Pension performance update: May 2022

Get the latest on the Penfold pension performance as economic markets continue their downward trajectory.

Murray Humphrey

30 May 2022

6 min read

The last few months have been a challenging time for investors. Rising inflation, supply chain issues, as well as the conflict in Ukraine have contributed to a widespread economic downturn. You may have also seen this reflected in the value of your pension.

While it can be concerning to see your savings dip, it's also important to not get carried away and to keep an eye on the bigger picture. Market downturns are a normal part of investing and while the near future appears to be more of the same, there is reason for optimism.

Here's what's happening with your Penfold pension and what (if anything) you should do next.

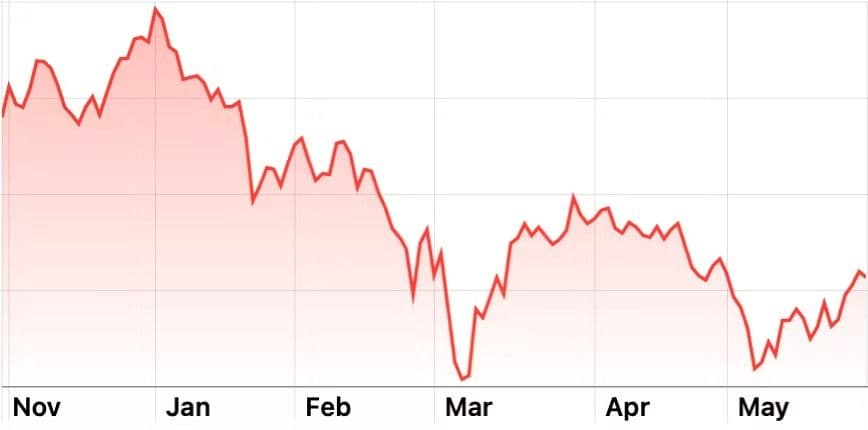

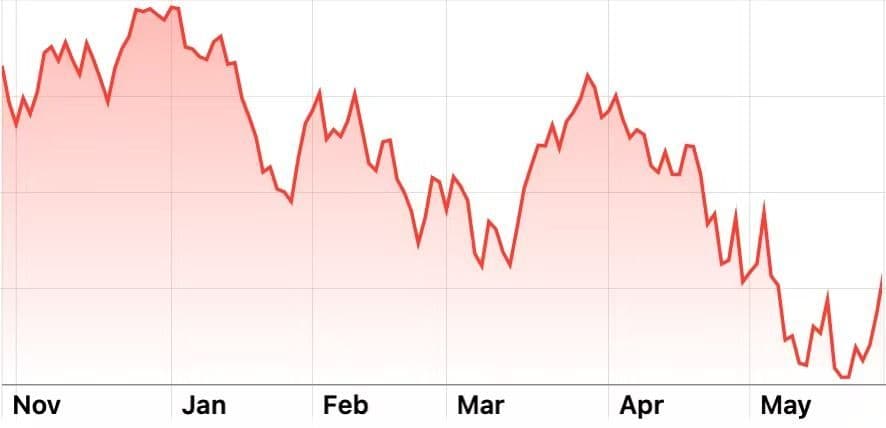

Since our last update, the negative headlines haven't gone away. The FTSE 250, the UK's stock market indicator, has been down by as much as 6% in May, although it has since largely recovered since the start of the month. It is down 9% over the last 6 months.

In the US, it's a similar story. The S&P 500 index dropped by 6% in mid-May, although has now also recovered to slightly higher than we were at the start of the month. The S&P 500 is also down 9% over the last 6 months.

Widespread and prolonged market decreases like these tell us that investors are cautious about the economic future. This is down to a mixture of the issues raised at the start of this article, namely:

A prolonged drop in the stock market usually tells us that investors are pessimistic about opportunities for growth. They sell these investments, moving their money into traditionally 'safer' assets like commodities, government bonds, or even cash. This then causes the value of the stocks and shares they've sold to drop.

Unsurprisingly, the widespread economic downturn is also being felt in our pensions. Regardless of which pension plan you selected, a portion of your pension is invested in the stock market. This means that when global markets drop, the value of your pension savings can drop as well.

At the moment, those invested in 'higher risk' plans with a larger portion invested into stock and shares may be experiencing more of a decrease than those who opted for a less volatile plan.

While this is of course disheartening, it's important to remember that this dip is being felt everywhere - you won't be the only one seeing a drop in the value of your pension over the last few months. Penfold savers, keep an eye on your inbox for a personalised breakdown of your pension's performance arriving in the next few days.

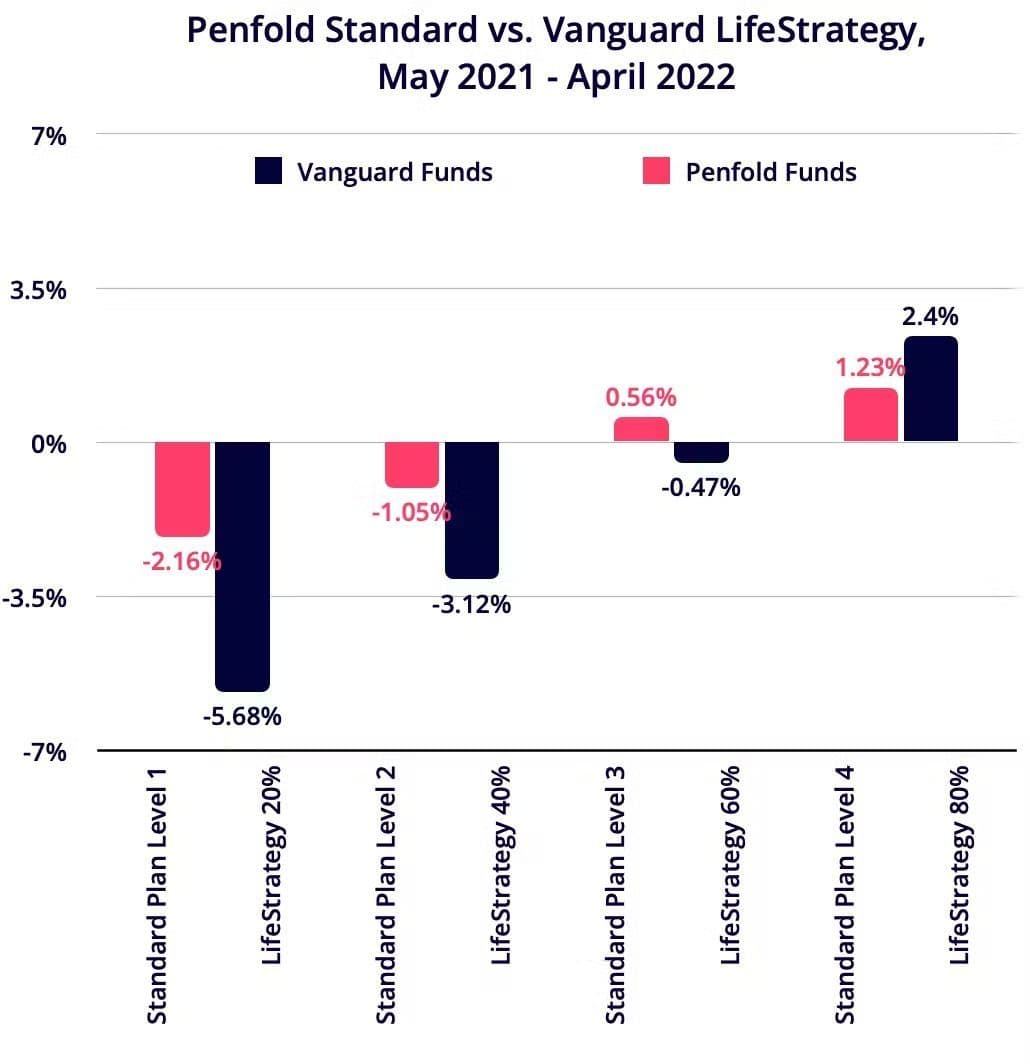

Of course, Penfold savers aren't the only ones seeing a drop in the value of their pension right now. In fact, our recent study revealed that the overall performance of Penfold's funds has fared better than other pension companies.

Past performance is not a reliable indicator of future performance.

Although your pension may be performing slightly better than some others, we of course acknowledge that a drop in pension value - regardless of the amount - can make you uncomfortable. So, what are we doing about it?

In response to the stock market downturn, we've worked with our money managers to rebalance our investments - bringing the risk of our plans down slightly. This is to balance the losses from equities in economies that have declined - whilst maintaining still enough exposure to benefit from a stock market rebound in the future.

For example, BlackRock (the money manager behind our Lifetime, Standard and Sustainable plans) have bought broadly in commodities while reducing exposure to European and Emerging Market equities. They've also increased Japan and US equity exposure as well as making a greater investment in less volatile assets like US & EU bonds.

When it comes to your pension, it's important not to panic. While it can be very alarming to see your savings decrease in value, that doesn't necessarily reflect how much money you will eventually withdraw from your pension, even if you're close to retirement.

If you were to consider transferring or withdrawing your pension right now, you'd only serve to make your losses real. Often, the best course of action is to do nothing, giving your pot enough time to recover from the drop in value. Remember, your pension is a long-term investment.

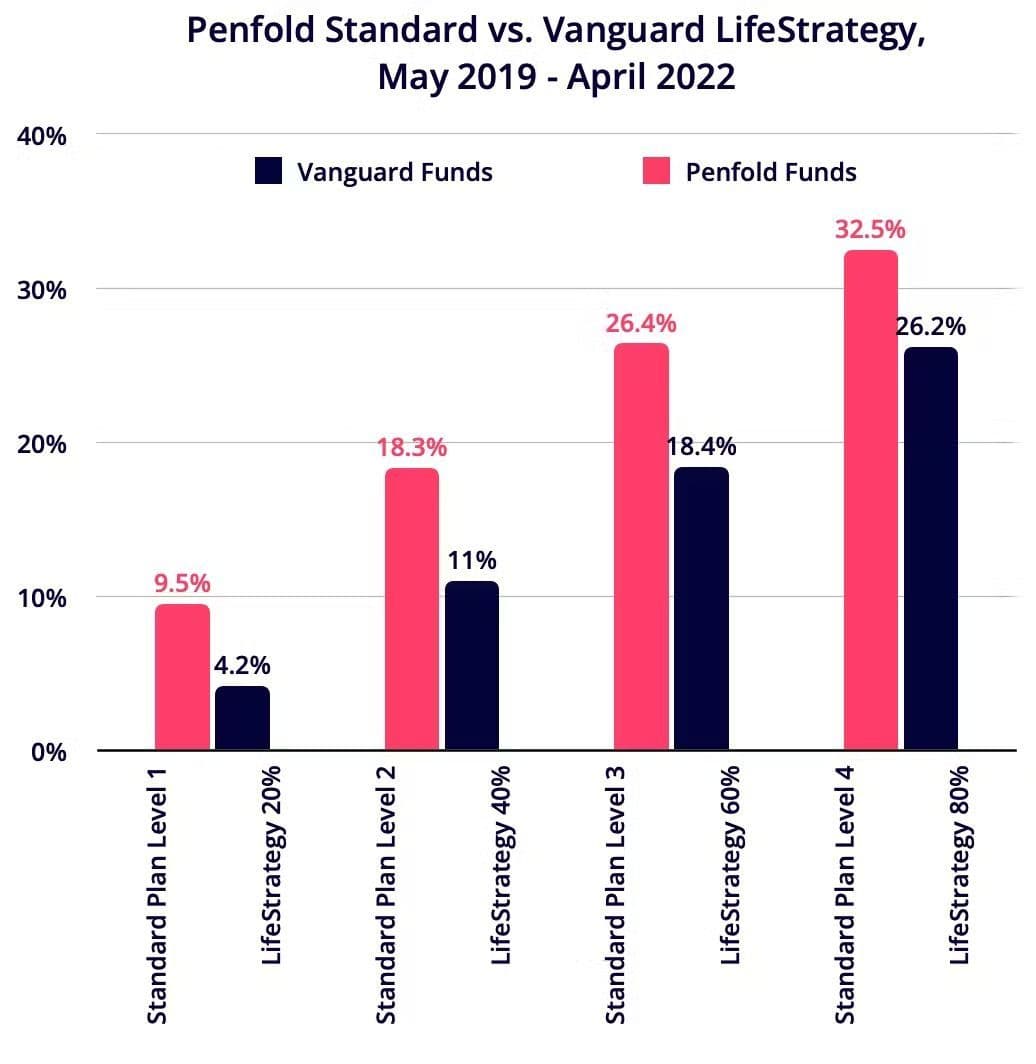

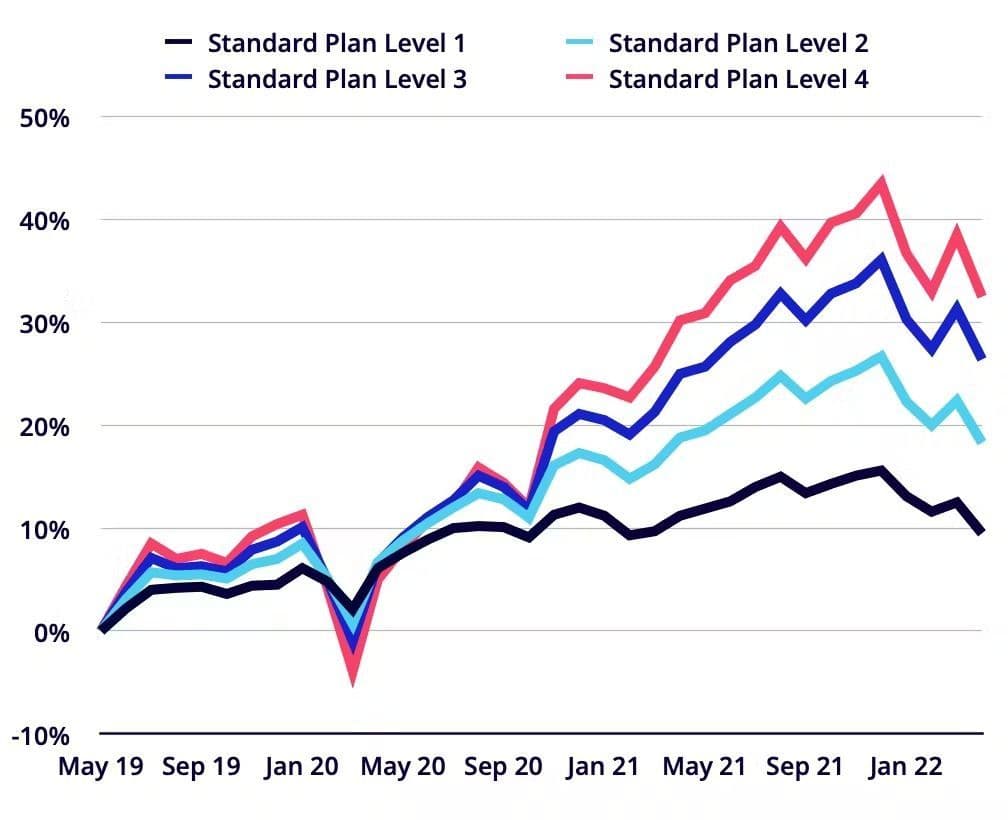

The chart above shows the performance of Penfold's pension plans over the last 3 years. As you can see, drops in value are frequent and expected - but withdrawing your money at this stage means you miss out on when the market recovers.

Past performance is not a reliable indicator of future performance.

For savers who are ready to access their pension, you may want to take another look at your retirement plan. Pushing back the date you access your pot, or even choosing to withdraw a little less now and rely on other sources of income will give your pot more time to recover, helping your money go further.

Of course, there is no guarantee that the situation will improve in a year's time - it's vital that you make a plan and weigh up how much you'll need to retire against when you'd like to stop working.

For more help on how to react to investment declines, checkout out our complete guide on what to do if your pension value has dropped. If you're worried about delaying your retirement, you can get free advice by speaking to Money Helper - a public body supported by the government.

Many UK savers will be rightly concerned by the performance of their pension right now. This is mainly due to the rising cost of living, widespread supply chain issues and the war in Ukraine. Please try not to be too concerned about any current decrease in the value of their pension if their retirement is still some way off.

At Penfold, we are working hard to balance the short-term impact of any drop in value against the opportunities for growth in the future.

Those close to, or already in retirement may want to consider delaying withdrawing from their pension to allow their pot to recover.

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.