How to Build a £1 million Pension Pot

Learn how to build a £1 million pension pot – from starting early and staying consistent to understanding risk and long-term growth.

Murray Humphrey

5 January 2026

7 min read

£1 million. In your pension.

For many people, that sounds wildly optimistic. But in reality, a good number of earners can reach a £1 million pension pot by retirement.

It’s not about luck or earning an enormous salary. It’s about starting early enough, staying reasonably consistent, and letting time do most of the heavy lifting. With the right approach, and a bit of patience, a million-pound pension pot is an achievable long-term goal.

In this guide, we’ll break down what a £1 million pension could mean for your retirement, and the practical steps that can help you get there.

Let’s start by grounding expectations.

£1 million is a lot of money – but the real benefit isn’t extravagance. It’s flexibility. A pension pot of this size gives you far more control over how much you take out each year, and how long your money could last.

A typical retirement is often estimated to last around 25-30 years. With a £1 million pension pot, withdrawing £50,000 a year through pension drawdown could, in simple terms, last around 36 years (ignoring investment growth or inflation for now).

A 2022 study by Which? found that two-person households spend roughly £28,000 a year to enjoy a “comfortable” retirement.

Similarly, the Retirement and Living Standards framework suggests:

That level of income typically covers everyday living costs, plus things like holidays, hobbies, eating out and the odd treat.

With an income closer to £50,000 a year, you’d have even more room for flexibility – whether that’s travelling further afield, upgrading your car more often, or simply enjoying extra peace of mind.

Very roughly, here’s how long a £1 million pension pot could last at different withdrawal levels:

Again, these are simplified examples – real-world outcomes depend on investment performance, inflation and how flexible you are with withdrawals.

If there’s one concept that matters more than any other when building a large pension pot, it’s compound interest.

Compound interest is essentially “interest on interest”. Your investments don’t just grow on what you put in – they grow on the growth itself. Over long periods of time, this creates a powerful snowball effect.

As Investopedia explains the longer your money stays invested, the greater the impact of compounding. In pensions, time is your biggest advantage.

This is very different from simple interest, which only applies to your original contribution. With compounding, growth accelerates the longer you stay invested.

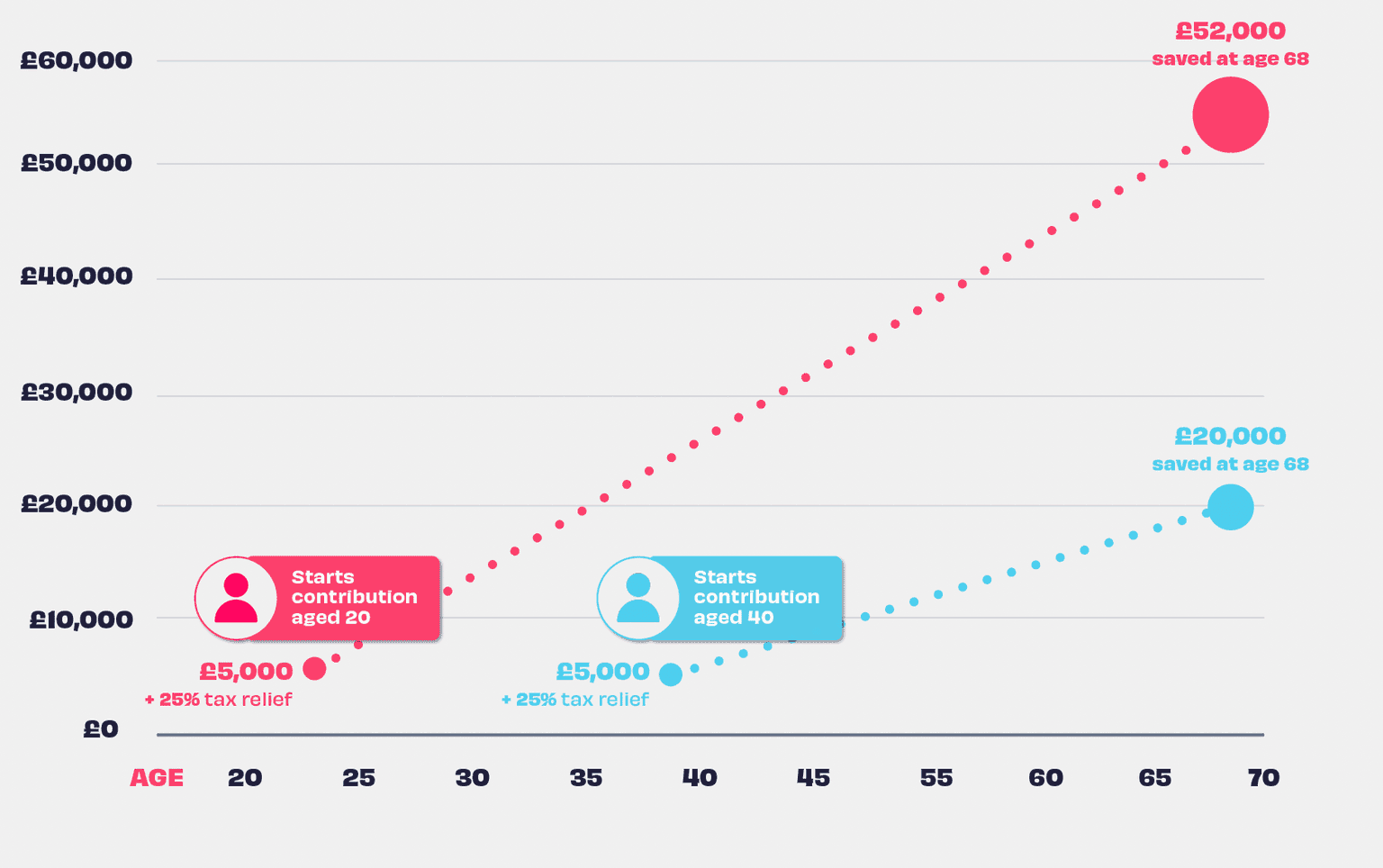

Here’s a simple example.

If you invest £5,000 into a pension at age 40 and leave it untouched, it could grow to roughly £20,000 by age 68 (assuming a 5% annual return).

Put that same £5,000 in at age 20, and by 68 it could be worth around £52,000, more than double, without adding a penny more.

Nothing clever happened here. The difference is time.

In reality, most people increase their contributions over their career and experience varying returns. But the message holds: the earlier you start, the harder your money works for you.

So what does this look like in practice? Let’s break it down.

You’ve probably heard the phrase: the best time to start was yesterday. The next best time is today.

The earlier you begin contributing, the more time compound growth has to work in your favour. Even small, regular contributions can make a meaningful difference over decades. And pensions give you a head start:

Waiting means missing out on this extra money – money that could be compounding for years.

Consistency matters more than perfection.

There will be years where you can contribute more, and years where you can’t. That’s normal. What matters is keeping the habit going and returning to it when things settle down.

Try not to compare yourself to others or write off “bad” years. Small contributions still count – and you can always increase them later.

Your attitude to risk plays a big role in how your pension grows.

Lower-risk investments tend to be steadier but may only keep pace with inflation. Higher-risk investments can fluctuate more in the short term, but they’ve historically offered higher long-term growth.

If you’re younger or starting later and aiming for a larger pot, holding some higher-risk investments may help – as long as you’re comfortable with ups and downs along the way.

There’s no single right answer. The key is choosing a strategy that lets you stay invested for the long term without panicking when markets wobble.

Early contributions are powerful, but later-life contributions often make up the biggest sums.

As your career progresses and your income rises, increasing your pension contributions can significantly boost your final pot. A good rule of thumb is to increase contributions whenever you get a pay rise – before lifestyle inflation kicks in.

You can usually contribute up to £60,000 or 100% of your earned income per tax year (whichever is lower), while still receiving tax relief.

If you’ve changed jobs, there’s a good chance you’ve built up multiple pension pots along the way.

Combining them can make it much easier to track your progress, manage your investments and understand how close you are to your goals. Many people also find it easier to keep fees under control with fewer pensions to monitor.

Fees matter more than most people realise. While investment returns rise and fall, fees are paid regardless. Over decades, even small differences in charges can significantly reduce your final pension pot.

Always check what you’re paying, particularly for older or forgotten pensions, and make sure the costs feel reasonable for the service you’re getting.

Finally, retiring later can have a surprisingly big impact. Working for a few extra years means:

It’s not an option for everyone – but even a short delay can make a meaningful difference.

A few rules are worth understanding as your pension grows.

You can usually receive tax relief on pension contributions up to your annual allowance of £60,000 or 100% of your earned income per tax year (whichever is lower). Contributions above this don’t qualify for tax relief.

If you haven’t used your full allowance in previous years, you may be able to use carry forward rules to make larger one-off contributions. We explain this in our guide to carrying forward your pension allowance.

There was previously a limit called the Lifetime Allowance, set at £1,073,100. This has now been fully abolished, meaning there’s no longer a cap on how large your pension pot can grow without facing additional lifetime allowance charges.

A £1 million pension pot isn’t a requirement for a comfortable retirement – and many people won’t need anything close to it. But it is a useful reference point that shows what’s possible with time, consistency and the right setup.

To maximise your chances, focus on:

Above all, break big goals into smaller, manageable steps. Pension saving is a long game – and progress adds up faster than you might think.

If you want a simpler way to stay on track, Penfold is an award-winning digital pension designed to make saving feel clear and manageable. You can:

Ready to start your journey to a £1 million pension pot? Create your free account today.