Self Assessment Tax Returns Explained: A Practical Guide

A clear, practical guide to Self Assessment tax returns – who needs to file, key deadlines, what you’ll need, and when to get help.

Murray Humphrey

13 January 2026

6 min read

If you need to file a UK Self Assessment tax return, it’s important to understand what it’s for, whether it applies to you, and what you’ll need to complete it.

This guide explains how Self Assessment works, who needs to file, key deadlines, and what to watch out for – so you can stay compliant and avoid unnecessary stress or penalties.

Self Assessment is the system HM Revenue & Customs (HMRC) uses to collect Income Tax and National Insurance from people whose income isn’t fully taxed automatically.

While most employees pay tax through PAYE, Self Assessment is required when you have income HMRC doesn’t already know about – or where tax relief needs to be claimed manually.

You may need to file a tax return if you:

Even if you’re employed and taxed through PAYE, you may still need to file if your financial situation is more complex. If you’re unsure, HMRC provides an online checker – or you can speak to a tax professional.

If you’ve never filed a Self Assessment before, you must register with HMRC.

If you’ve filed before, you don’t need to re-register unless HMRC has told you otherwise.

There are three key deadlines to be aware of, missing these deadlines can result in penalties and interest:

If you miss the deadline for submitting your tax return or paying your bill, you’ll incur a late filing penalty of £100 if your tax return is up to 3 months late. More significant penalties apply for longer delays. Interest is charged on late payments. However, you can appeal against a penalty if you have a reasonable excuse.

If this is your first Self Assessment, you would have needed to register with HMRC by the 5th of October telling them that you need to submit a Self Assessment tax return. HMRC would have sent you your Unique Taxpayer Reference (UTR) number which you’ll need for the return.

You’ll also need to gather a few documents about your income and relevant costs throughout the tax year. This includes:

Most people file online via HMRC’s website, which allows you to:

Alternatively, you can use an accountant. Penfold customers receive 10% discount with our partner, TaxScouts.

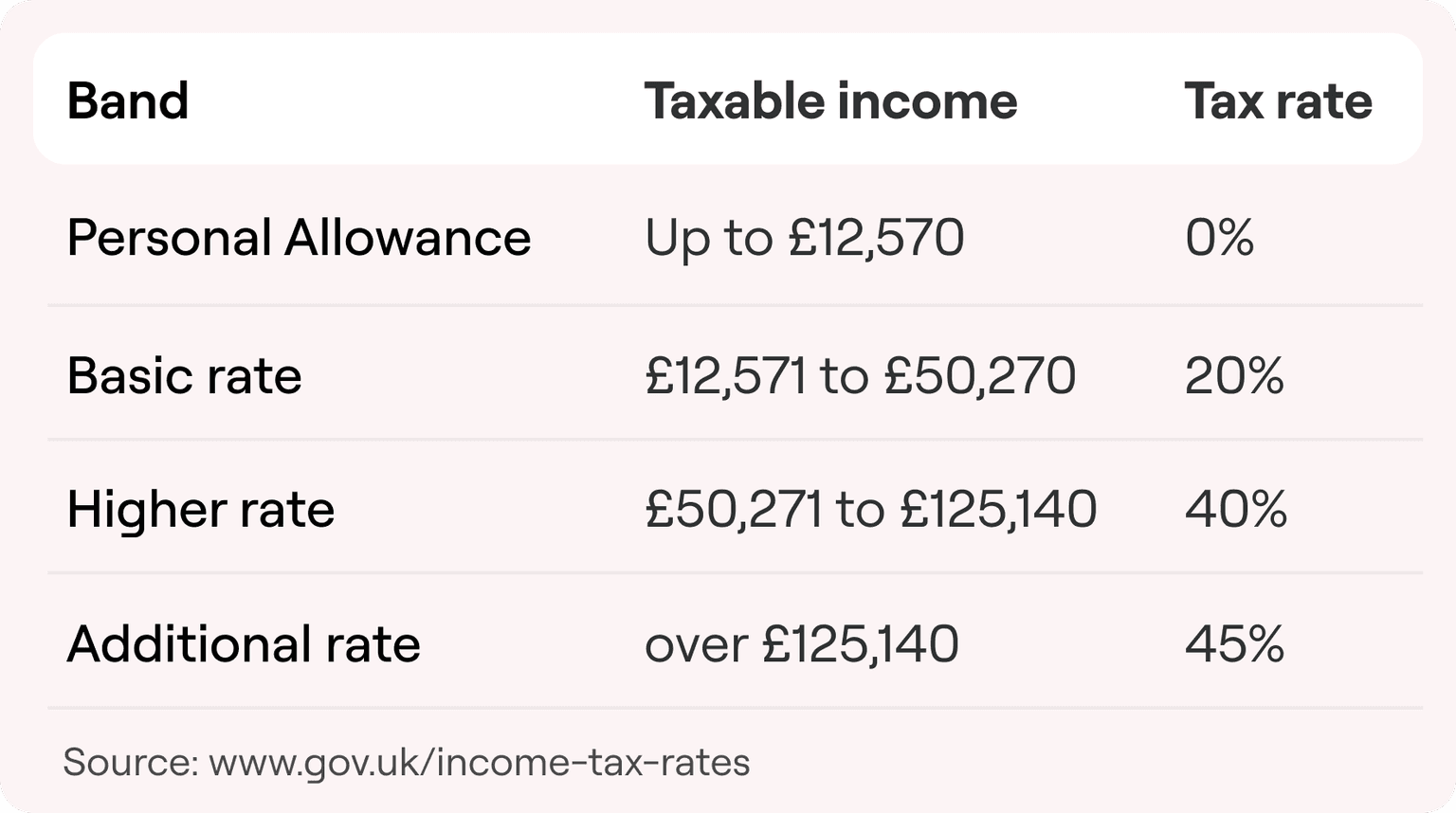

Everyone has a personal allowance, which is currently £12,570. Income above this is taxed at different rates depending on your earnings. Higher income may also reduce or remove your personal allowance entirely. Here’s a breakdown of income brands and their tax rates to help you figure out what you might owe.

If you’re self-employed, National Insurance is handled through Self Assessment. Key points:

Rates and thresholds can change, so it’s important to check the rules for the relevant tax year.

You may need to report capital gains if you sell assets that have increased in value, such as:

The annual Capital Gains Tax allowance is £3,000 for individuals. Capital gains are reported using the SA108 supplementary pages alongside your main tax return.

Self Assessment can vary significantly depending on individual circumstances. Unique situations may require additional attention:

In these cases, seeking specialised tax advice is often beneficial to ensure compliance and optimise tax liability. For detailed guidance, consider consulting a professional tax advisor or refer to specific HMRC resources.

If HMRC queries your Self Assessment tax return or decides to conduct an audit, it’s important to be prepared. HMRC may ask for clarification or evidence for certain figures on your return. This could be due to discrepancies or simply as part of their random checks. In an audit, HMRC thoroughly reviews your financial records and tax return. It’s essential to have all your documents organised and readily available, including income records, expense receipts, and bank statements. Cooperating fully and promptly with HMRC’s requests is crucial. If discrepancies are found, you may have to pay additional tax, interest, or penalties. Legal advice or assistance from a tax professional can be beneficial in these situations.

HMRC offers online guidance and tools, including digital assistants and videos. You can find more information on the GOV.UK Self Assessment pages.

If you need help understanding how pensions fit into your tax return, Penfold’s team is always happy to help via chat or email.

This article is for general guidance only and does not constitute tax or financial advice. Tax rules may change and depend on individual circumstances.