how much you can contribute while still receiving tax relief. This can be especially useful if your income has increased or you’ve received a bonus. To use carry forward:

The information provided in this article is intended for general informational purposes and should not be construed as professional financial or tax advice. Pension contributions, tax relief, and related regulations can be complex and vary based on individual circumstances.

Tax treatment depends on the individual circumstances of each individual and may be subject to change in the future.