Unveiling the Hidden Costs of Workplace Pensions

Explore the hidden costs of UK workplace pensions. Read our overview of some extra charges to watch out for when choosing a pension provider.

Murray Humphrey

30 July 2024

3 min read

When it comes to workplace pensions, transparency is key. Yet, many auto-enrolment providers cloak their fees in a shroud of complexity, leaving accountants and advisers struggling to understand and convey the true costs to their clients.

At Penfold, we believe in clarity and simplicity. This guide will help you navigate the often murky waters of pension fees and highlight why Penfold is the straightforward, cost-effective choice for you and your clients.

In the UK, there are 5.5 million businesses classified as SMEs, accounting for 99% of all businesses according to the British government.

Most of these have fewer than 50 employees. Since the introduction of auto-enrolment in 2012, all small businesses are required to provide a workplace pension for their employees, contributing a minimum of 3% of their salaries. This often makes workplace pensions the most significant benefit cost for employers.

However, the financial burden doesn’t stop at contributions alone.

Some pension providers impose additional charges which can add up quickly.

These costs can be avoided with some other workplace pension providers.

Did you know that Smart Pension have introduced a monthly employer charge?

Smart Pension stated that this fee would help improve their service and allow for platform enhancements.

Additional charges also affect employees.

Nest charges a 1.8% contribution fee. If an employee contributes £200 a month, they lose £3.60 each time, amounting to £43.20 annually or £432 over a decade, this doesn’t count the lost potential compound growth.

Some providers charge users a monthly ‘member administration charge’ on top of the annual management charge (AMC).

For low earners, this can be significant. For instance, someone saving £300 annually would see 7% of their savings go to these fees.

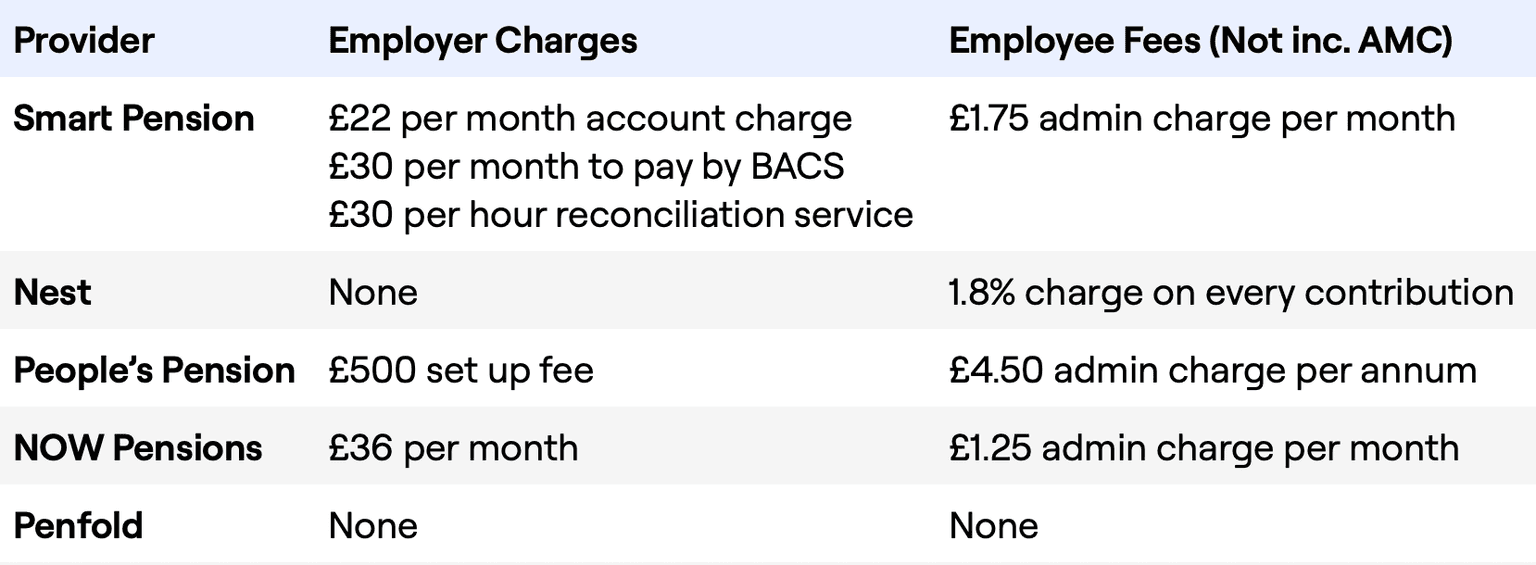

Pension providers charge an annual management charge (AMC) but some add extra fees, making it difficult to understand the total cost. Here’s a comparison of common workplace pension providers additional fees:

For a detailed comparison, check out our guide to different workplace pension providers.

At Penfold, we value transparency and hate extra charges – so we’ve created a fair, straightforward fee structure:

We understand the financial duty accountants have towards their clients, with Penfold you can offer a cost-effective solution.

When evaluating a new provider, consider not just the fees but also fund choices, performance, and customer service quality. We’ve put together a list of the things you should consider in our How to choose a workplace pension provider article.

Our modern workplace pension prioritises simplicity and transparency.

Our simple fee structure eliminates hidden charges, making it easy for both you and your clients to understand the true cost of their workplace pension. For more information about Penfold's one simple fee (the AMC) read our pension charges page.

Switching providers is simpler than many think; read our guide on how to change workplace pension provider to find out more.

Give your clients the peace of mind that comes with clear, predictable fees and the potential for significant savings.