Accountants, you can recommend a workplace pension to your clients

It’s a widespread misconception that recommending a workplace pension to your clients constitutes financial advice. Find out the truth.

6 June 2025

3 min read

It’s a widespread misconception that helping your clients reassess their workplace pension scheme – or even recommending a specific provider – constitutes financial advice. But that's not the case!

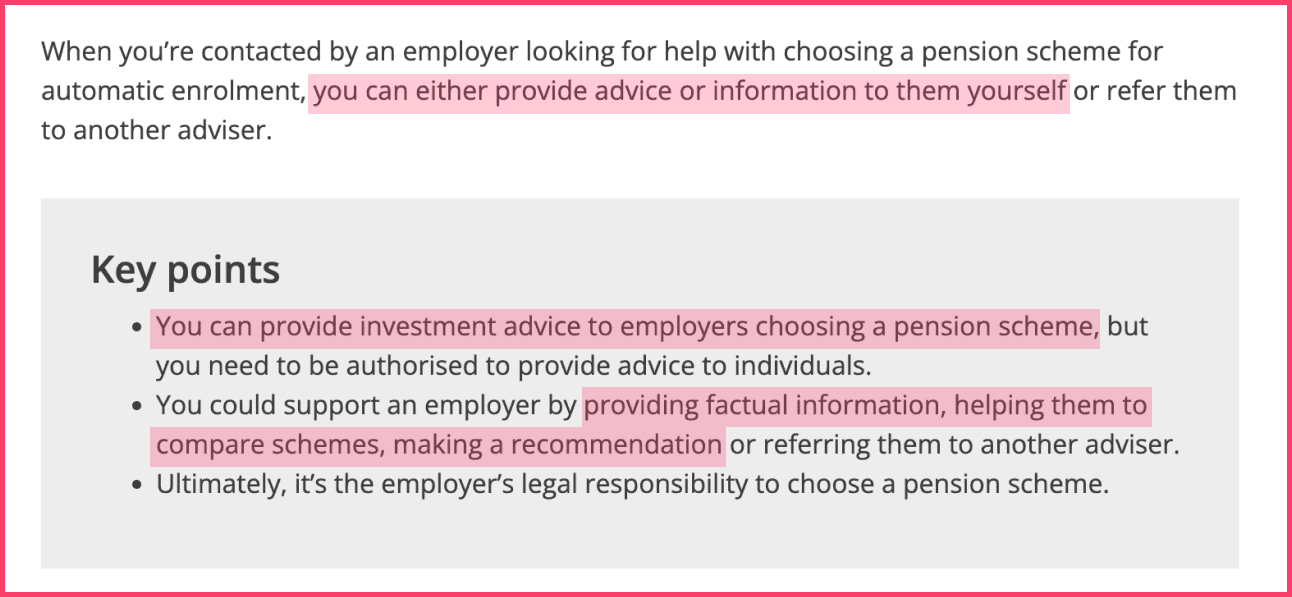

Crucially, advising employers on workplace pension scheme selection is not considered regulated financial advice. Don’t believe us? We’ve broken down the advice from The Pension Regulator. Find out what it means for you.

While this article is written with accountants in mind, The Pensions Regulator (TPR) makes clear that the same guidance applies to a wide range of business advisers.

TPR uses the term “business advisers” to refer to anyone helping employers with automatic enrolment and workplace pensions. This includes:

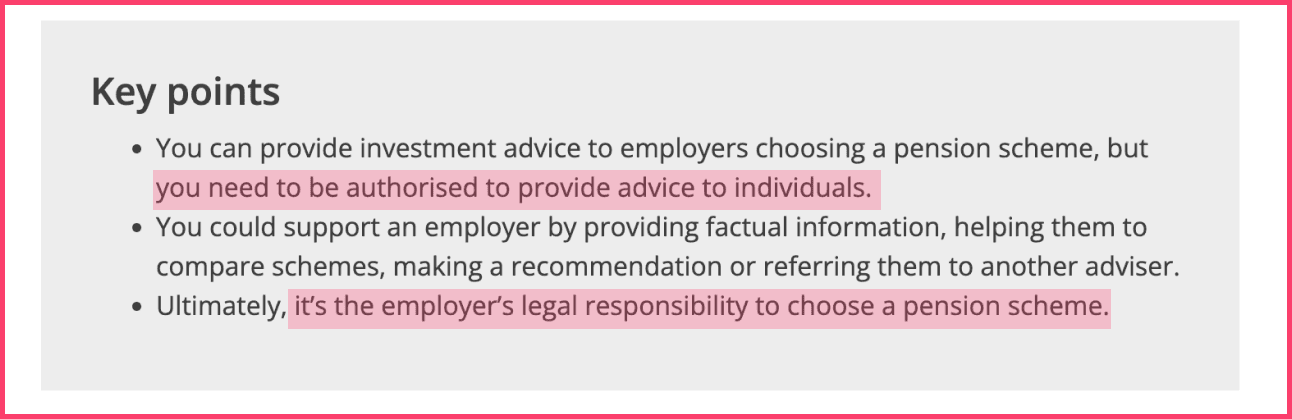

So if you're an accountant, you absolutely fall within this group. And crucially, TPR makes it clear that you can help your clients choose a pension scheme by providing factual information, comparing schemes, or even recommending one – without needing FCA authorisation.

Just remember – this all applies when you're supporting employers with their scheme choices, not advising individuals on their own pension decisions. That’s where FCA rules kick in.

According to The Pensions Regulator, as a business adviser you can provide advice to employers choosing a pension scheme by:

See for yourself! You’re free to do this without stepping into FCA-regulated territory:

Just because you can support employers doesn’t mean anything goes – TPR sets out some clear red lines. You can’t:

See the relevant information highlighted below:

Many companies – potentially including your clients – are dissatisfied with their current auto-enrolment scheme but don't know where to start when selecting a new one.

It’s also good practice to review their workplace scheme regularly to make sure it’s still fit for purpose. And hiring a dedicated consultant to help with this can end up being very costly.

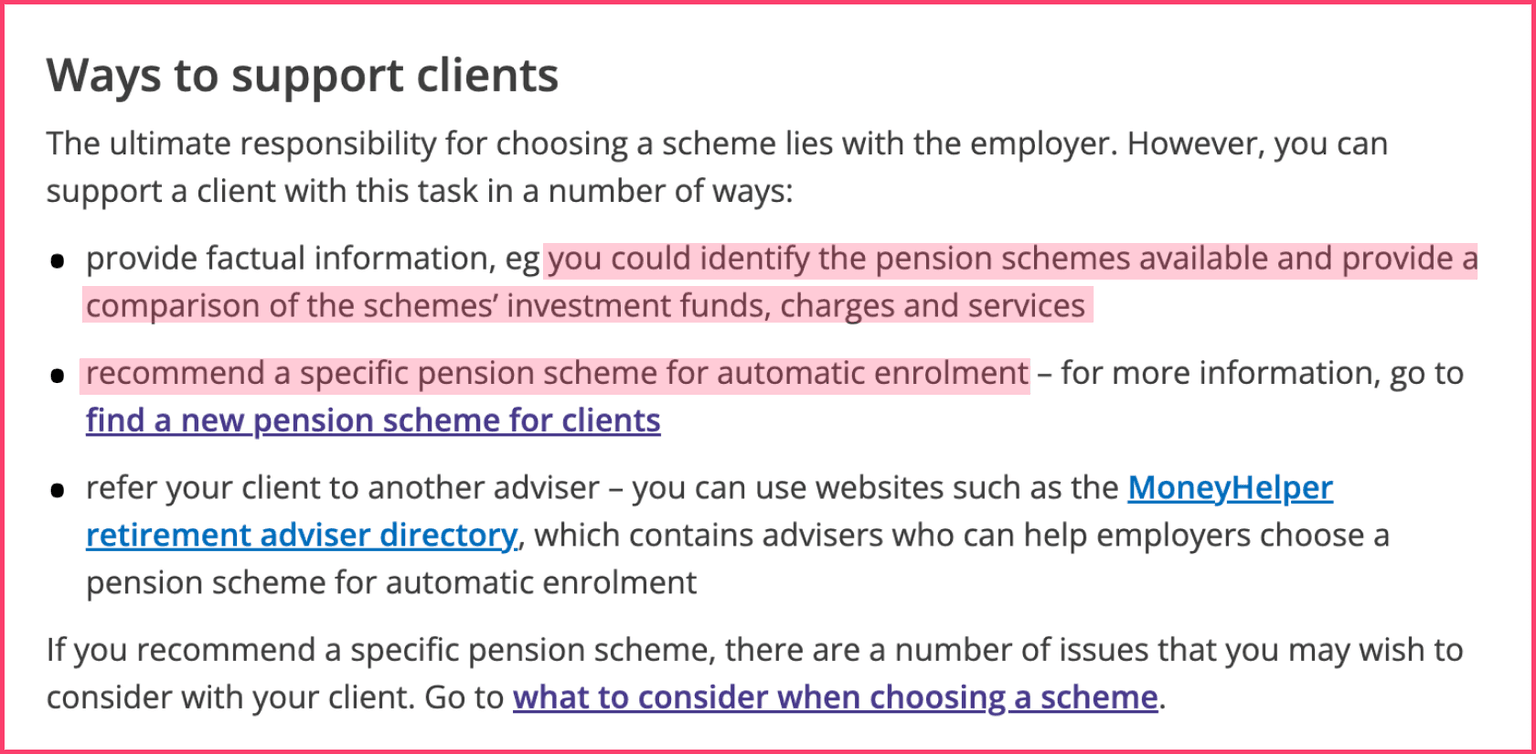

By stepping in with simple, clear guidance, you can provide a highly valued service that strengthens your client relationships. For starters, The Pension Regulator specifies some ways you can help your clients:

But there are so many ways to go above and beyond. At Penfold, we support many firms with the resources and materials they need to make these conversations easier, including:

Use our handy resources to guide your clients through their auto-enrolment obligations, helping them make informed decisions about their pension schemes that will benefit them and their employees.