Pension interest rates: How do they work?

Pension interest rates work a little differently than regular savings accounts. Here's everything you need to know.

Murray Humphrey

22 May 2023

5 min read

When it comes to saving, many of us are used to traditional savings accounts with a fixed, steady interest rate. Pensions, like all investments, work a little differently. In this blog, we’ll look at how pension interest rates work and how this affects the value of your pension pot.

With a pension, everything you contribute into your pot is invested. Rather than sitting in an account with a locked-in interest rate, everything you pay into your pension is usually invested into a fund. Your money is then used to buy a wide range of different financial assets - from stocks and shares to government bonds and even property.

Exactly how your savings are invested depends on your pension plan, but here’s the thing to keep in mind: how well your pension performs comes directly from the performance of the investments inside your pension fund. Whether the value of these investments goes up or down.

Here’s the good news - in the past, returns from long-term investments (like your pension) have drastically outperformed any return from a regular savings account. And that’s not even taking into account the low-interest rates offered by savings accounts right now.

Of course, this also means you won’t see any ‘guaranteed’ interest rate attached to a pension. The actual rate of return will vary over time.

Regular savings accounts, whether easy access or fixed are about short-term saving. If you’re looking to put money aside for the long term, you’ll want to look at investing - and this involves a variable rate of return. Your ‘return’ (or the % your pension grows by) will change as the value of your investments rise and fall.

While it’s completely natural to be anxious as the size of your pot fluctuates, remember that a pension is likely the longest-term investment you’ll make in your lifetime. You won’t be able to access your pot until 55 at the earliest - this means there is more than enough time for any downturns to be corrected over time.

Plus, don’t forget any fluctuations you see in the meantime are sort of beside the point. It doesn’t matter if your return rate drops a little when you’re still 20 years from retirement. The only thing that matters is how much you have when you start to withdraw.

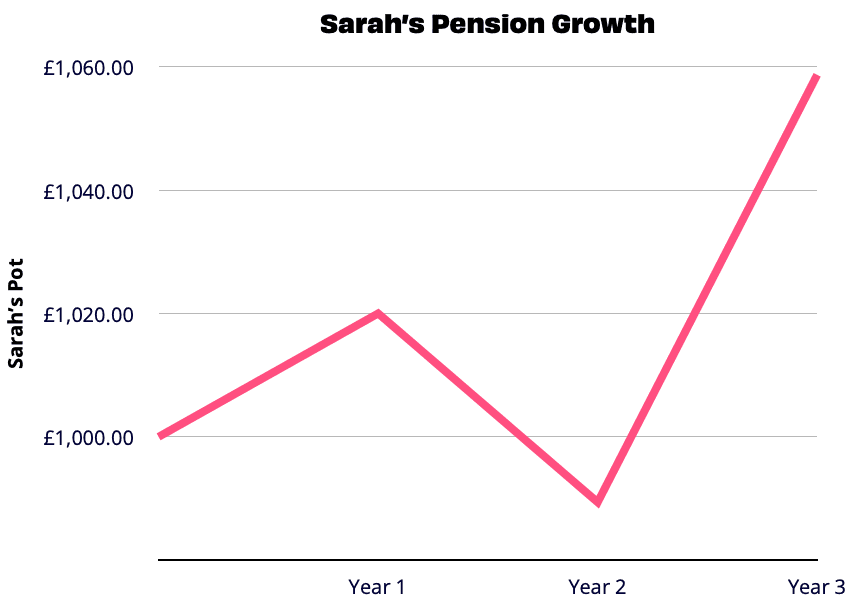

Let’s take a look at a simplified example: Sarah pays £1000 into her pension. During her first year, her pot grows by 2%. Great, now her pension is worth £1,020 - assuming Sarah is adding anything extra via regular contributions. However, the next year isn’t so good. There’s a market crash and her pension investments drop by 3%. Now her pot is down to £989.40. Luckily, her pension bounces back. The next year, the market recovers strongly and rises by 7%. Now Sarah is sitting on a pension of £1,058.66.

Despite the interest rate varying significantly, Sarah has seen an overall growth of 5.87% on her original contribution of £1,000. And this is how your pension can grow, even without a guaranteed interest rate.

As we outlined above, the interest your pension earns comes directly from the performance of your investments. But there is one more thing to keep in mind: compound growth. This can be a slightly tricky concept but it’s important to understand how it impacts your savings. Why? Because compound growth is your pension’s superpower. Compound growth is, essentially, growth on growth. Whenever your pot grows, any future earnings will come on top of your new bigger pot.

For example, if you get a 5% return on £100, you now have £105. However, the next time your pot grows, you’re getting 5% of £105 - your new pot amount.

The longer your savings are invested, the more you’ll benefit from compounding. And this is why long-term savings like a pension is so efficient. Check out our previous blog post for more on how compound interest works.

Over the last 5 years, pension funds in the UK have grown by just under 7% on average - in line with the assumed growth rate of 7% over 35-40 years. But the real answer to what kind of growth you should expect on your pension depends on a few different things.

First of all, how long you've been investing. With pensions, the younger you start saving, the better return you can expect to get. This is due to the nature of long-term investing and the power of compound growth as outlined above.

Secondly, your level of risk. Riskier investments tend to have a greater chance of netting you greater returns - although this also includes more ups and downs along the way.

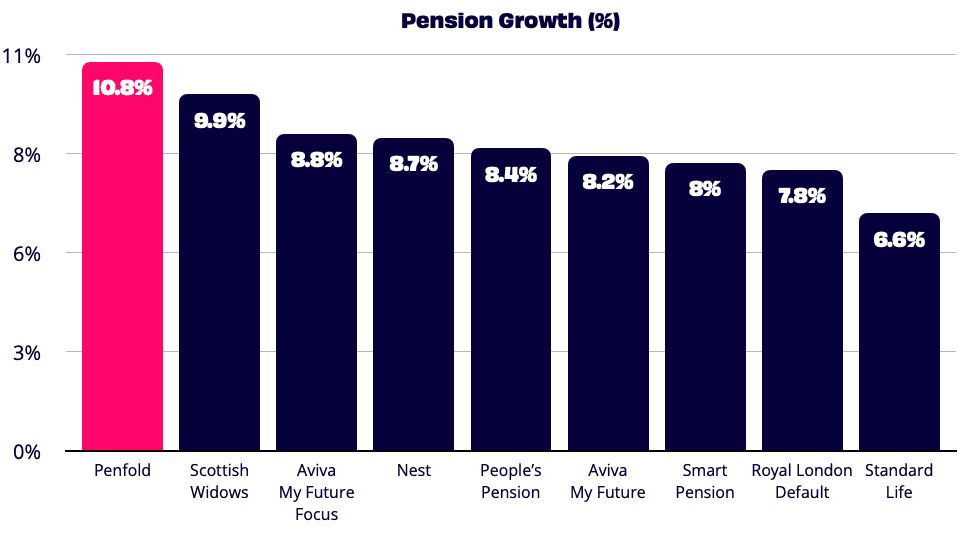

We recently shared the results of our most popular plan, used in both our private and workplace pensions - our most popular plan achieved a return of 10.8% over a simulated 5-year period.

These figures are particularly impressive when compared to the guaranteed interest rates available for easy-access savings accounts (≈0.5%) and fixed-rate savings accounts (≈1.5%).

To give that a little more context, let’s imagine you save £150 every month. After 30 years in a 1.5% savings account, you’d end up with roughly £68,000. However, investing the same money into a pension for 30 years with a 7% return would leave you sitting on £175,000. Even a small difference can have a huge impact over the long term.

In summary, there’s no way to guarantee a certain return on your pension - as with any investment. The secret to getting the best return possible, however, is simple. Give yourself time.

Remember, past performance does not guarantee future returns.