Reduce Employer NICs: Salary Sacrifice Pensions

The perfect pension for directors and limited companies

Running your own business can be stressful. Our pension is quick to set up and simple to use, helping directors and people running limited companies make tax-efficient contributions in line with cash flow anytime, anywhere.

As with all investments, your capital is at risk.

Join thousands of happy pension savers

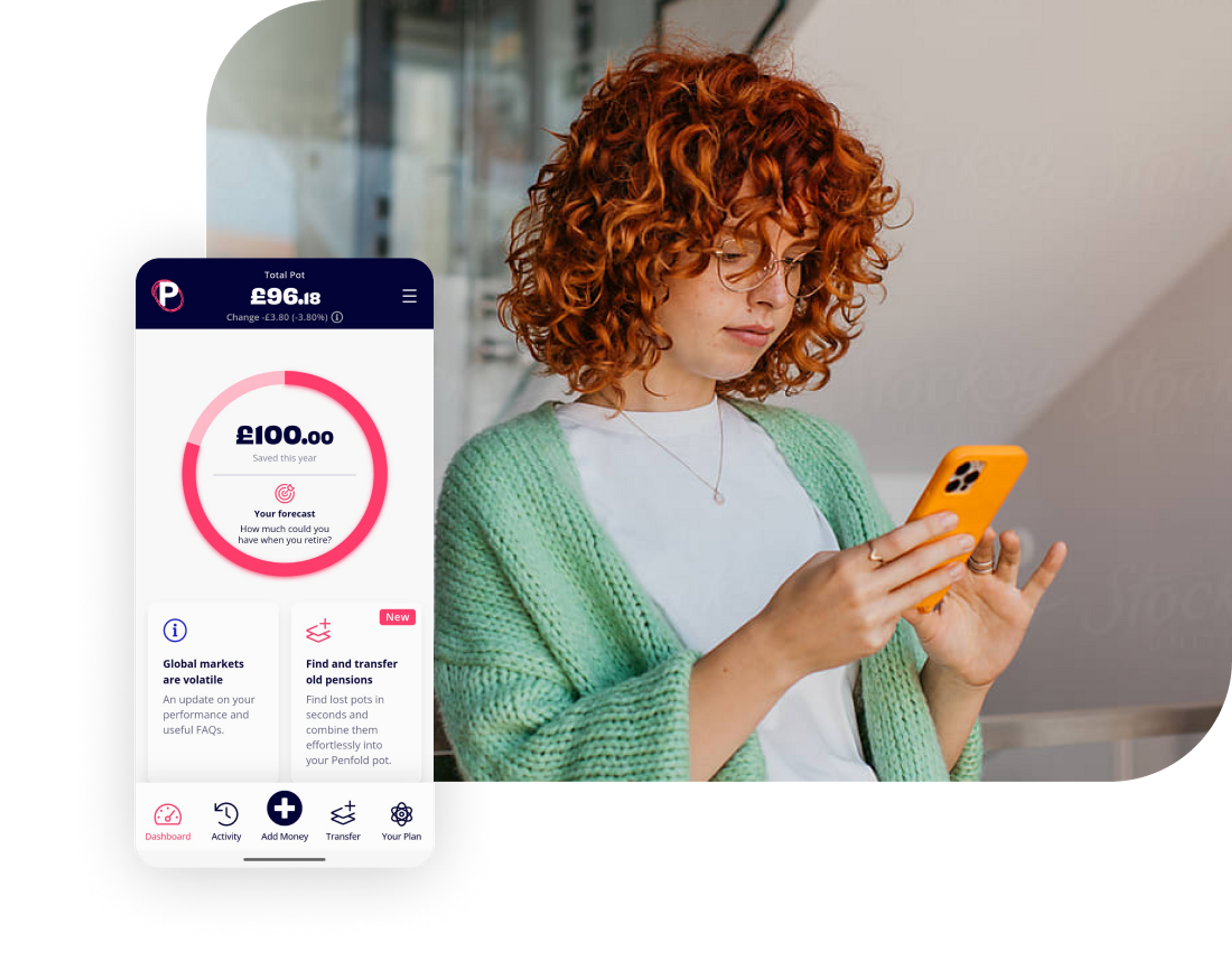

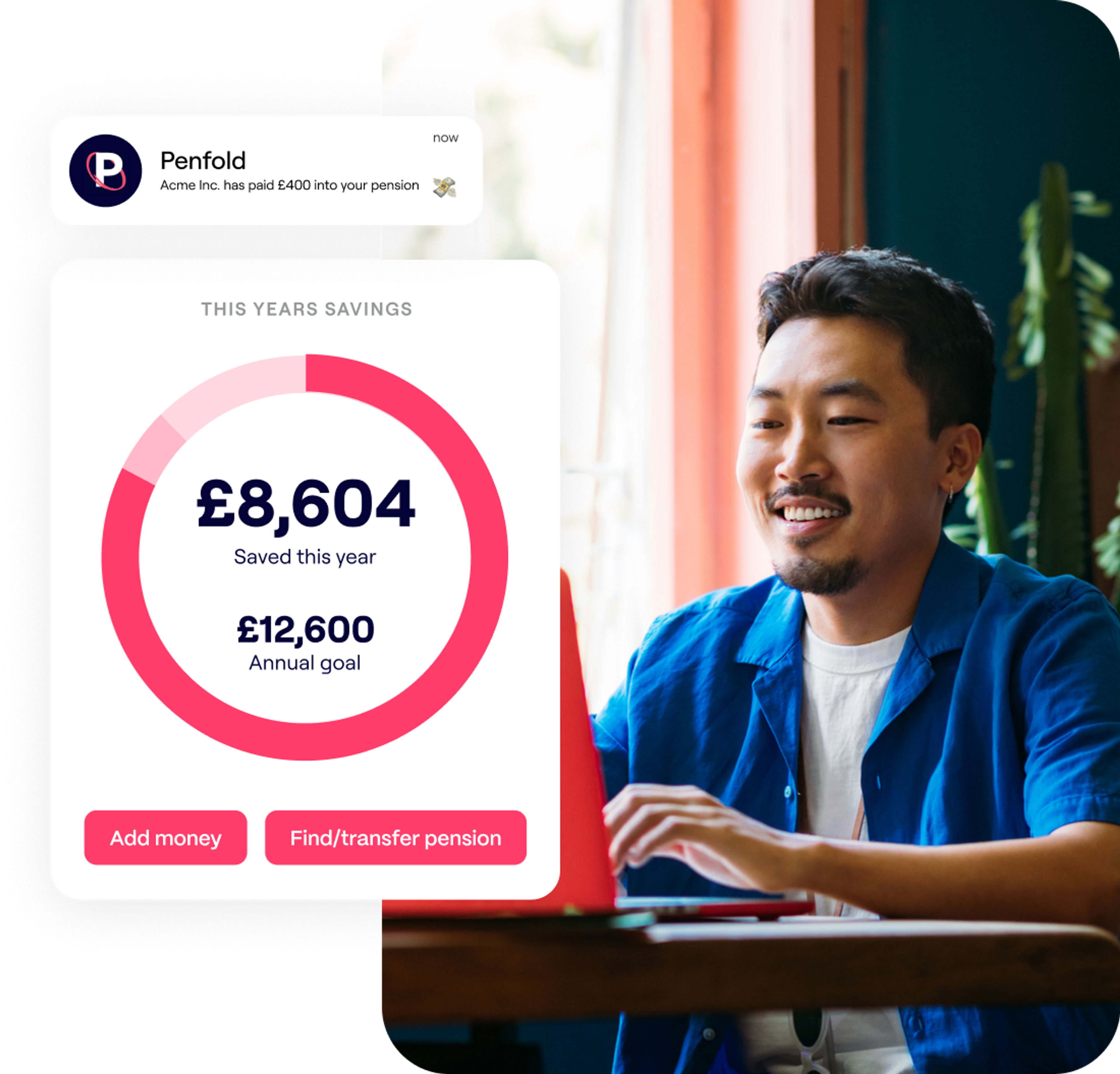

Optimise pension contributions

Make tax-free contributions: Pension contributions from your limited company are classed as a business expense, so you won't pay any tax on these contributions.

Save between 19-25%: Business contributions are deductible from your corporation tax bill. If your business makes a profit below £50,000 you can save the small profits rate of 19%. Therefore £1,000 paid into your pension cuts your tax bill by £190.

Use your allowance: For most people, pension contributions are capped at £60k or their yearly salary, whichever is lower. As a limited company director, your business can contribute into your pension without the salary restriction.

Tax treatment depends on your individual circumstances and may be subject to change in the future.

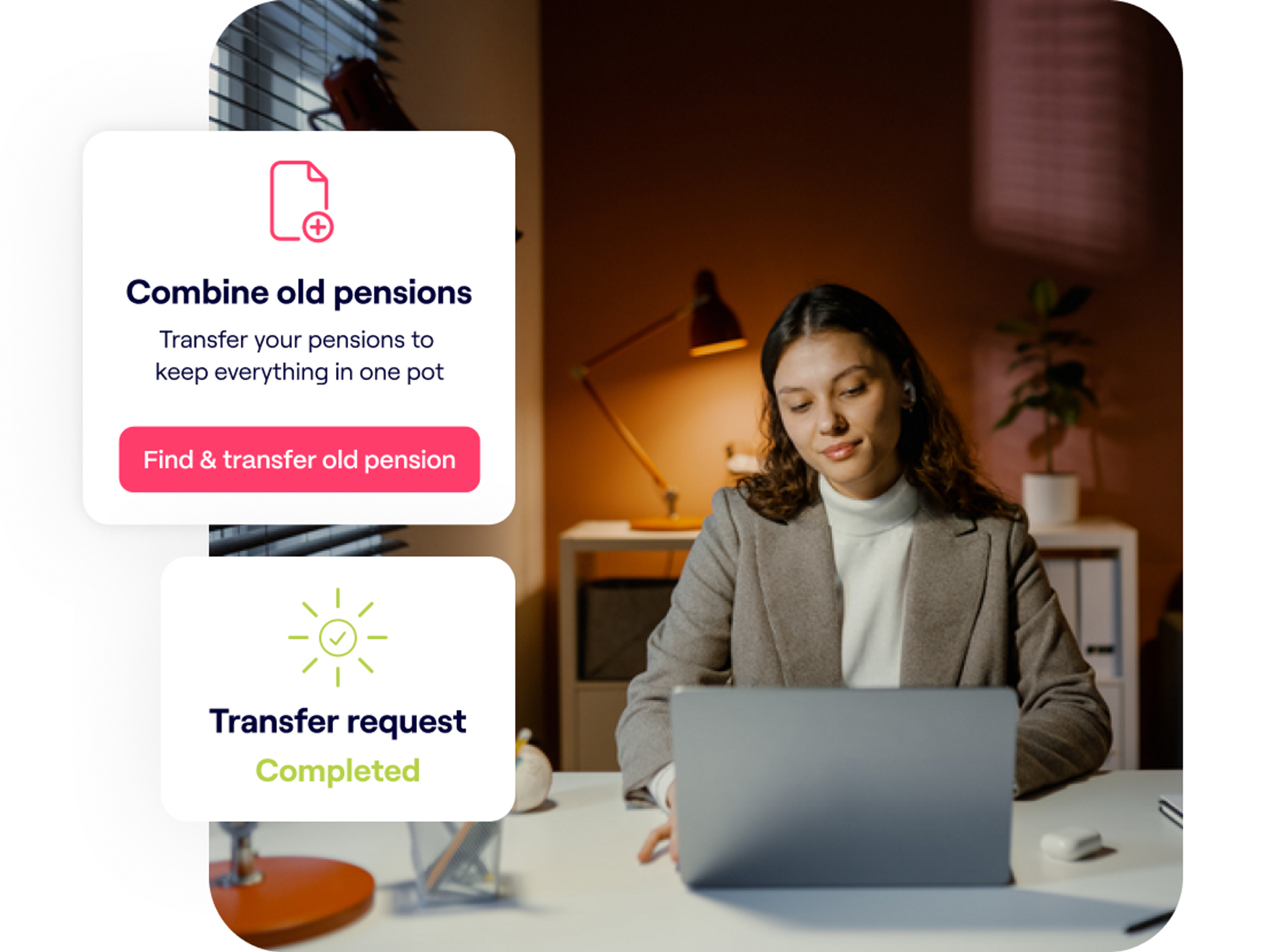

Combine old pensions

Transferring pensions to Penfold is easy, free of charge, and our expert team will manage it on your behalf.

Got old pension pots? Transfer and combine in a couple of taps by entering the policy provider name and account number. Our team of pension transfer specialists will do the hard work for you.

Missing pension details? Use our Find My Pension service to find the provider and contact details, all we need is the name of your previous employer.

It’s important to compare providers’ fees and any guaranteed benefits when deciding on whether to transfer, and be sure that the investments available are suitable for you. If your employer is paying into your pension currently, transferring that pot may mean you lose out on their contribution.

Friendly and expert support

Our UK-based expert team are on hand to answer your pension questions.

We've helped hundreds of company directors with their pension arrangements. Drop us a message on chat, email or call any time. No waiting lines or call centres.

We can even help you make pension withdrawals. Choose drawdown, an annuity or even take a lump sum in one go and enjoy a happy retirement.

Looking for more information about company director pensions? Read our dedicated director pension guide.

Hand-picked fund selection

Lifetime

Automatically adjusts investments to maximise early growth before protecting your pot as you approach retirement.

Sustainable

Make a positive impact on the world without sacrificing growth. Invests your money into companies with a high ESG rating.

Sharia

Invest your money only into Sharia-compliant companies. All investments are approved by an independent Sharia committee.

Standard

Complete control of your pension. Choose between four different risk levels - tailoring investments to fit your preferences and outlook.

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice and past performance is not a reliable indicator of future performance.

Director and limited company pension FAQs

You can pay into your Penfold pension through your limited company, which is known as a business, or employer contribution. Because employer contributions are an allowable business expense, you can offset pension contributions when you complete your Company Tax Return to reduce your corporation tax bill by between 19-25% dependant on your company profits.

To set up paying through business contributions, when you get to the final page of the set-up process, swipe the ‘business’ toggle.

The page will then prompt you to enter your limited company bank details and setup a Direct Debit with your business.

You can then adjust, pause and top up your pension through your limited company bank account via Direct Debit and bank transfer.

Usually the maximum amount a self-employed person can contribute into their pension is their total salary, if they earn less than £60k a year. However, as a company director paying into your pension, you can contribute the full £60k into your pension, regardless of your salary, and claim the 19% reduction in corporation tax on top!

Yes! As a Limited company director, you have the option to pay in through either or both business contributions and personal contributions with a Penfold pension. You can do this through regular and top up payments, via both Direct Debit and bank transfer.

Paying in through personal contributions means that your contribution will receive a 25% tax top up from the government. The government’s 25% tax relief is essentially paying back the income tax you’ve already paid on that contribution. For example, if you pay £100, the government will add £25. Tax treatment does depend on your individual circumstances and may be subject to change in the future.

We hate hidden fees and you probably do too. We'll only charge you one fair, transparent annual fee for managing your pension that covers absolutely everything within Penfold’s pension service.

You'll pay an annual fee between 0.75% and 0.88%, depending on the plan you choose. We'll automatically deduct a portion of your annual fee from your pension in 12 monthly instalments.

If your pension pot size is larger than £100,000 the fee is reduced to either 0.4% or 0.53%, depending on the plan you choose, on the portion of your savings over this amount.

Our platform is based on giving you pension peace of mind. We believe you should know your savings are being looked after, no matter what the future holds.

At Penfold we don’t hold or manage your money. Anything you pay into your pension with us first goes into a secure account held by a custodian bank. It’s held here for usually just one business day before being used to buy into your investment plan, managed by some of the world’s largest money managers.

Here’s an important thing to remember: Your savings are your savings. All of your pension is kept separate from us and belongs entirely to you. This means if anything were to happen to Penfold, your money can’t be touched by us or any of our partners. Your pot will be transferred to another pension provider, ready for your retirement.

With Penfold, the money you pay into your pension is invested. Your savings are used to buy a mixture of shares (part ownership in a company) and bonds (a loan with a guaranteed fixed interest rate) that will hopefully help your pot grow over time.

As with any investment, this involves risk. The value of your pension can go up as well as down, and you could get back less than you put in. However, greater risk can lead to greater returns. If you have a long time before retirement, investing over the long-term can help ease any short-term losses.

We have appointed BlackRock and HSBC as your money managers, two of the biggest names in investment management.

The day-to-day management of your investments is done by these money managers who, although appointed by us, act independently of us, to try and ensure that your investments perform well.

Penfold is a registered pension administrator, authorised and regulated by the Financial Conduct Authority (FCA), number 826097.

Penfold is also a part of the Financial Services Compensation Scheme (FSCS). In the very unlikely event that something were to happen to Penfold or our partners (BlackRock and Lloyds bank), the value of your pension is protected up to a maximum of £85,000 per individual.

As a digital pension provider, we understand that many people want to know how their personal information is kept safe.

To safeguard your data, we use the latest security technology and maintain strict internal practices every step of the way.

We also comply with General Data Protection Regulation (GDPR) guidelines. We'll never share your information with anyone else without asking you first.