Tax Year End Checklist for the Self-Employed (2026)

Use pension contributions to reduce your self-assessment tax bill before 5 April. Learn about tax relief, annual allowance and key thresholds for 2026.

Murray Humphrey

16 January 2026

5 min read

The end of the tax year is one of the most valuable financial planning moments for self-employed people.

Unlike employees, you don’t get automatic workplace pension contributions — and your tax bill can feel unpredictable from year to year. But there’s also a major advantage:

Before 5 April, you may still have time to take action that reduces the tax you owe – while boosting your long-term savings.

One of the most effective tools available is making a pension contribution before the tax year ends. This guide explains how it works and what to consider in 2026.

Tax year end is a natural checkpoint to review:

For many self-employed people, pension contributions are one of the simplest ways to do exactly that.

When you contribute to a personal pension or SIPP, the government effectively helps pay into it too.

This is because pensions come with tax relief, designed to encourage long-term retirement saving.

Most pension contributions automatically receive basic-rate tax relief. For example:

That’s why pension tax relief is often described as a 25% top-up.

Making a pension contribution before 5 April can help you:

It’s one of the few tax planning moves that benefits both your future and your finances today.

The annual allowance is the maximum amount most people can contribute to pensions each tax year while still receiving tax relief. In 2026, this is usually:

Higher earners may have a reduced allowance, and contributions above the limit may trigger a tax charge.

If your circumstances are complex, it’s worth speaking with an accountant or adviser.

In many cases, yes. If you haven’t used your full annual allowance in previous years, you may be able to carry forward unused allowance from up to the last three tax years. This can be especially useful if you’ve had a particularly profitable year and want to make a larger one-off pension contribution.

Carry forward rules can be complicated, so professional advice is recommended.

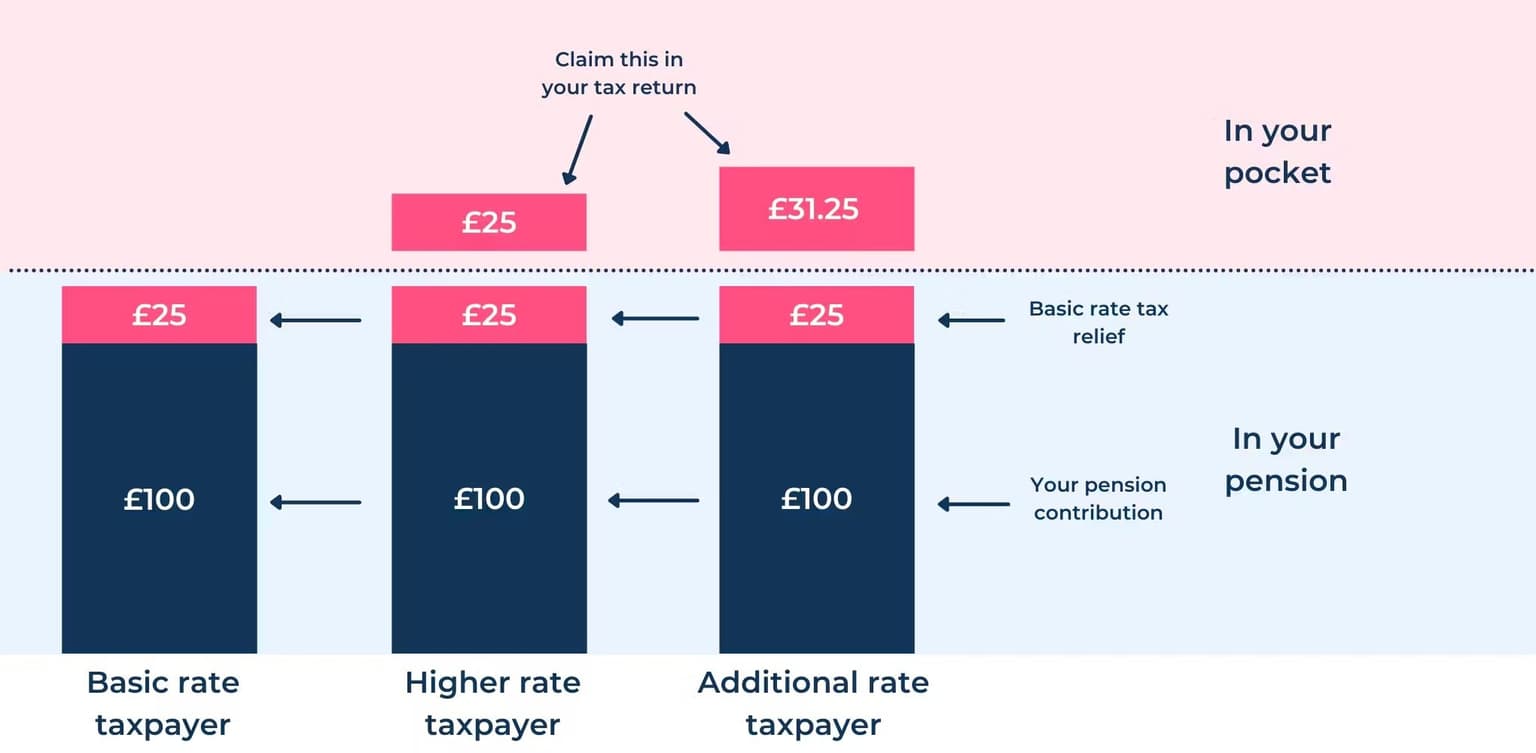

If you pay higher or additional rate tax, pension contributions can be even more valuable.

Penfold (and most pension providers) will claim the basic-rate relief and add it to your pension pot.

If you pay:

This extra relief is typically claimed through your self-assessment tax return. HMRC will either send this to you in a cheque in the post, or take it off your total tax bill. So pensions can be one of the most tax-efficient ways to save if you’re a higher earner.

You can see here how much tax relief you can get back in your pension and in your pocket, from a £100 pension contribution depending on your taxpayer bracket.

Tax relief depends on individual circumstances and may change in future.

Pension contributions don’t just build retirement savings — they can also help you manage your taxable income. Here are two important examples.

If your income exceeds £100,000, your personal allowance begins to reduce. For every £2 earned above £100,000, you lose £1 of your allowance. This means the effective tax rate in this range can be very high.

Because pension contributions can reduce your taxable income, making a contribution may help you:

This is a common planning strategy for self-employed professionals in high-income years.

If you (or your partner) receive Child Benefit, the High Income Child Benefit Charge applies when income exceeds £50,000.

Because pension contributions can reduce your adjusted income, they may help you keep more of your entitlement.

You can check the latest rules using the official GOV.UK guidance.

Before 5 April, consider:

Even one well-timed contribution can make a significant difference.

Pensions are one of the most effective long-term tools available to the self-employed. They offer:

Tax year end is simply a reminder to take advantage of what’s available — and ensure your money is working as hard as you do.

A pension contribution could help reduce your tax bill and build a stronger financial future.

👉 Learn more about the Penfold pension

👉 Or create an account in minutes and start saving today

With pensions, as with all investments, your capital is at risk and the value of your pension may go up or down. You may get back less than you put in. Tax rules depend on individual circumstances and may change. This article is for information only and does not constitute financial advice.