Pensions for self-employed savers

If you’re self-employed, pension contributions fall entirely on your shoulders. We’re here to help you save and grow wealth for your retirement.

Our pension is built for anyone who works for themself. Flexible contributions, automatic tax relief, a transfer service that does the paperwork for you and much more.

As with all investments, your capital is at risk.

Join thousands of self-employed pension savers

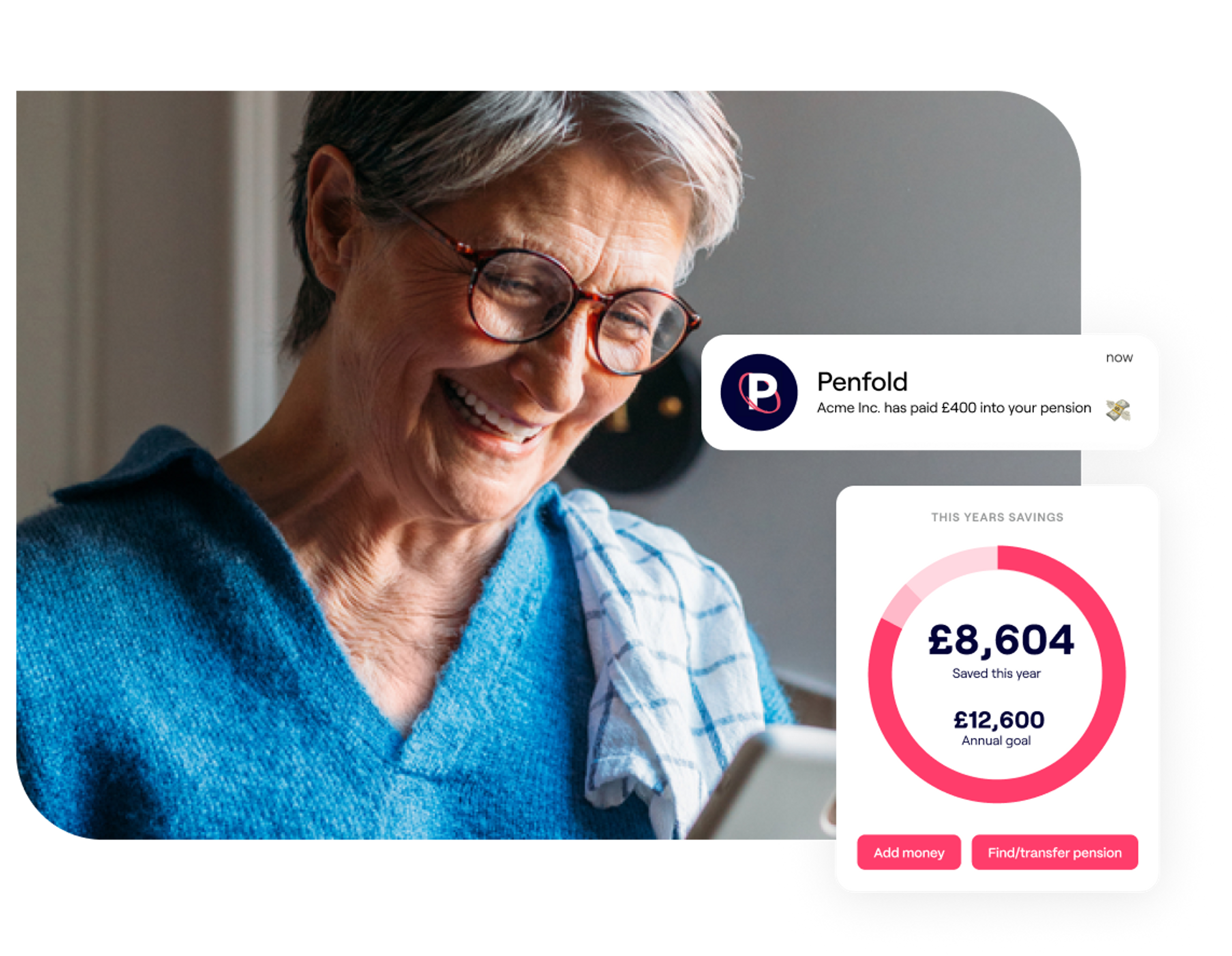

Relieve pension tension

Running a business likely leaves you short on time, in fact only 14% of self employed people are saving into a pension.

You might be focused on the day to day needs of your business, but it’s important to think about the future too.

That’s why we built a pension that only takes 5 minutes to set up and can be managed entirely from your phone, not only your web browser.

Sign up for free with your email address, a password and a few personal details to get started today.

Flexible contributions

Whether you’re a freelancer, sole-trader, contractor or anything that means you work for yourself; income and outgoings probably aren’t easy to forecast.

Penfold is designed to be as flexible as your finances are. Once you’re set up you can adjust, top-up, or pause payments at any time, instantly online or with our app.

Take advantage of tax relief

Self-employed workers get a 25% tax relief top-up on pension contributions. We organise it for you, automatically adding it to your pension.

If you're a company director you can pay into your pension through your limited company, contribute up to £60,000 each year and claim a reduction between 19-25% on your corporation tax bill. Find out more about arranging a director pension with Penfold.

Subject to annual allowance. Tax treatment depends on individual circumstances and may change in the future.

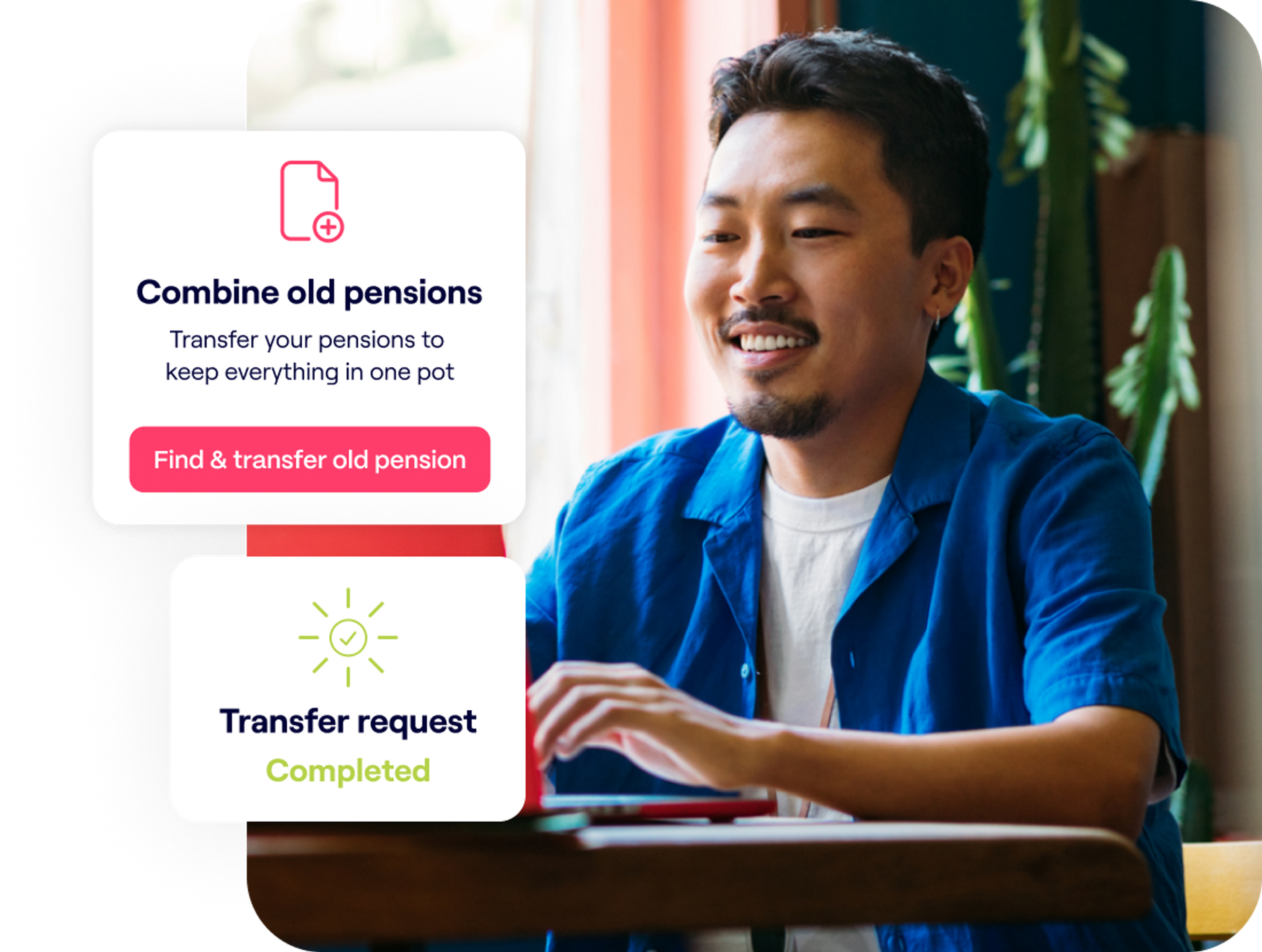

Transfer old pensions

Transfer and combine existing pensions into a Penfold account to simplify your finances.

All we need is the name of your pension provider(s) and policy number(s).

Alternatively, track down old or lost pensions using our Find My Pension tool. Simply enter an employer name and we'll find the contact details of the pension provider.

Consolidating pensions with Penfold is easy, free of charge, and our expert team of transfer specialists will manage it on your behalf.

It’s important to compare providers’ fees and any guaranteed benefits when deciding on whether to transfer, and be sure that the investments available are suitable for you. If your employer is paying into your pension currently, transferring that pot may mean you lose out on their contribution.

Hand-picked fund selection

Lifetime

Automatically adjusts investments to maximise early growth before protecting your pot as you approach retirement.

Lifetime planSustainable

Make a positive impact on the world without sacrificing growth. Invests your money into companies with a high ESG rating.

Sustainable planSharia

Invest your money only into Sharia-compliant companies. All investments are approved by an independent Sharia committee.

Sharia planStandard

Complete control of your pension. Choose between four different risk levels - tailoring investments to fit your preferences and outlook.

Standard planWith investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice and past performance is not a reliable indicator of future performance.

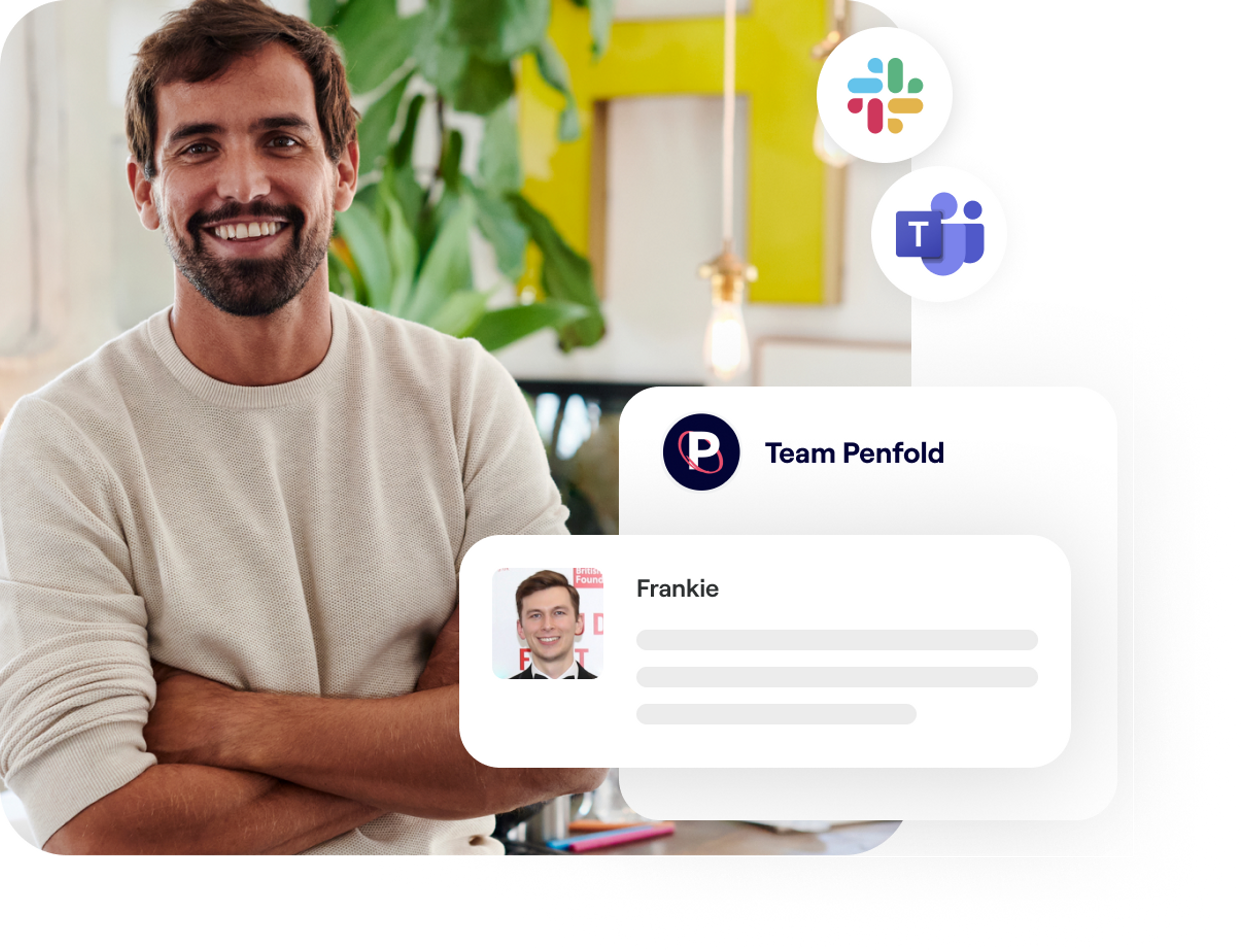

Friendly and helpful support

Our UK-based expert team are on hand to answer your pension questions. There are no waiting lines or call centres. Message us using the chat function on our app or website, email or call us any time.

We can even help you make pension withdrawals. Choose drawdown, an annuity or even take a lump sum in one go and enjoy a happy retirement.

If you’re interested in finding out more about pensions in general visit our Pension Guides section for more information about contributions, tax relief and much more.

Katherine's Story

Self-employed pension FAQs

Penfold is designed for maximum flexibility, so you can pause or stop your contributions at anytime, make one-off top-ups, or set up regular payments – whatever you like. There is no minimum deposit when you set up your pension, and you can pay nothing each month if you like. If you do make a contribution, the minimum amount we can process is £10.

We hate hidden fees and you probably do too. We'll only charge you one fair, transparent annual fee for managing your pension that covers absolutely everything within Penfold’s pension service.

You'll pay an annual fee between 0.75% and 0.88%, depending on the plan you choose. We'll automatically deduct a portion of your annual fee from your pension in 12 monthly instalments.

If your pension pot size is larger than £100,000 the fee is reduced to either 0.4% or 0.53%, depending on the plan you choose, on the portion of your savings over this amount.

Our platform is based on giving you pension peace of mind. We believe you should know your savings are being looked after, no matter what the future holds.

At Penfold we don’t hold or manage your money. Anything you pay into your pension with us first goes into a secure account held by a custodian bank. It’s held here for usually just one business day before being used to buy into your investment plan, managed by some of the world’s largest money managers.

Here’s an important thing to remember: Your savings are your savings. All of your pension is kept separate from us and belongs entirely to you. This means if anything were to happen to Penfold, your money can’t be touched by us or any of our partners. Your pot will be transferred to another pension provider, ready for your retirement.

With Penfold, the money you pay into your pension is invested. Your savings are used to buy a mixture of shares (part ownership in a company) and bonds (a loan with a guaranteed fixed interest rate) that will hopefully help your pot grow over time.

As with any investment, this involves risk. The value of your pension can go up as well as down, and you could get back less than you put in. However, greater risk can lead to greater returns. If you have a long time before retirement, investing over the long-term can help ease any short-term losses.

Once you reach 55 (or 57 from 2028 onwards) you can withdraw your Penfold pension. There's no restrictions with how you take your Penfold pension, you can go into drawdown, take a lump sum or as purchase an annuity.

The withdrawal process is entirely digital, so there's no hassle with forms on your behalf.

You can nominate a friend or family member to be the legal recipient of your Penfold pension if something happened to you, also known as a beneficiary. You can add, edit and change your pension beneficiaries in minutes on your Penfold account.

Penfold is a registered pension administrator, authorised and regulated by the Financial Conduct Authority (FCA), number 826097.

Penfold is also a part of the Financial Services Compensation Scheme (FSCS). In the very unlikely event that something were to happen to Penfold or our partners (BlackRock and Lloyds bank), the value of your pension is protected up to a maximum of £85,000 per individual.

We have appointed BlackRock and HSBC as your money managers, two of the biggest names in investment management.

The day-to-day management of your investments is done by these money managers who, although appointed by us, act independently of us, to try and ensure that your investments perform well.

As a digital pension provider, we understand that many people want to know how their personal information is kept safe.

To safeguard your data, we use the latest security technology and maintain strict internal practices every step of the way.

We also comply with General Data Protection Regulation (GDPR) guidelines. We'll never share your information with anyone else without asking you first.