Four ways accountants can fall back in love with pensions

Discover how accountants can navigate the complexities of pensions with ease. Dive into the benefits of transparent fees, responsive customer service, automation, & engaging pension platforms.

Murray Humphrey

1 August 2023

5 min read

Auto-enrolment is a double-edged sword for accountants. If they can help their clients choose the right pension provider and process the payments, it’s one more revenue stream to enjoy.

But with multiple file formats to grapple with, customer service too often involving long phone calls and a tightrope of tax compliance to walk, getting the work all finished and accurate in time for payroll can prove painful.

Rest assured there’s a better way. Accountants: it’s time to fall back in love with pensions. Here’s four reasons why.

A new way to look good to your clients

Partnerships are built on relationships and we know that accountants like being able to provide value to their clients. After all, if you can regularly demonstrate that you’re helping one of your customers out, they’re more likely to stay as your client for the long term.

The principal way is to help them save money and there are two easy ways to do this. The first is the fees employers might be getting charged by their pension provider and the second is the charges incurred by employees.

Some pension providers levy monthly charges to employers. What’s almost worse is trying to get clarity on those fees and others (one example: employees being charged to contribute to their pension).

Googling for some of the more famous providers’ fees will see you disappearing down rabbit holes that end in spreadsheets containing a bewildering smorgasbord of percentages.

At Penfold we keep it simple. We don’t charge employers anything for their workplace pension. For employers there are no account fees or management charges, and no adviser fees. We make all our charges transparent on our pension charges page.

Customer service you can actually talk to

A common complaint we’ve heard from accountants is that they find it hard to get in touch with the pension providers when they really need to.

When payroll needs to go out and you’ve got an issue with a payment, the last thing you need is to spend your precious time listening to tinny muzak whilst endlessly waiting in a queue for someone to talk to.

In the worst cases, Trustpilot lists records of people waiting three weeks for a reply to an email from some of the better known auto-enrolment providers!

At the time of writing, Penfold is the best rated workplace pension provider on Trustpilot. One of the reasons is that, with us, you get a dedicated account manager to contact in a number of different ways, including common messaging software like Slack. And if you’ve got a problem you really can’t fix, you can hand it over to us and we’ll figure it out.

Automation to make things easier

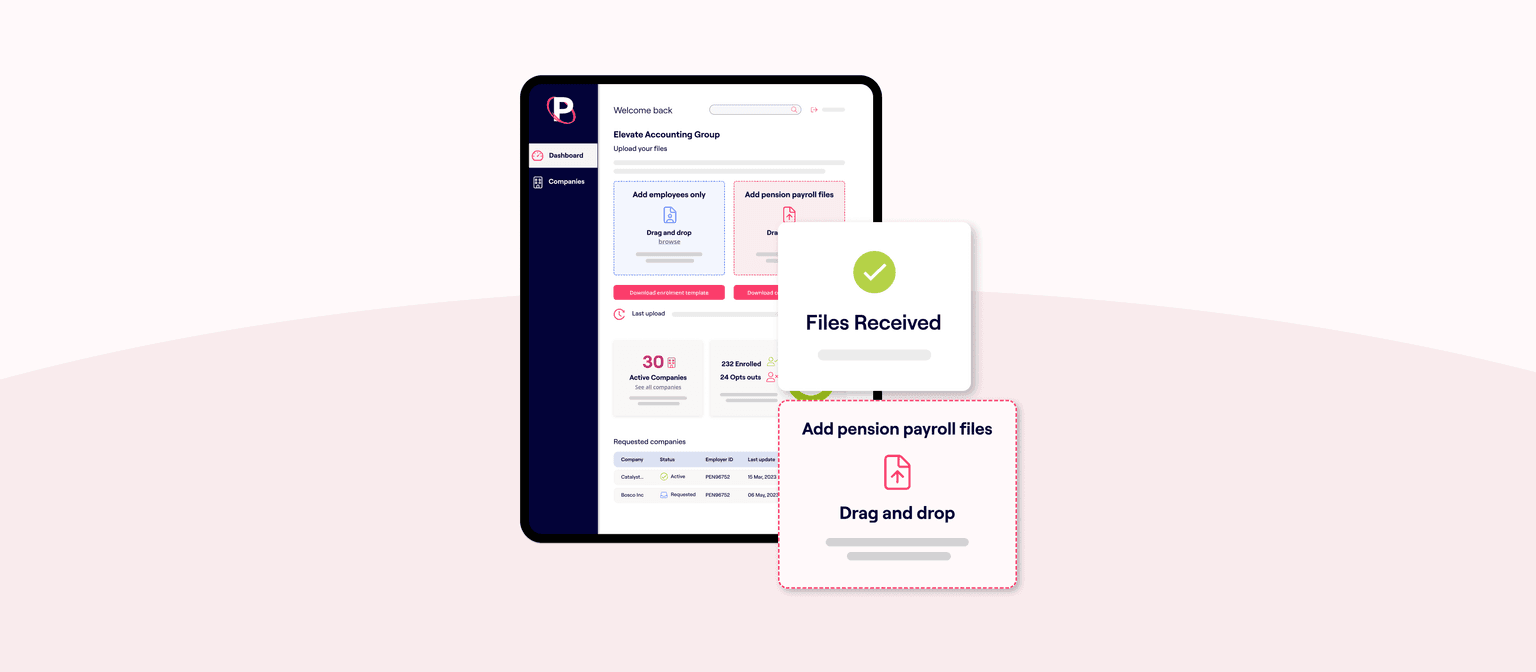

Remember when we all thought Excel spreadsheets were pretty cool? Tech has moved on quite a bit since then. Instead of squinting at cells, software such as our workplace platform presents data in a more user-friendly way.

Penfold pension processing platform

Not only is it easier to find the figures you need, the clarity it offers actually helps when striving for 100% accuracy. We know that pensions present a minefield for accountants when it comes to maintaining accurate records. No longer. Contribution statuses, opt-out summaries, and employee payment histories – all easy to find and check.

We’ve also done away with the cumbersome task of reformatting and uploading multiple different file types sent by clients. Drag and drop any recognisable file into the platform and it’s done.

Efficiency, accuracy, compliance. All wrapped in a package designed to make pensions that bit more pleasurable. You can see what we mean on our pension platform page.

A pension that people won’t put off thinking about

It’s no wonder pensions have an image problem. An annual statement letter containing disappointing figures, with no help offered as to how to improve the situation, is hardly likely to promote engagement. It’s no wonder the Institute of Fiscal Studies found that 90% of people are not saving enough for retirement.

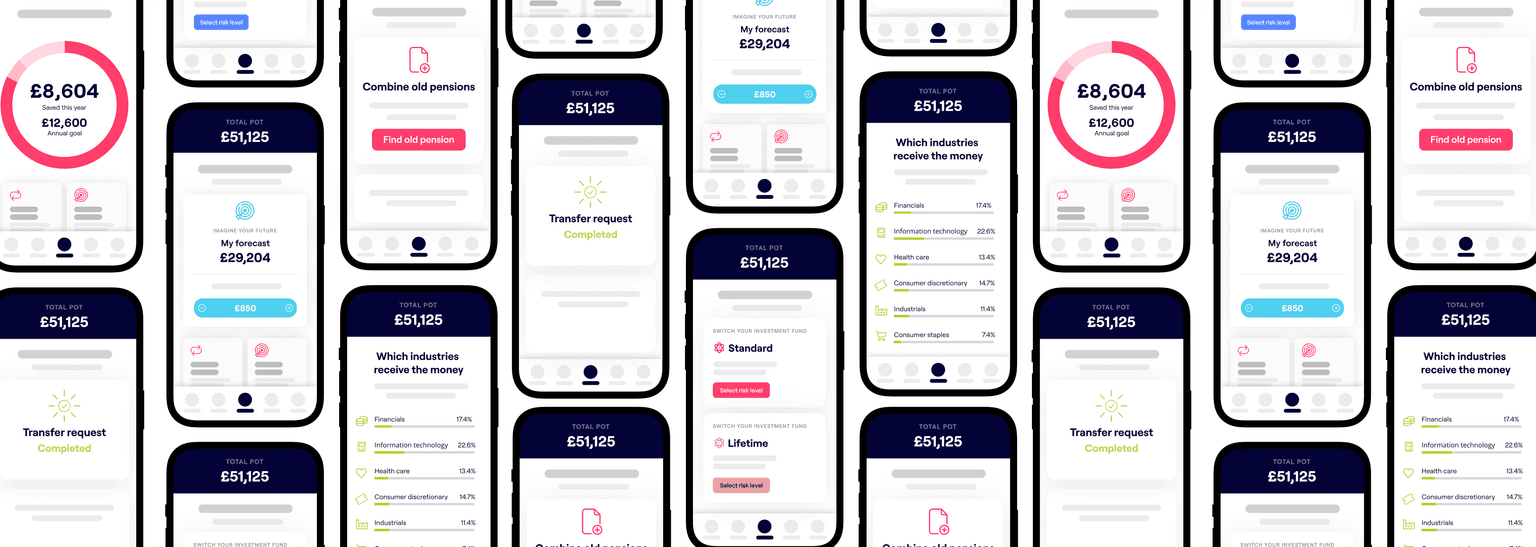

If the phone in your pocket can book airline tickets, track your physical health and tell you how much you’ve got in your bank account, it can certainly help you plan for the future. Open the Penfold app and it instantly tells you how much you’ve got and how much your savings have grown by.

Our customers get the dopamine hit of being notified when their employer has dropped some money into their fund and the forecast tool tells them what income they’re on track for – but not only that. It places users in one of three retirement lifestyles, based on the Pension and Lifetime Savings Association’s Retirement Living Standards.

Penfold app

This tells them what their retirement income will pay for in terms of regular costs such as the weekly shop, transport and holidays. In short, it takes the guesswork out of figuring out how much people will need to have the kind of life they want when you stop working.

All of which means people can feel more in control of their finances. It’s one less thing for them to worry about. And if employees are that bit happier, it’s got to be good for the companies they work for.

Final thoughts

For some accountants, we appreciate that processing pension contributions can be painful. But remember that if they’re a hassle, it doesn’t have to be that way – especially if you’re with the right provider.

They also represent an opportunity: if you can suggest ways for clients to save money with an alternative pension provider, you’ll be scoring a heap of brownie points that should help to cement relationships.

If you still haven’t fallen back in love with pensions, we’d love to change that. Fair warning: a ten minute tour of our new workplace platform might yet set your pulse racing. Let us know when you can fit us in.