Auto enrolment rules

Auto-enrolment pension rules oblige an employer to set up an auto-enrolment pension scheme for their employees. Read our guide to learn the requirements.

17 May 2023

5 min read

If you’re an employer, you are obligated to set up an auto enrolment pension scheme for your employees. In this article, we’ll break down everything you need to know about setting up and managing an auto enrolment pension.

Put simply, auto enrolment is a pension set up by you, the employer, for your workers. Since 2012, all eligible employees have to be automatically enrolled into a workplace pension scheme. More on what constitutes an ‘eligible employee’ shortly.

Both you and your employees will need to contribute into their pension, up to the legal minimum of 8% of their pre-tax salary. Auto enrolment was introduced by the government to increase the amount of UK workers contributing into their pension.

Most workers in the UK will be eligible for an automatic enrolment pension. Which of your team you’ll need to enrol depends on:

The basics you need to know is this: if you are 22 or over and earn over £10,000 a year, you’re eligible for auto enrolment. There are a few exclusions to be aware of, including:

Every employee over 22 earning at least £520 a month must be automatically enrolled in your pension scheme.

Currently in the UK, employees won’t qualify for an auto enrolment pension scheme until they reach 22 years old. However, those aged 16 and above (or earning £6,240 a year and up) can also ask to be enrolled. If they do, you are legally obliged to set up and contribute into an auto enrolment pension for them.

The key to enrolling new employees into your pension scheme is the auto-enrolment date. This is the date that all employees must be enrolled and is the latest of:

Many employers chose to delay enrolling new employees until they have passed their probational period. You can therefore push back the date on which you enrol by up to a maximum of 3 months. You can also, however, choose to enrol new employees on their start date.

Here’s the main thing to remember. As long as the new employee is eligible, you have 6 weeks from their auto-enrolment date to enrol them into your pension scheme.

It’s also important to know that when you start contributing into an employee’s pension, you’ll need to make contributions from the given auto enrolment date - even if they did opt in at this point. This can mean you have to backdate contributions.

If you employ any temporary or part-time staff, you may still have to enrol them in your pension scheme. The question again comes down to are they an ‘eligible employee’, regardless of their employment status. If they are:

They’ll need to be enrolled into your auto enrolment pension, regardless of their employment status. Further, if they are under 22 but earn more than £10,000, they have the legal right to join your pension scheme if they ask. You don’t have to enrol them automatically.

You can delay the date you enrol an eligible employee in your pension scheme by up to 3 months.

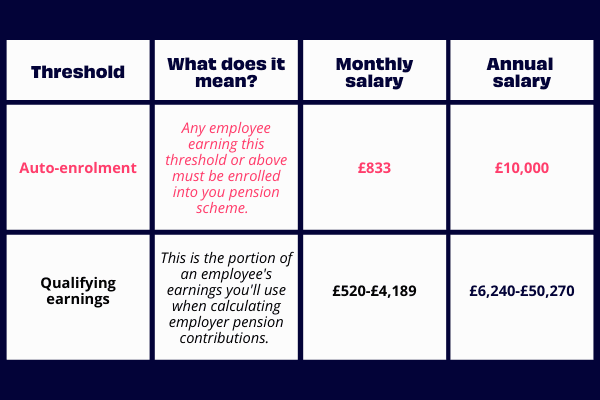

Auto enrolment pension thresholds impact:

It comes from establishing at what earning level employees qualify for auto enrolment, and how much of their earnings qualifies as ‘pensionable’ - i.e. how much of an employee's earnings you’ll use as the figure for a percentage pension contribution. The government Department of Work and Pensions reviews these thresholds yearly and makes adjustments to reflect the wider economy.

The auto enrolment rates for the 2022/23 tax year are below:

This affects the legal minimum you as a business will need to contribute into each employee’s pension. You can also contribute more, or use a different method of calculating pensionable earnings.

You may have also heard about salary sacrifice pensions in relation to auto enrolment. Here’s what you need to know. Salary sacrifice is not the same thing as auto enrolment.

Auto enrolment simply refers to the legal requirement for all UK companies to register eligible employees into their workplace pension scheme.

Very briefly, salary sacrifice is one method of processing employer pension contributions. It’s a way of reducing National Insurance liabilities for both the employee and employer. The other options are net pay and relief at source. Put another way, all salary sacrifice pensions are auto enrolment, but not all auto enrolment pensions are salary sacrifice.

For more on the benefits of salary sacrifice, read our What is salary sacrifice? Are you missing out? article.

Any employee who doesn't want to take part in your auto enrolment scheme will need to opt-out manually. There is no limit on who can opt-out (or when) - they'll simply need to let you know that they no longer wish to take part.

You'll no longer need to contribute into their pension unless they decide to re-enrol at a later date. The money in their pot at the time they opt-out will remain where it is, ready to access in retirement or to be transferred to another pension provider.

It's important to know that, as the employer, legally you need to offer every worker the chance to opt back into your pension scheme at least once a year. After 3 years, you'll need to re-enrol them back in your pension scheme automatically, as long as they're still eligible. If they still don’t want to be part of your pension scheme at this stage, you’ll need to manually opt them out again.