How do Penfold's fund performance & fees compare?

Read all about Penfold's fund performance for the last 5 years, as well as a comparison to other providers.

Murray Humphrey

13 October 2021

6 min read

A recent study exploring the UK’s biggest workplace pension providers found that Penfold has seen the best return on investment for its savers. In today's blog, we're taking a closer look at our fund performance and how our investing philosophy helped us deliver market-leading results.

Despite an uncertain economic landscape due to complications from the pandemic, Penfold has continued to provide our savers with a healthy return on investment. In fact, our most popular pension plan (used in our recently launched workplace pension) has grown significantly more than other main workplace pension providers.

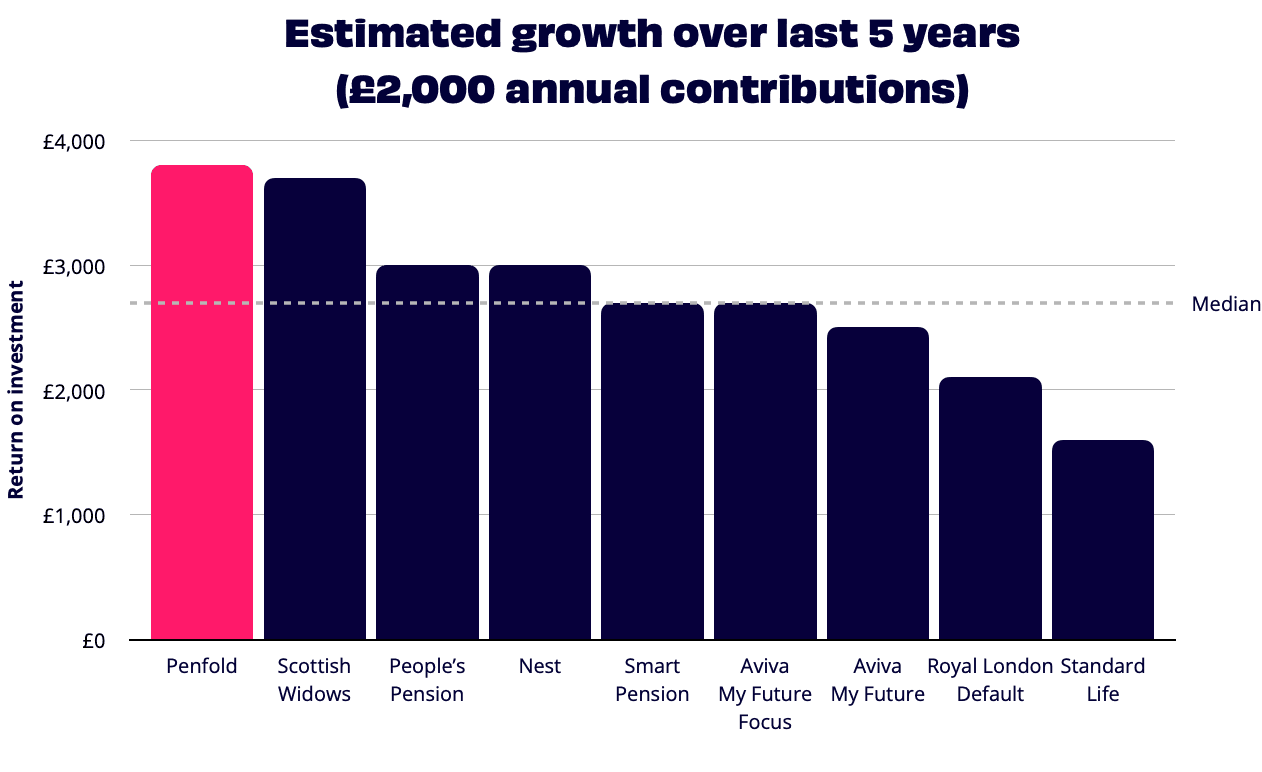

Let’s take a look at the numbers. The chart below shows how much someone’s pot would have grown over the last 5 years if they had invested in Penfold’s Standard risk level 4 plan compared to other workplace pension plans. It assumes contributions of £2k per year and shows the extra amount you would have above what you paid in by the end of the 5 year period.

*Data provided by Dean Wetton Advisory

Here's an example to help explain. Annabel is 25 years old and earns £25,000 a year. If she had opened a Penfold pension five years ago and contributed 8% of her salary into her pension (£2,000 per year), today she would have an extra £3,800 from investment returns above the £10,000 she had paid in, more than any of these other providers. Give it another 30 years until retirement, and that £3,800 could continue to grow and grow, up to £24k by age 68 assuming 5% indicative annual growth after fees.

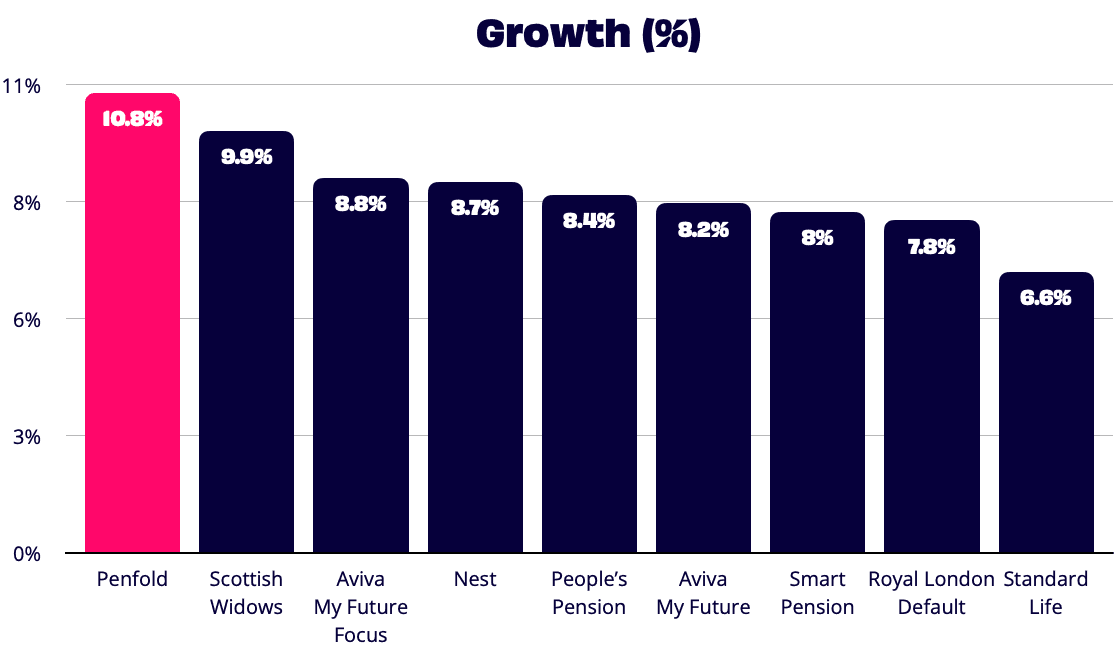

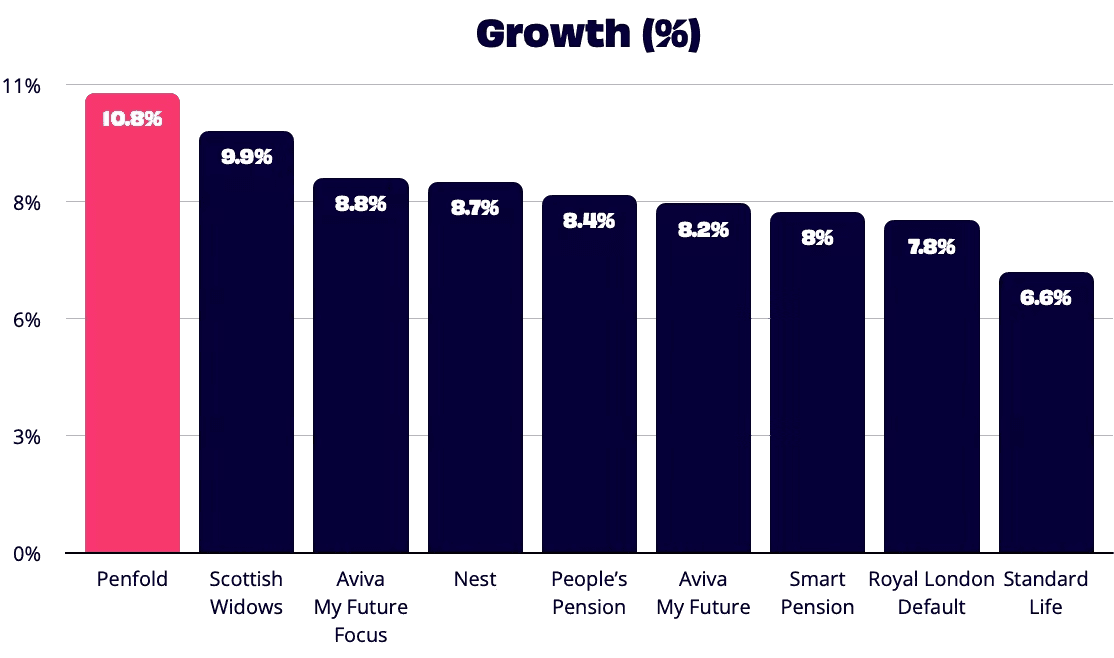

Now, let’s dig into our performance a little deeper. The next chart shows the underlying annual return on investment responsible for the growth in the above chart.

As you can see from the chart above, Penfold’s fund saw an average growth of 10.8% over a simulated five-year period. That’s more than 2% better than the median pension fund performance.

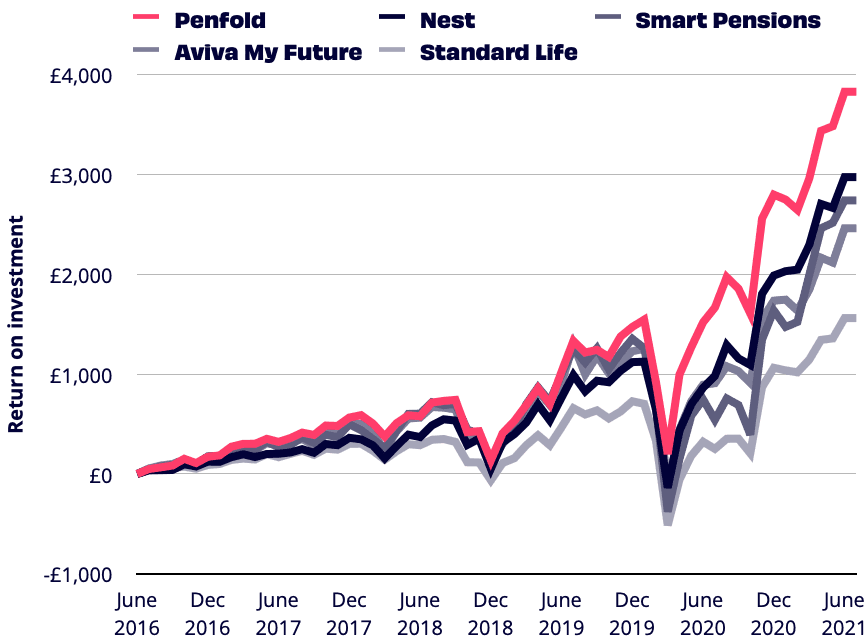

It’s great to know that Penfold savers have seen their pension grow more than with other providers. Now let’s take a look at how that unfolded over time, compared to a selection of these other providers.

You’ll notice each plan saw a dip around March 2020 when the markets were affected by the pandemic. Thanks to their active risk management strategy, our plans managed to provide a level of protection against the market dip, while allowing them to bounce faster than the rest.

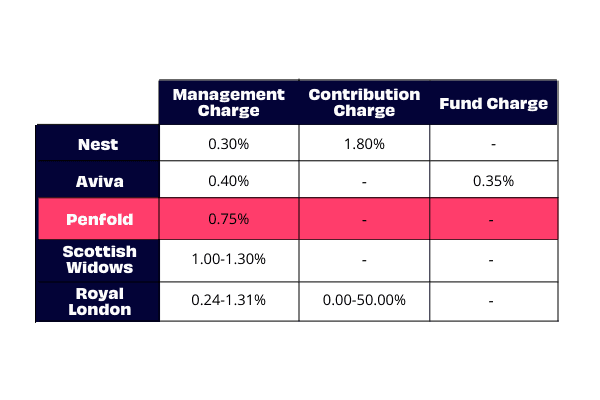

Not only is it great to know that Penfold savers have seen their pension grow from our out-performing funds, but also from our low fees compared to other pension providers. It is worth knowing that the returns above factor in fees and charges too.

Rather than use a variety of confusing fees, or charge you to pay into your pension, we prefer to keep it simple. That’s why we use a single, all-encompassing fee - to help you understand exactly how much your pension costs.

This one fair, transparent annual fee for managing your pension covers absolutely everything within Penfold’s pension service - including contributions, fund switches - anything. This fee is split between Penfold, our partners and your money manager for investing and administering your pension.

In the table above, you can see how our fees compare to similar pension providers. Other pension providers have other, hidden fees on top of the annual management charge - such as contribution and fund charges. This can often make the fee model seem complicated. For example, Nest charges a contribution fee of 1.8% for every transaction into your pension, which can get lost in your fee history.

It's always worth double-checking the fees of a pension provider you're with, or of one that you're considering transferring over to, or away from - as there can even be hidden exit fees depending on your total pot value.

Now, let’s dig into our performance a little deeper. The next chart shows the underlying growth responsible for the impressive return on investment we highlighted earlier in the blog. How about overall returns - how much the investments grew in our most popular plan. Based solely on returns over a five-year period, Penfold once again came out top.

*Data provided by Dean Wetton Advisory

As you can see from the chart above, Penfold’s fund saw an average growth of 10.8% over a simulated five year period. That’s more than 2% better than the median pension fund performance.

The secret behind this performance lies in how our investment partner BlackRock manages our savers’ money, in line with our core principles for investing:

2020 was a turbulent time for investors, with many markets falling and rising significantly throughout the year.

Our fund manager BlackRock managed to navigate through it all by being reactive - carefully adjusting investments within our pension fund in response to what was happening in the real world.

This helped to protect savers from many of the crashes, while still letting them benefit from the vast majority of market recovery - providing a far greater return on investment.

Some of the other workplace pension plans we’ve looked at have a more rigid approach to saving - preferring to keep the investments the same, regardless of what’s happening.

The simple explanation for how our plan outperformed the rest, in a word, is flexibility. It's all part of our mission to help more people stop worrying about the future - by providing a pension that helps them easily prepare for a comfortable retirement.

For more on our investment strategy, check out our blogs on our collaboration with BlackRock or, read more about how your savings are invested.

Want to check in on your pot? It's easy. Simply sign in to Penfold online or in our app to get a complete picture of your pension's performance right on your dashboard. You'll be able to see:

Data within this report is collected through a combination of self-reporting and through the use of data providers.

Where data was not available assumptions have been made based on what data could be collected.

Past performance does not guarantee future results.