The Autumn Budget 2024: What Does It Mean for Your Pension?

Bigger pension payments. Changes in Inheritance Tax. And more! Find out how the budget will impact pensions for savers and employers.

31 October 2024

4 min read

We’ve boiled the Autumn Budget down into six things you need to know – specific to pensions, of course.

Find out four ways the budget will impact pensions for savers, and another three big changes for employers. Then explore how salary sacrifice can help benefit them both.

The government confirmed that Basic and New State Pension payments will increase by 4.1% from April 2025 to April 2026.

This increase is in line with the triple lock – which guarantees that pension payments will rise by the highest of earnings growth, inflation, or 2.5%. (This time around it’s risen by earnings growth!)

What about other benefits?

While this increase benefits pensioners – they’ll have 4% extra in their pocket every month – working age benefits won’t receive the same increase.

For example, Child Benefit, Universal Credit and Housing Benefit, will only increase with the Consumer Price Index inflation rate of 1.7%.

There’s no change in the amount of tax-free lump sum you can withdraw from your pension at retirement. You can still choose to take up to 25% of your pension as tax-free cash, capped at £268,275 over your lifetime.

Tax rates for pensions also haven’t changed. There was a rumour the government was going to introduce a flat rate of pensions tax relief. But basic-rate, higher-rate and additional-rate taxpayers will continue to receive the corresponding tax relief on their personal contributions.

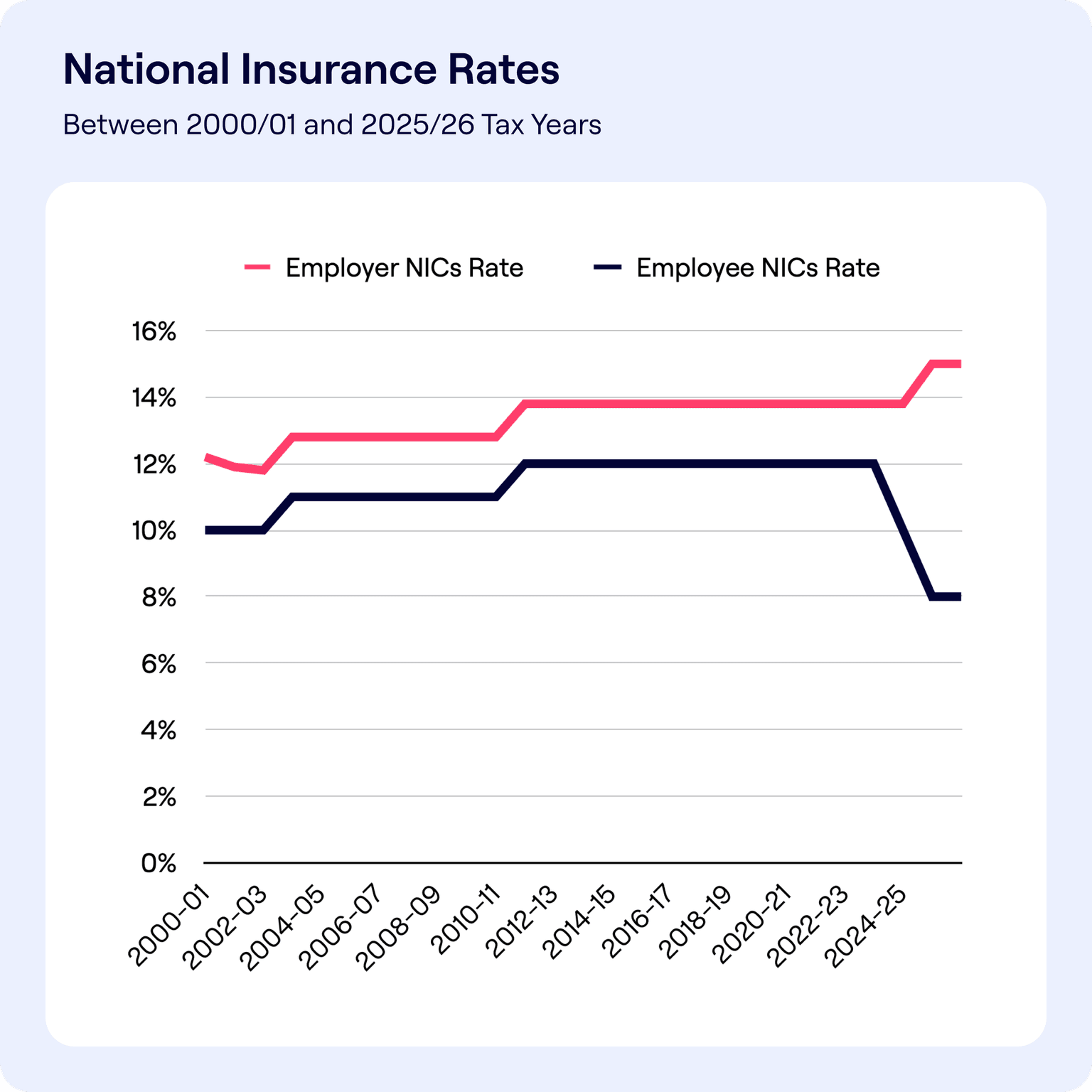

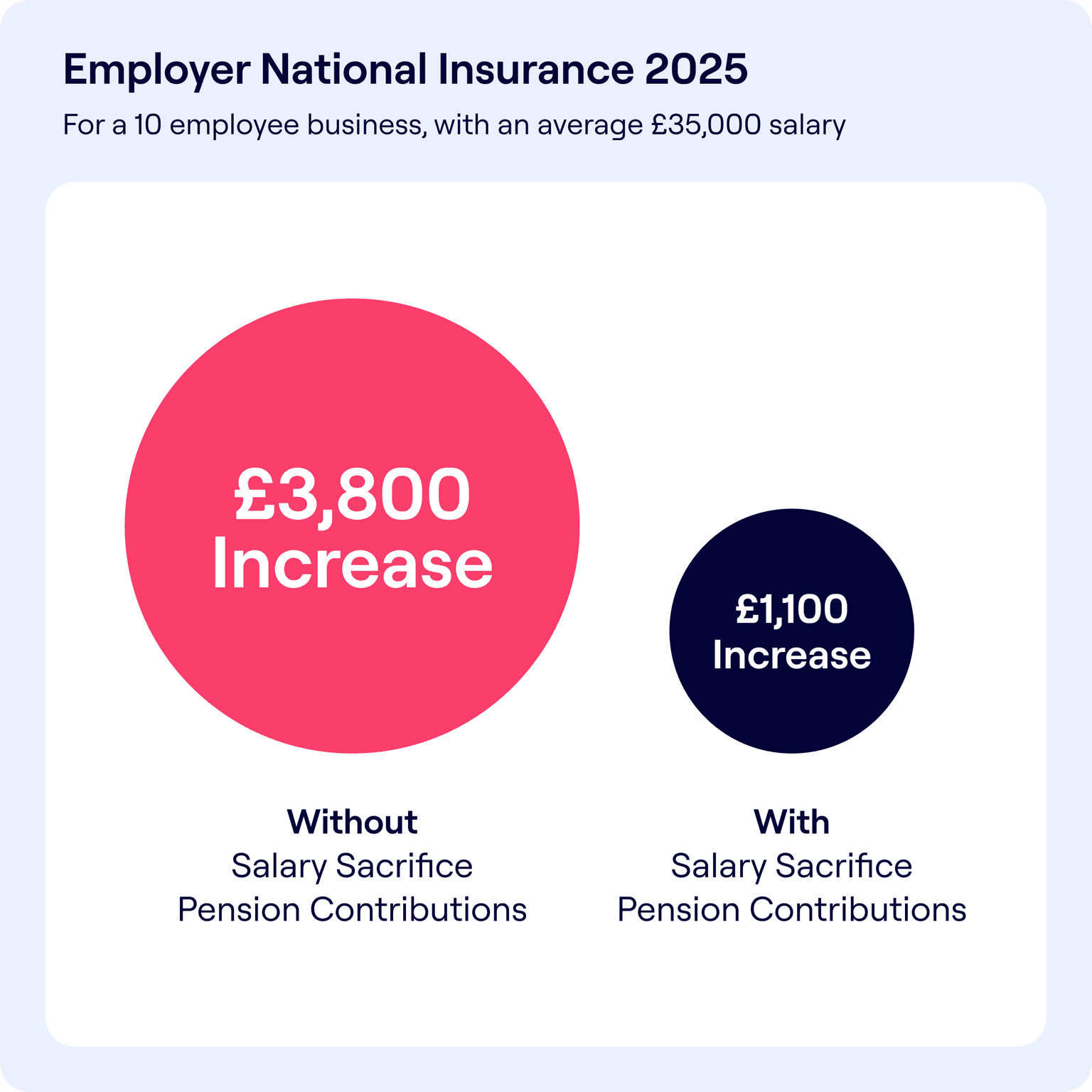

If you’re an employee, it’ll be useful to know that starting April 2025, the rate of employer National Insurance contributions will increase from 13.8% to 15%. And the tax threshold will be lowered from £9,100 to £5,000 per employee.

This increase means employers will pay more tax for each employee – but what could this mean for you?

Employers could introduce salary sacrifice, offering you the option to allocate a portion of your pre-tax income directly into your pension. This would lower your taxable salary, reducing NI contributions for you and your employer – while also boosting your retirement savings. (More on this for employer's later!)

Previously, pensions were often exempt from Inheritance Tax, but from April 2027 unused pension pots and death benefits will be subject to Inheritance Tax.

One way to respond? Make sure you spend it all!

It's important to note that Inheritance Tax only applies to estates worth over the threshold of £325,000 (or £500,000 for qualifying estates).

From April 2025, the rate of employer National Insurance will increase from 13.8% to 15%, with the threshold per employee lowered from £9,100 to £5,000.

Here’s a look at how National Insurance rates for employers and employees have changed over the years:

While National Insurance Tax rises for bigger businesses, to support smaller companies with rising costs the government has announced an increase in the Employment Allowance from £5,000 to £10,500.

This helps eligible businesses reduce the National Insurance they pay, meaning fewer small businesses will pay National Insurance Tax at all.

The main rate of Corporation Tax will remain at 25% on taxable profits over £250,000, and shouldn’t change again until the next election.

While this change mainly impacts bigger businesses, the certainty allows businesses to better plan for the future, helping them manage growth and investment more predictably.

At Penfold, it’s our mission to help savers secure a comfortable retirement – by supporting accountants, employers and individuals.

And don’t get us wrong, the Autumn Budget contains some pretty big changes, but also some big opportunities for individual savers and employers to improve the way they manage pensions…

A salary sacrifice pension scheme means employers can offset the increase in National Insurance tax, while employees can increase their take-home pay and save more for a comfortable life after work. It's better for everyone!

We offer free support to set up salary sacrifice for employers and accountants, helping individual savers and employers reduce National Insurance Tax, without reducing pension contributions.

Our team of salary sacrifice pension experts can help employers and accountants understand how it works, calculate potential savings based on head counts and finances. And we’ll be by your side all the way through with a straightforward switching process. Plus we also offer free Q&A sessions for employees!

We don't add this cost on anywhere else, either. Our pension scheme is free for employers and accountants, with just one fair, transparent annual fee for savers that covers absolutely everything within our service.