Pension re-enrolment explained: Your one-stop guide

Pension re-enrolment is a requirement for all UK employers. Here's everything you need to keep on top of pension re-enrolment, explained in plain English.

Frankie Dewar

9 May 2023

5 min read

In the UK, it's a legal requirement for all employers to re-enrol eligible employees back into their auto enrolment pension scheme. The auto re-enrolment pension procedure needs to be completed regardless of whether employees have asked to be re-enroled or not. In this article, we'll reveal how to stay compliant with the re-enrolment pension rules.

If you weren't already aware, every company in the UK has to provide a pension scheme - regardless of whether the employees want to enrol.

The same follows with offering an auto re-enrolment pension. Every 3 years, you must put eligible members of staff who have left your workplace pension back into the scheme (more on what eligibility means below).

Whether the employees have formally asked to get put back into your workplace pension scheme or not, you must complete a re-declaration of compliance to tell The Pension Regulator you've met the mandated duties.

Both re-enrolment and re-declaration are considered legal duties. Failing to act can result in a fine, which can escalate to a daily rate of £10,000.

Above, we briefly mentioned that you only need to re-enrol eligible employees to your workplace pension. Briefly, an eligible employee is anyone who meets the below auto-enrolment rules:

You can read more about who is (and who isn't) eligible for auto enrolment here. If any employees meet the above criteria, you need to re-enrol them into your pension scheme even if the employee says they don't want to rejoin. These employees will then need to manually opt-out again. However, there are a few exceptions that disqualify staff from re-enrolment. If an employee fits any of the criteria below, you don't need to re-enrol them into your auto enrolment scheme.

If an employee meets any of the above rules, you don't need to go through the process of pension re-enrolment. However, you should note that you still need to complete a re-declaration of compliance for The Pension Regulator.

You need to re-enrol all eligible employees back into your pension scheme even if the employee says they don't want to rejoin.

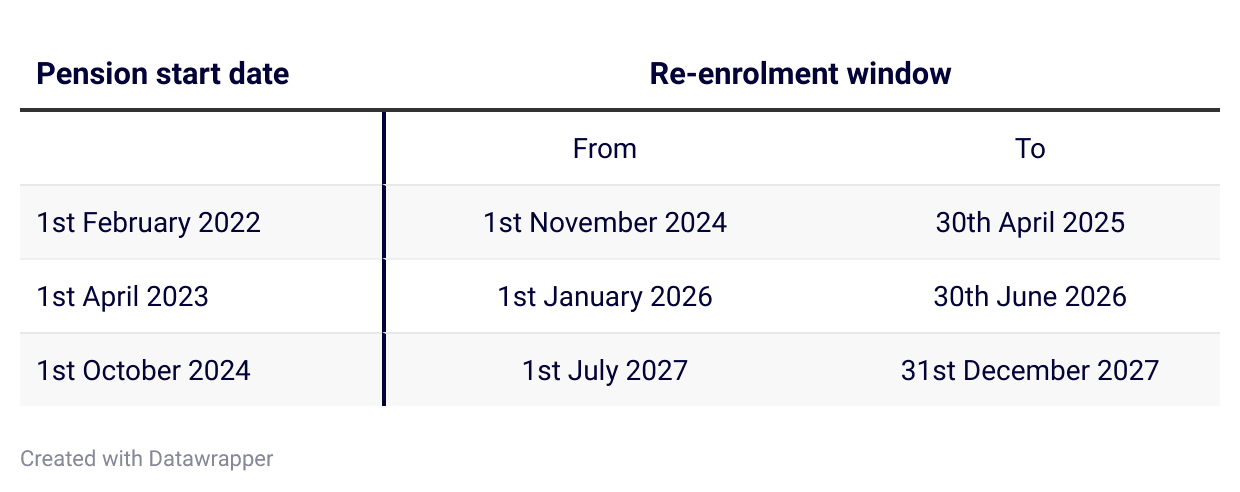

As an employer, your first re-enrolment date is set 3 years from your staging or (duty start) date. However, this isn't an exact date - it's a 6-month window. You have flexibility to choose any date between three months before or after your staging date. You can see an example of what this might look like in the table below.

If you aren't sure when your staging or duty start date was, you can find your dates for re-enrolment through The Pension Regulator's Find out your re-enrolment date range page by entering your letter code and PAYE reference.

The date you choose for re-enrolment must include all employees eligible within your 6-month window. When this date begins, you'll need to start making contributions to their pension pots again until they opt-out.

It's also important to remember that you cannot postpone your re-enrolment date beyond your 6-month window. Ideally, choosing a re-enrolment date that aligns with your payroll is best as this will enable you to match the start of your pay period.

Pension re-enrolment follows the same steps as normal auto-enrolment. Briefly, here's how it works.

Don't worry, finding your pension re-enrolment date and re-enroling staff is easy. By following the above steps, you can effortlessly re-enrol employees into a workplace pension and stay compliant. For more guidance, you can also check out our article on how to set up an auto enrolment pension.

Your first re-enrolment deadline is 3 years from your staging date.

After re-enroling eligible employees into your workplace pension scheme, you'll also need to declare compliance with The Pension Regulator again. You must declare compliance 5 months before either of the below:

Please note, you must re-declare compliance regardless of whether you need to re-enrol any employees or not. If you fail to do so, you could face hefty penalties.

On the The Pension Regulator's portal, they've made it easy to re-declare compliance. You'll just need to make sure you have the below information to hand.

Additionally, you'll need to supply the below information about your scheme:

Now you've read the above, you should comprehensively understand how pension re-enrolment works. This will help your company stay compliant with UK pension law. Keeping on top of re-enrolment is essential to reduce the chances of any penalties or fines which can reach up to £10,000 a day.

If you find managing your auto enrolment pension scheme daunting, you may want to consider switching to pension provider that does the hard work for you. Penfold is the award-winning auto enrolment pension scheme that employees love.

Request more information today to find out how Penfold can take the stress out of workplace pensions.