Pension performance update: November 2022

What happened to pensions in November? Read our summary of investment markets across the globe and what it means for your savings.

Murray Humphrey

15 December 2022

8 min read

With the global stock market rising by 7.8% and government bonds increasing by 4.8%, November proved to be a month of recovery for capital markets. The gains came amid hopes that inflation in the US and Europe may have already peaked, anticipating a deceleration in the rise of interest rates.

Additional support for shares arrived from signs Beijing is relaxing some of its stringent Covid measures that recently hampered economic activity and provoked public unrest across different cities in China.

For pension funds, the recovery in November was a welcome reprieve after an otherwise tumultuous year.

Here’s a summary of the performance of the main indices in the UK and the US, including some other key indicators as well. You’ll also find an update on the performance of Penfold's pension funds.

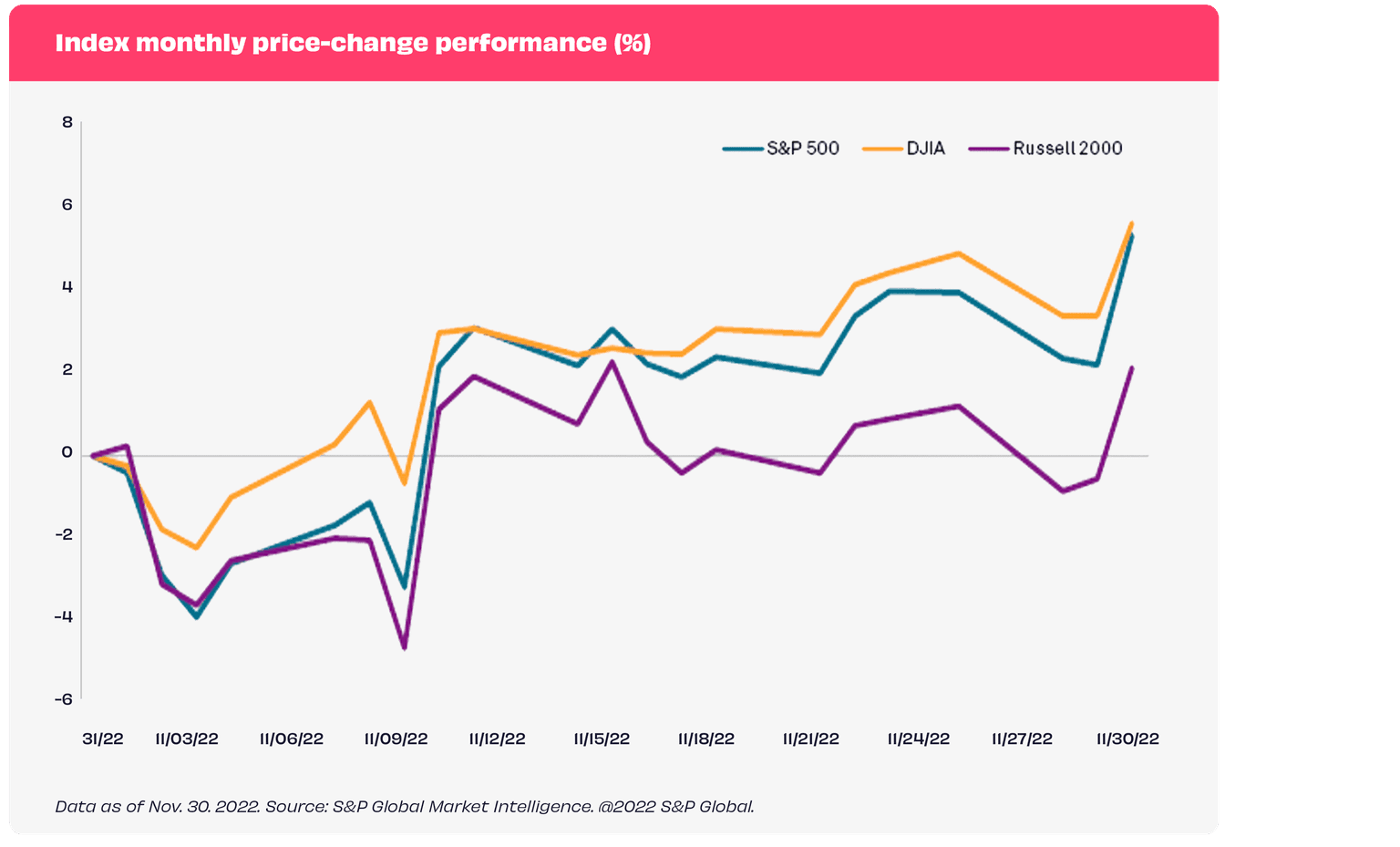

The stock market had a noteworthy month in November, with the S&P 500 closing up 5.4% and the Dow Jones Industrial Average increasing by 5.7%, while small-cap stocks lagged a bit behind, with the Russell 2000 increasing by 2.2%.

After a difficult start of the month, markets have rebounded on news that inflation is easing off from its record highs and that the Federal Reserve (Fed) may soon start slowing down its interest rate hikes.

Source: S&P Global

With North American companies accounting for a large portion of Penfold's pension funds, keeping an eye on their stock markets, and in particular, the S&P 500 - an index including the 500 leading US publicly traded companies - can give you an idea of how our funds are doing.

But, it should be taken just as an indication, given that our pension plans are all distinct, investing in a variety of markets with different risk-reward profiles to meet your investment goals.

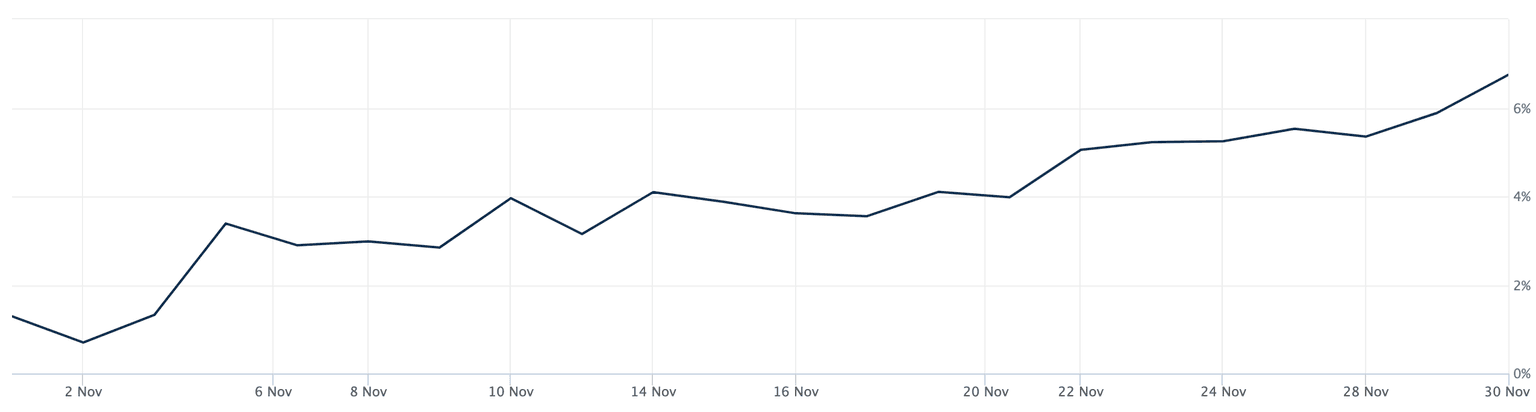

Yes, you read it right - it's not all doom and gloom after all. The UK's FTSE 100 index rose 6.7% in November, recording its best monthly performance in two years driven by commodity-linked and consumer stocks on hopes of Chinese demand recovery and easing domestic political concerns. Since the infamous mini-budget that caused markets to plummet on October 13th, the FTSE 100 has risen 12.9%.

Source: Wall Street Journal

Is this affecting your pension funds' performance? Yes, but with a limited impact, smaller than what we have seen above with the US markets. In fact, the portion of Penfold's fund made of UK equities is limited to a quota that goes from 3.75% to 12.5%, depending on which of the four plans you selected.

All in all, that's a relatively small influence, which can be viewed as good news, considering that a year of recession seems on the way. Indeed, in periods like this, having your savings invested into a well-diversified fund becomes particularly important for smoothing out any volatility.

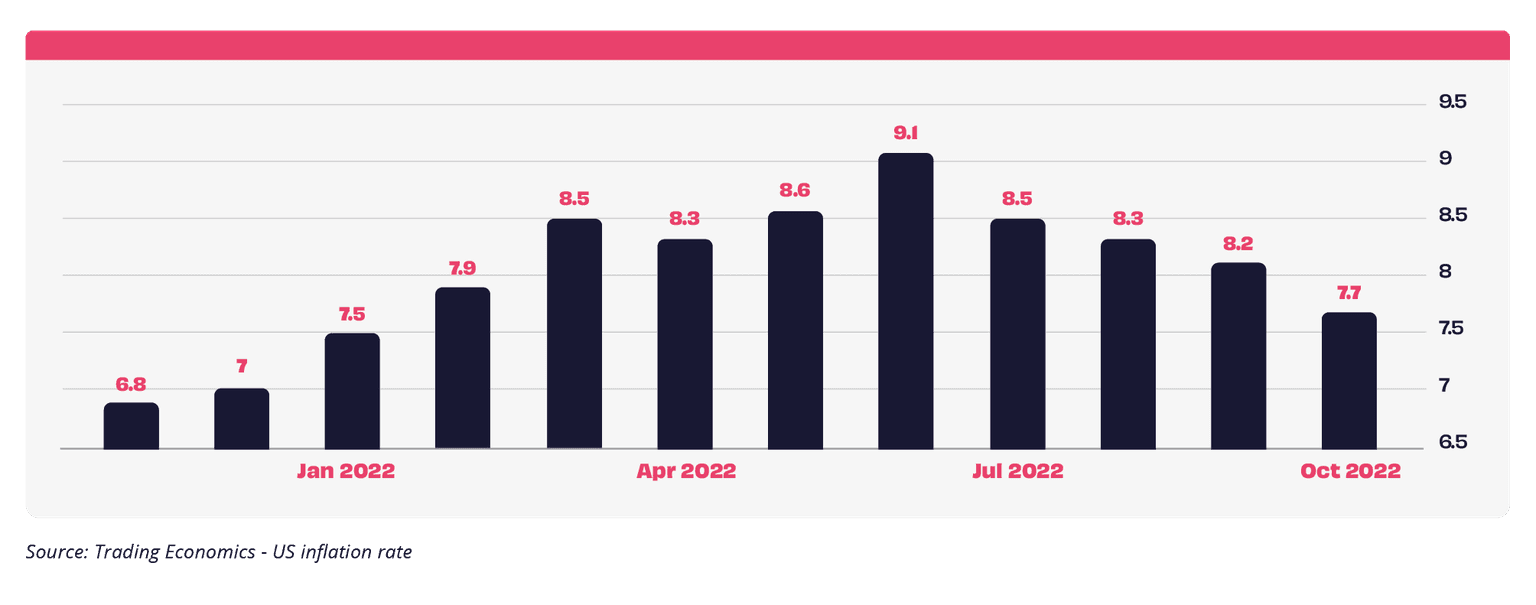

Rising inflation and increasing interest rates have significantly impacted this year's financial market performance. But, as we have seen, the most recent statistics comforted investors, who now anticipate that inflation will continue to cool down.

Looking at the actual data, the consumer price index (CPI) for the Eurozone showed that inflation lessened to 10.0% from October's year-on-year rate of 10.6%. Likewise, in the US, the annual inflation rate decreased for the 4th consecutive month to 7.7% - the lowest number since January and below the predictions of 8%.

A slightly different situation for us in the UK, as inflation is anticipated to rise further to 11.3%. To fight that, the Bank of England will probably increase interest rates by another 50 basis points, bringing the cost of borrowing to 3.50%. The good news here is that we may be finally near the peak.

The European Central Bank (ECB) and the Federal Reserve (Fed) are also expected to lift interest rates further - but at a slower pace than previously predicted, in light of the reassuring data related to inflation.

Another key November fact has been the update on the state of the economy, delivered by UK chancellor Jeremy Hunt via his Autumn Statement.

In summary, the government proposed a series of tax increases and spending cuts to face the current challenging situation. The changes will take effect in April 2023 and have long-term implications for UK workers.

Contributing to a pension is one of the best ways of reducing net income and if you want to know more about paying less tax then check out our guide on pension tax relief.

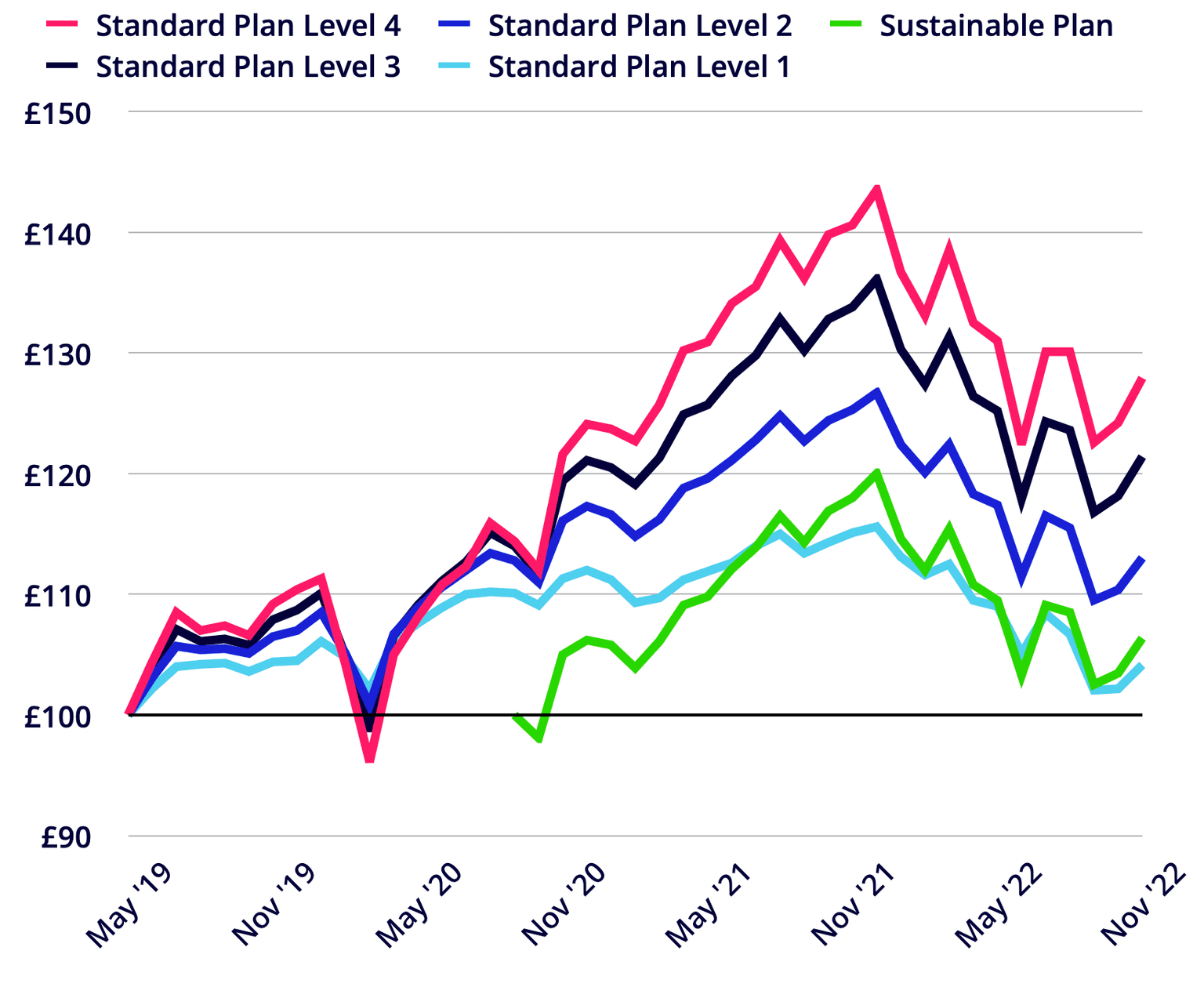

Overall, November has been a good month for Penfold’s funds. With global capital markets offering signs of recovery after a few tough months, most of our pension plans also rebounded from the slight decline experienced in October. The chart below shows what would have happened if you invested £100 into one of our plans at Penfold.

Source: BlackRock

Just looking at the past month, five of our pension funds increased in value. Of course past performance is not a reliable indicator of future performance. Ups and downs are absolutely normal and not something that should concern you on a month-by-month basis, as pension funds are long term investments and should be evaluated as such.

In fact, while it’s useful to keep an eye on your funds and understand why the valuations are increasing or decreasing, it’s also key to maintain perspective

With a recession in sight, interest rates and inflation rising, we can realistically expect some challenging months for the financial markets. However, how you should think about financial planning primarily depends on your situation, age and goals.

What if you are now close to retirement age?

In this situation, considering the current market volatility, it may be wise to start revisiting your retirement plans and exploring options for drawdown. In particular, here's what you can do:

1. Review your retirement plans in detail. Check if you are comfortable with the age or date of retirement and assess any risks associated with delaying it. Examine the implications for your benefits, pension entitlements and other factors that would affect your financial situation when planning to retire.

2. Check your forecasted pension pot size for your intended retirement date and decide if this will be enough to fund your desired lifestyle. Make sure you consider inflation rates and other factors that could impact the pot size in the future

3. Review all available options for pension drawdown. As a general rule, you can access most private pensions when you reach 55. If you have already reached that age, there are four main ways to access your pension savings: withdrawing your whole pension pot in one lump sum, withdrawing from your fund in smaller lump sums, using flexible drawdown to take out an amount that suits your needs, or purchasing an annuity which provides a regular income for a set period of time. The first 25% withdrawn from your pot is tax-free, while the remaining 75% is taxable.

Take a look here for more info and guidance.

But what if you are still early in your life and career?

That's a very different situation. While the immediate future may not look that bright, that shouldn't influence your long term financial planning too much. In fact, it's in these situations that long-term thinking becomes more important than ever, allowing us to focus on cultivating the investments that will be beneficial in the future. In other words, it's good to remember that your investment decisions today will set you up for success in the future—not just this month or next year, but way down the line.

In that sense, investing for your retirement when you're young might not seem the most exciting thing to do, but it's actually one of the smartest financial moves you could make. After all, time is on your side - and can be a powerful ally in helping you reach your saving goals.

Why it is key to start early:

1. You can take advantage of the power of compound interest for an extended time. The longer you save, the more your money earns from compounding returns, helping to grow your savings faster over time.

2. Investing in pension funds early on gives you access to investment options with tax advantages.

3. Even if you can't contribute a lot to your pension fund right now, adding small amounts over a long period is an excellent way to protect your money from the ups and downs of the market.

Last month's recovery was a welcome reprieve for pension funds after an otherwise rough year. But as we have seen, the global economy remains fragile, with markets likely to remain volatile in the foreseeable future.

As we approach the end of the year, we now have an excellent opportunity to look back at the past twelve months, assess how investments have performed and make any necessary adjustments to your financial plan, including your pension funds. Now is also the time to start planning and preparing for 2023, so you can set yourself up for financial success in the new year.

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.