New feature ✨ Your Forecast

Your Forecast helps Penfold savers predict their income in retirement. Here's how it works.

Murray Humphrey

14 September 2022

8 min read

Not sure what your pension will look like when you retire? You're not alone. When asked, 77% of savers didn’t know how much they’d need to retire. This makes it nearly impossible to work out what you should do with your pension today. It's difficult for savers to know if they're contributing enough, or the real impact of increasing (or cutting back) their pension contributions in 10, 20 or 30 years' time.

Even trickier is trying to work out what kind of lifestyle you can look forward to. At Penfold, we wanted an easy way for our savers to understand what their retirement might look like and take action today. So, we're launching a brand new tool to help Penfold savers get a clear picture of their financial future. Introducing Your Forecast.

Your Forecast gives you a personalised forecast of what your pension will look like when you retire. Launch Your Forecast from your app or online dashboard to calculate your forecast instantly. You'll see how much income you can take from your pension each year, based on:

Your forecast is calculated automatically - no complicated questions or maths required! You can also adjust your age, contributions and more to see how it will impact your retirement income. More on that in a moment.

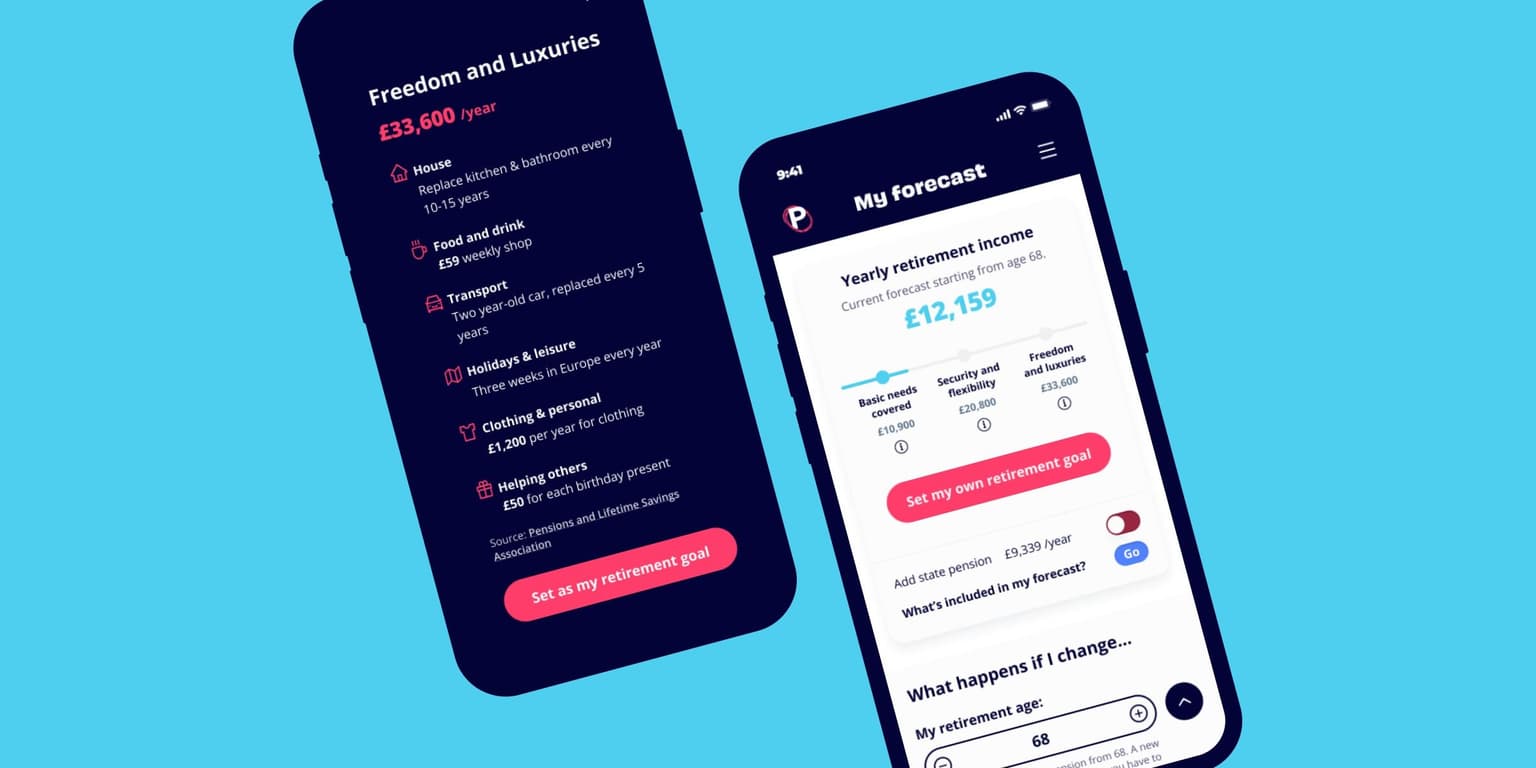

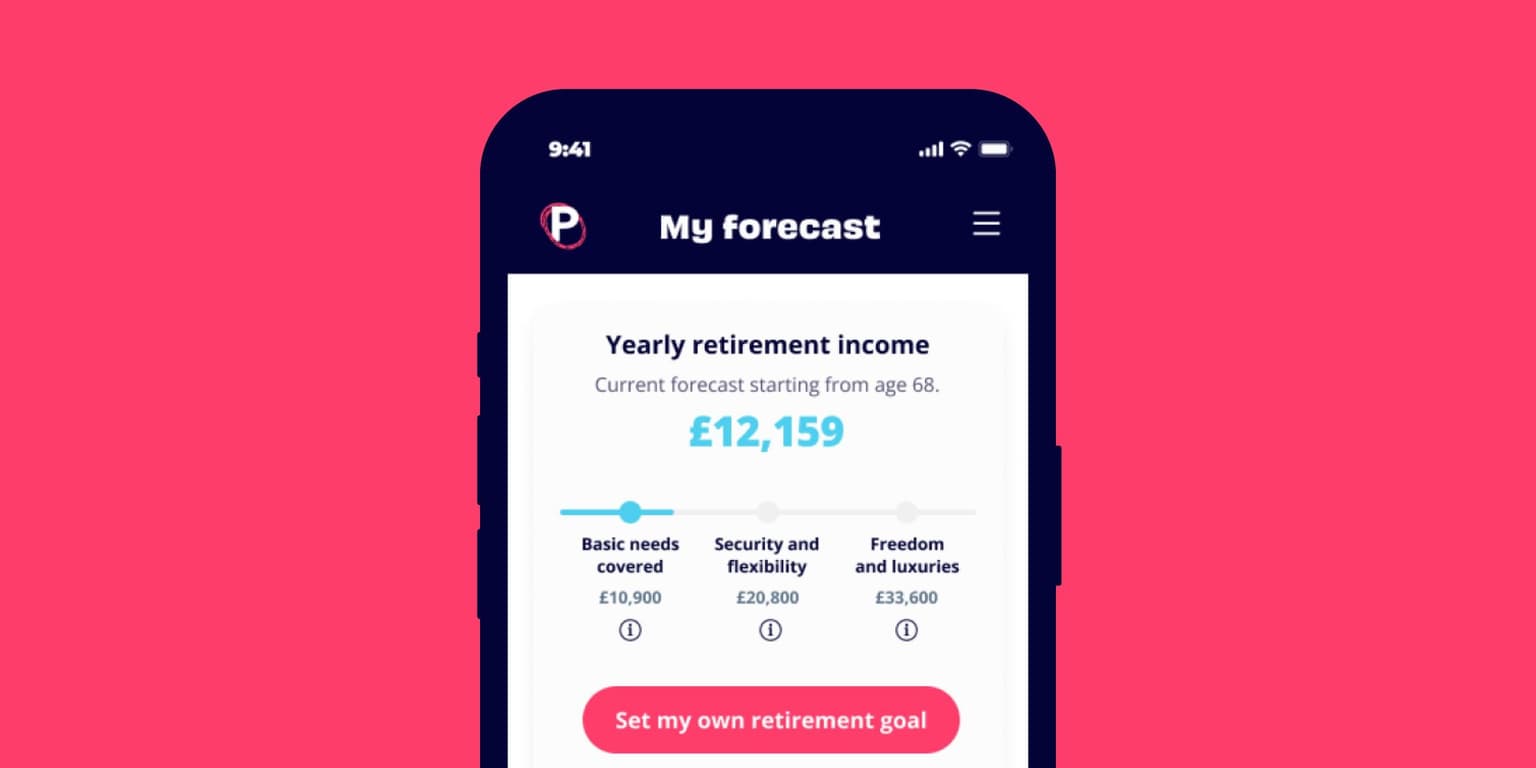

To help you understand your forecast, we've also provided three lifestyle categories to benchmark your retirement income against - to understand what the value of your pension pot will mean in real terms. These are a rough guide of how much you'll need in your pension to afford a good quality of life in retirement, based on research from the Pensions & Lifetime Savings Association (PLSA).

For more on planning your contributions, check out our complete guide to how much you should pay into your pension.

Your Forecast is designed to be powerful yet simple. To get started, all you need to do is sign in to your Penfold account and tap the Your Forecast icon inside your Yearly Target Donut. You can also access the feature by hitting the Your Forecast tile.

This will give you your current predicted yearly income in retirement, along with some information about how this figure was calculated. Of course, for a more accurate picture, we'll need a few bits of information from you. Here's how you can configure your personal pension forecast.

The number you'll see at the top of your screen is your forecasted retirement income. How much you'll be able to withdraw from your pension each year, starting from the age of 68.

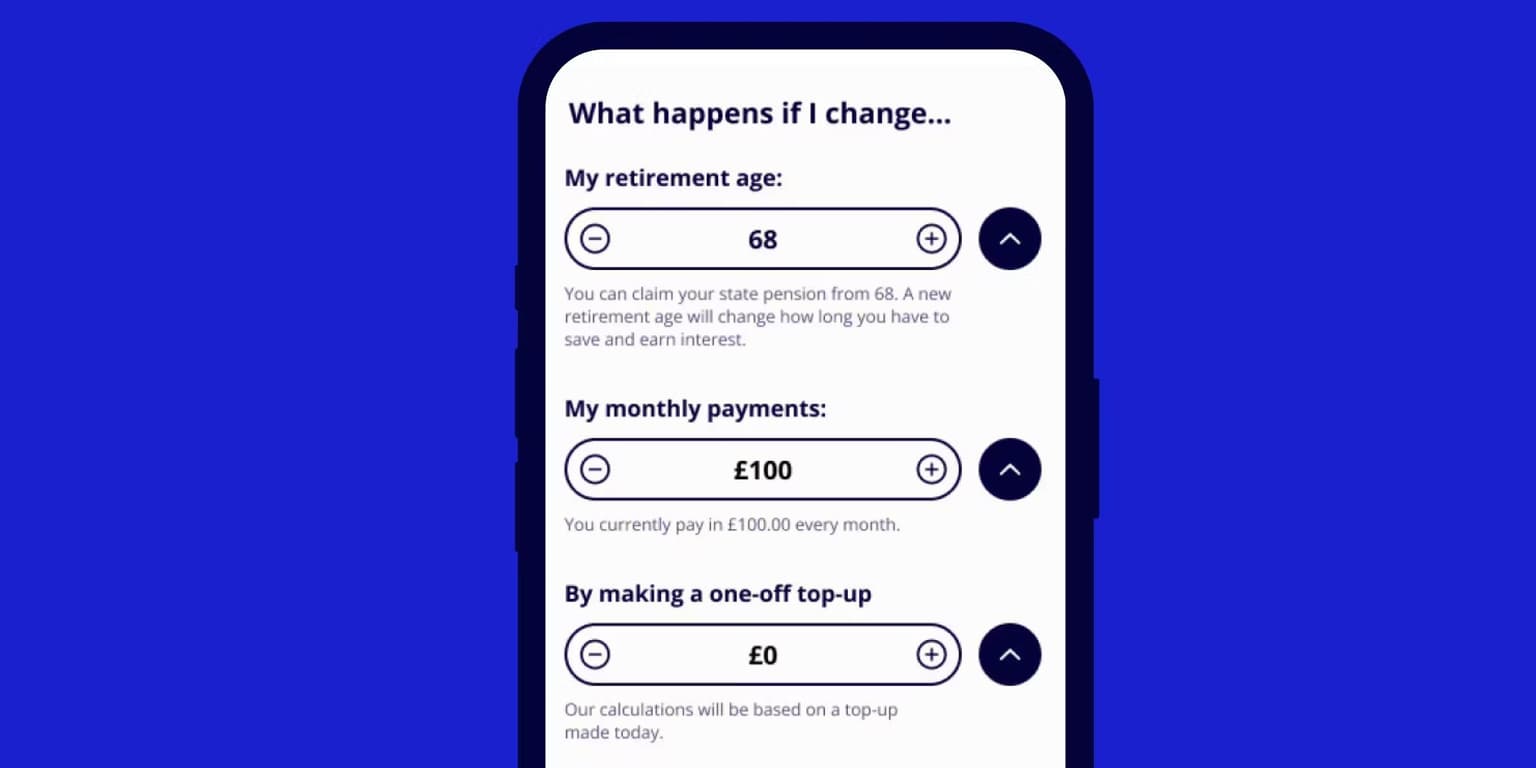

Plan on retiring sooner? You can change your planned retirement age by adjusting "My retirement age". This will automatically update your predicted income - decreasing if you stop working younger, increasing if you want to retire later. The maximum age you can set is 100.

You can also adjust your monthly pension contributions to get a clearer idea of how altering your savings today will affect your pot size tomorrow. Increasing or decreasing the number under "I make personal monthly payments of" will give you an idea of how your retirement income could change depending on your regular payments into your pension.

Of course, many people prefer to pay into their pension on a more ad-hoc basis. Your Forecast also allows you to factor in how a one-off top-up today affects your future pot.

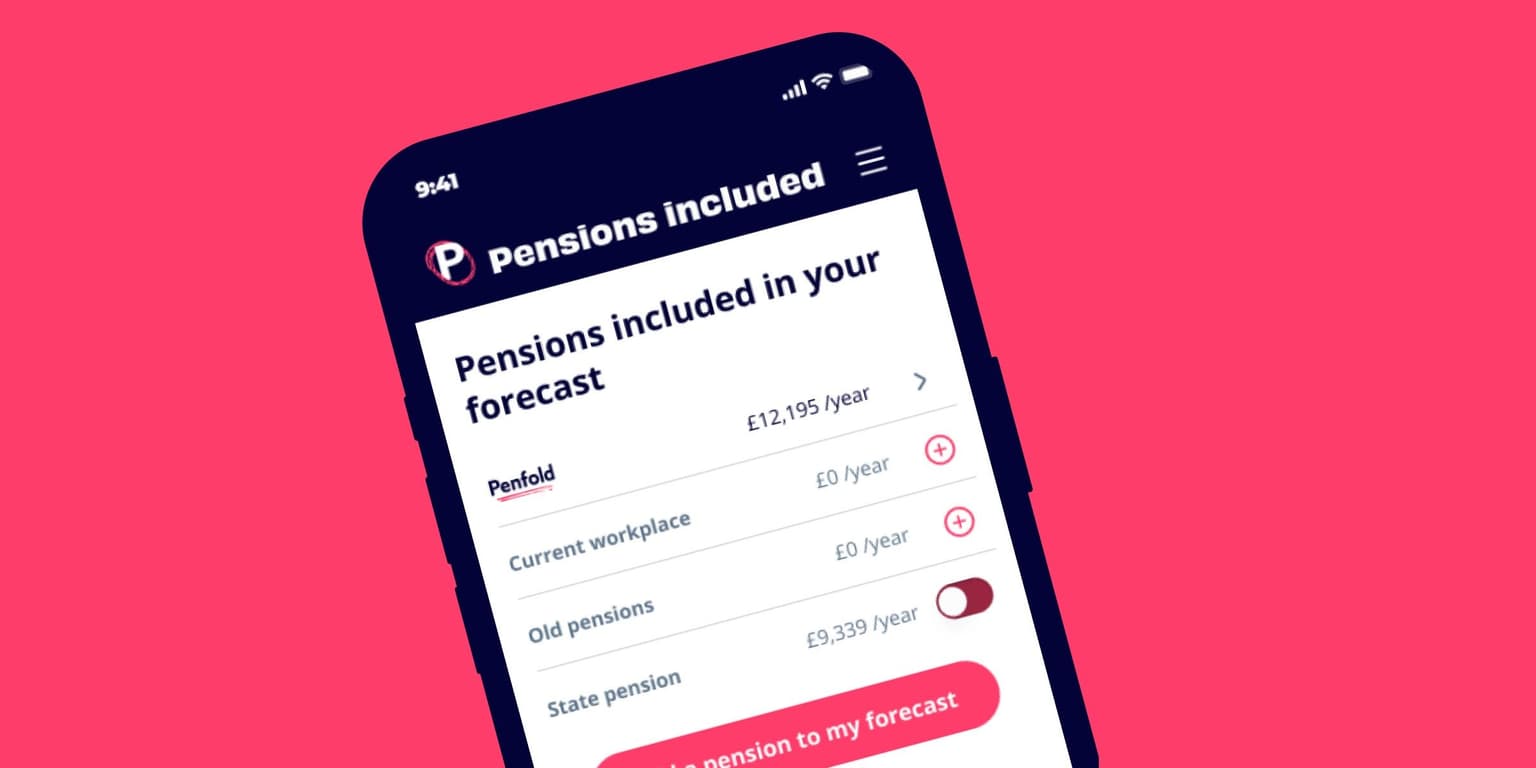

Forecasting your retirement accurately relies on us having a complete picture of your savings. You may also have old workplace pensions or other private pensions outside of Penfold you'd like to include. Your Forecast makes it a doddle.

Tap the button to the right of "What's included in my forecast?" to see a breakdown of all the pensions currently included in your forecast. From here, you can tap the plus icon to add the value of your other pensions into the calculation. Remember to include ALL your other pensions in this figure. An estimate is fine, but the more accurate the number, the more precise your forecast will be!

You can also choose to include the State pension in your forecast. For those that aren't aware, the State pension is a payment from the government to you when you reach State pension age, currently 66 but scheduled to rise in the coming years.

Please note: adding the State pension to Your Forecast will lock your chosen retirement age to your predicted State pension age. If you're still a few years from retirement, you won't be eligible until you're 67 or 68. In other words, you can't include the State pension if you plan on retiring before 66.

The State pension currently pays £9,339 a year, although it rises every April with the triple lock. Just tap the slider to add or remove the State pension to your forecast.

Your Forecast is based on a few assumptions, including:

With pensions, as with all investments, your capital is at risk. Your projected retirement income is not guaranteed and could be higher or lower than forecast. Your Forecast also assumes that pension tax laws will not change between now and your retirement.

Remember, that any withdrawals from your pension (excluding a 25% tax-free lump sum) will be subject to income tax at your marginal rate.

For more information on how Your Forecast is calculated, tap 'Forecast assumptions' just under your retirement income figure.

Are you a company director? Your Forecast works just the same way for you. All you need to do is scroll to the bottom of the tool and tap the "I'm contributing from a business account" slider.

Your Forecast launches today for all Penfold savers. Simply sign in online or on the app to check it now!

Your Forecast aims to show you what your yearly income might be in retirement - based on your age, the current value of your existing pensions and projected monthly contributions.

First, we calculate the total size of your pension when you reach retirement age. This forecasted figure is then divided by the number of years you will be ‘in retirement’. We assume your retirement period lasts until you reach 100 years of age.

For example, if you wish to retire at 70, Your Forecast will show you how much you can withdraw from your pension from age 70 to 100 - or a 30-year retirement.

Today, the retirement age for private and workplace pensions is 55. This is the earliest you can access your savings when a hefty tax charge. The retirement age is scheduled to rise to 57 in 2028. It's likely the minimum retirement age will increase further in the years ahead.

To help you make sense of your retirement figure, Your Forecast also provides 3 types of retirement lifestyles

All 3 lifestyle categories use the Retirement Living Standards study from the Pensions Lifetime Savings Association (PLSA). The PLSA’s benchmarks help you understand how much you’ll need each year in retirement to afford your desired lifestyle - based on a basket of everyday goods and services.

Your Forecast highlights what lifestyle you’re currently on track for, and how changing your contributions or retirement age can help you reach the next level.

Your Forecast assumes an average annual inflation rate of 2.5%, in line with the Bank of England's target rate. This means the real value of your money drops by 2.5% every year - £10 went much further ten years ago than it does today. The investments inside your pension are designed to help combat inflation by providing returns far above the rate of inflation so that the real value of your money grows.

No, this forecast only shows your yearly income from your total pot at retirement. Should you wish to take your 25% tax-free lump sum when you retire, your yearly retirement income in the following years will be lower. For more on your options at retirement, check out our complete guide to pension withdrawal.

If your forecasted retirement income is looking a little low, there’s no need to panic. Pensions are a very long-term investment. For many of us, it's the longest we’ll ever hold an investment. Even if you’re far off from your retirement goal, chances are there’s plenty of time to catch up.

It’s also important to make sure your forecast is correct - have you added all your pensions from old jobs or other providers? Have you included the State pension?

If you’re concerned about your retirement outlook, speak to someone. You can get free, impartial advice from the government-backed Money Helper using the details below.