2025 National Insurance Increase: How Salary Sacrifice Helps

Learn how the 2025 National Insurance increase impacts employers and why salary sacrifice pension contributions can help avoid rising payroll costs.

31 March 2025

4 min read

💡 Looking to cut National Insurance costs?

Penfold offers free salary sacrifice setup and support to help you save money and support your team.

Talk to our team or Get started free

Announced during the 2024 Autumn Budget, big changes are coming to employer National Insurance (NI) from April 2025 that will mean significantly higher payroll costs for many businesses.

But there’s good news: salary sacrifice pensions can help businesses soften the blow while helping employees grow their pension savings. Here’s why now is the time to consider salary sacrifice – and how Penfold can help.

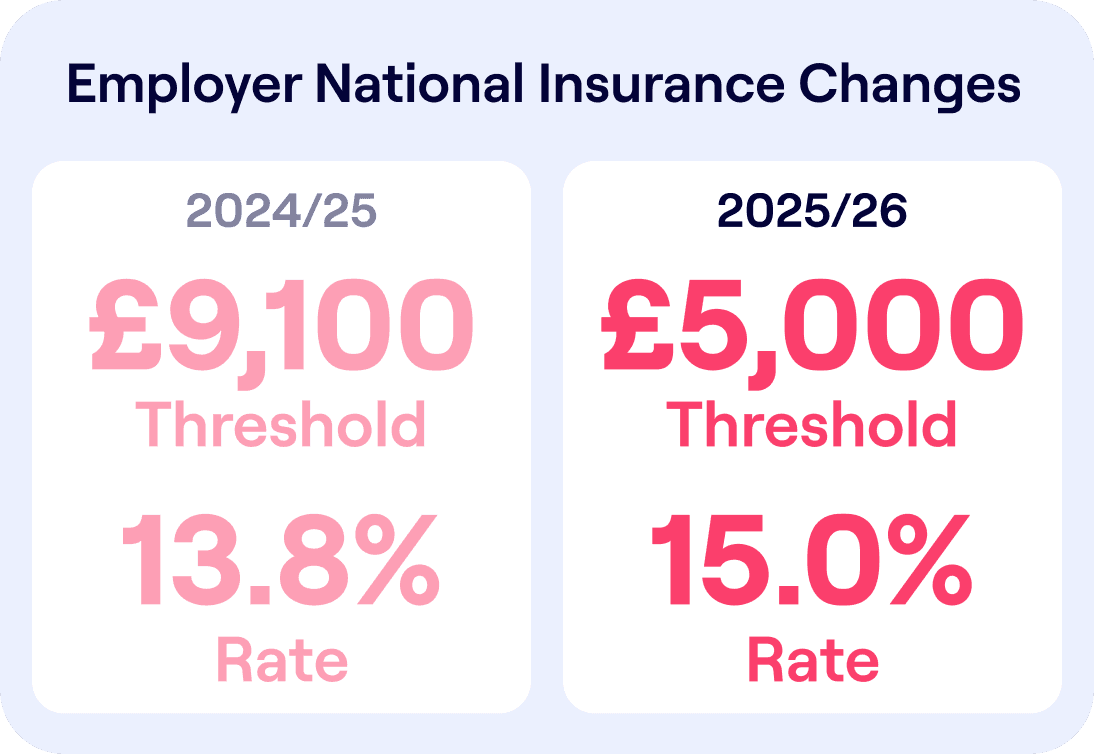

Let’s start with the facts – straight from HM Treasury. From 6 April 2025, businesses across the UK will face two major changes to employer National Insurance contributions, as outlined in the 2024 Autumn Statement:

These reforms are part of the government’s effort to raise an additional £25 billion a year to support public services and reduce debt. But for employers, they mean a steep rise in payroll costs – especially for businesses with larger teams.

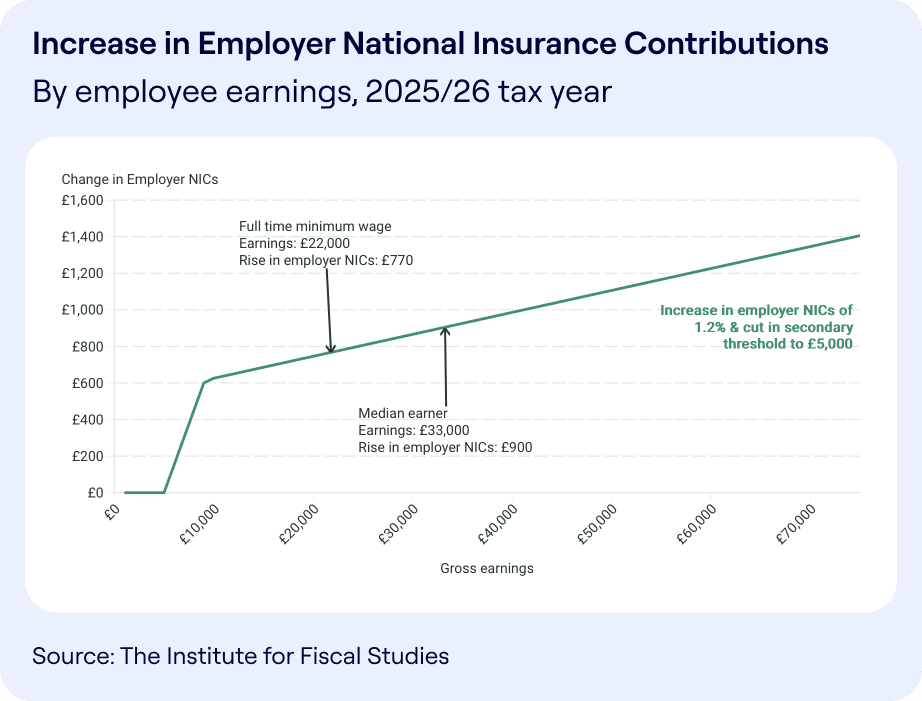

For many businesses, these new NI requirements represent a big increase in costs:

In short: you’ll be paying more NI on more of each employee’s salary – and at a higher rate. The cost impact could be thousands of pounds a year.

To help cushion this, the Employment Allowance will increase from £5,000 to £10,500 in April 2025, which will benefit some small businesses. But if your total Class 1 NI liabilities exceed £100,000 annually, this allowance doesn’t apply – so larger employers will still feel the full force of the hike.

This is where salary sacrifice comes in.

Salary sacrifice (also called salary exchange) allows employees to give up part of their gross salary in exchange for a non-cash benefit – like pension contributions.

Here’s why it’s a game-changer under the new rules:

It’s a rare win-win that’s both financially efficient and HMRC-approved.

With the upcoming NI increase, salary sacrifice provides a timely solution for businesses to manage increased NI costs while offering employees a tax-efficient way to grow their pensions.

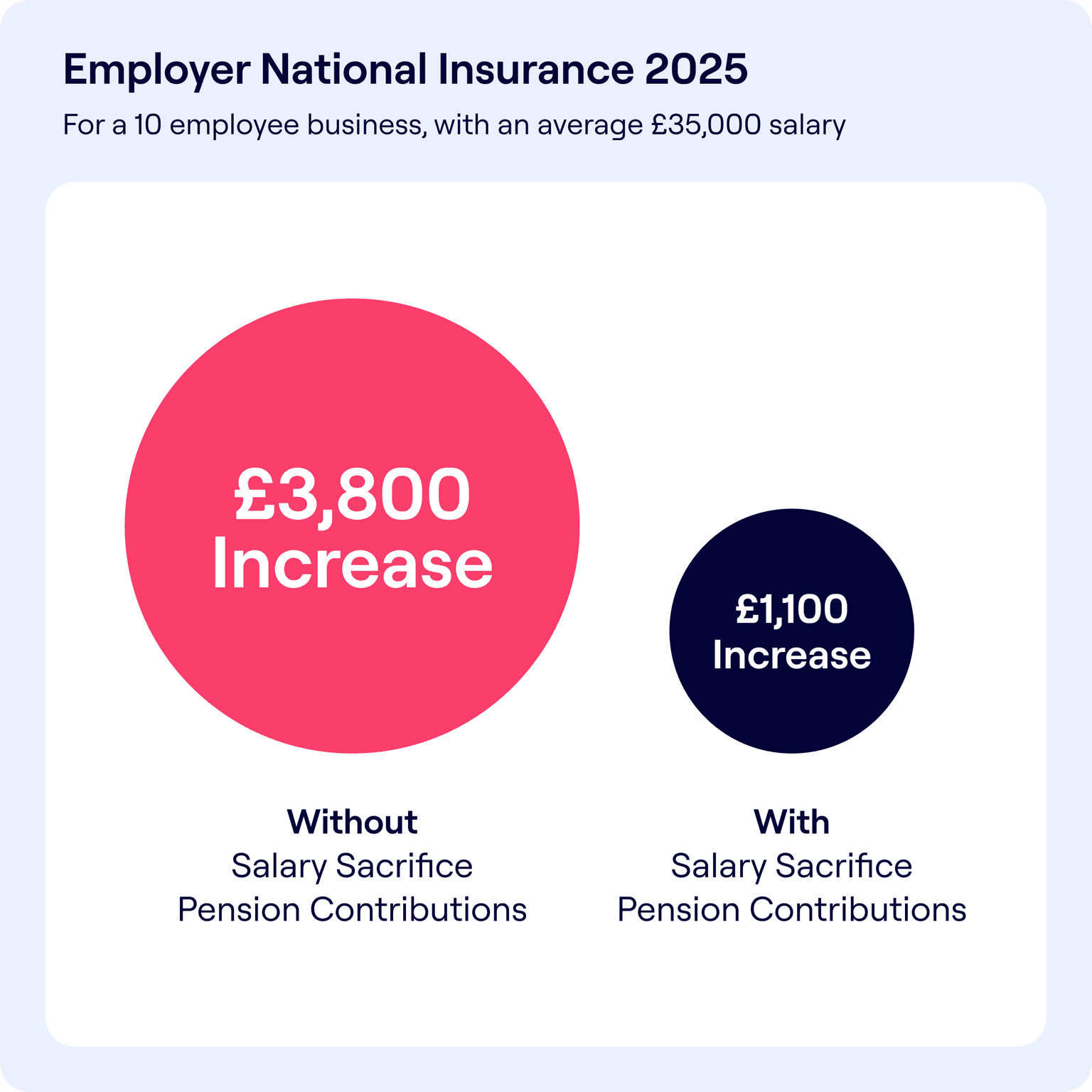

Let’s say you’ve got 10 employees, each earning £35,000.

That’s £2,700 saved. Every year. And that’s just one example. These savings scale with your workforce – and they only grow more valuable as NI rates rise.

Don’t just take our word for it. One of our customers, Capital on Tap, implemented salary sacrifice with Penfold and saved over £135,000 a year in employer National Insurance contributions.

“With the rise in employer National Insurance contributions, salary sacrifice has been a game-changer for us. By implementing it early with Penfold, we’ve been able to significantly reduce our payroll costs while continuing to invest in our people with their pension.”

— Fay Sumner, Head of People, Capital on Tap

Salary sacrifice doesn’t just help your business. It also helps your team:

It’s a tangible financial wellbeing perk, at zero cost to your employees – and minimal admin for you.

With the changes coming into force in April 2025, the best time to act is now. Switching to a salary sacrifice scheme means:

At Penfold, we help modern businesses turn pension saving into a strategic advantage. Our modern platform makes switching to salary sacrifice effortless:

We’re already helping hundreds of employers cut costs and boost pension engagement. Yours could be next.

Whether you’re switching from a traditional provider or just starting out, Penfold makes setting up a salary sacrifice workplace pension painless and powerful.