Pension performance update: January 2023

Stay informed with our global investment market and Penfold pension plans performance update for January 2023 and see how your savings may be affected.

Murray Humphrey

17 February 2023

3 min read

The stock market kicked off 2023 with a bang, with gains across the global equity landscape. The reopening of China, with the end of the zero-Covid policy in December, helped drive this growth. Likewise, easing inflation in the major economic regions has helped to boost market sentiment as central banks now appear to be winding down the series of interest rate hikes.

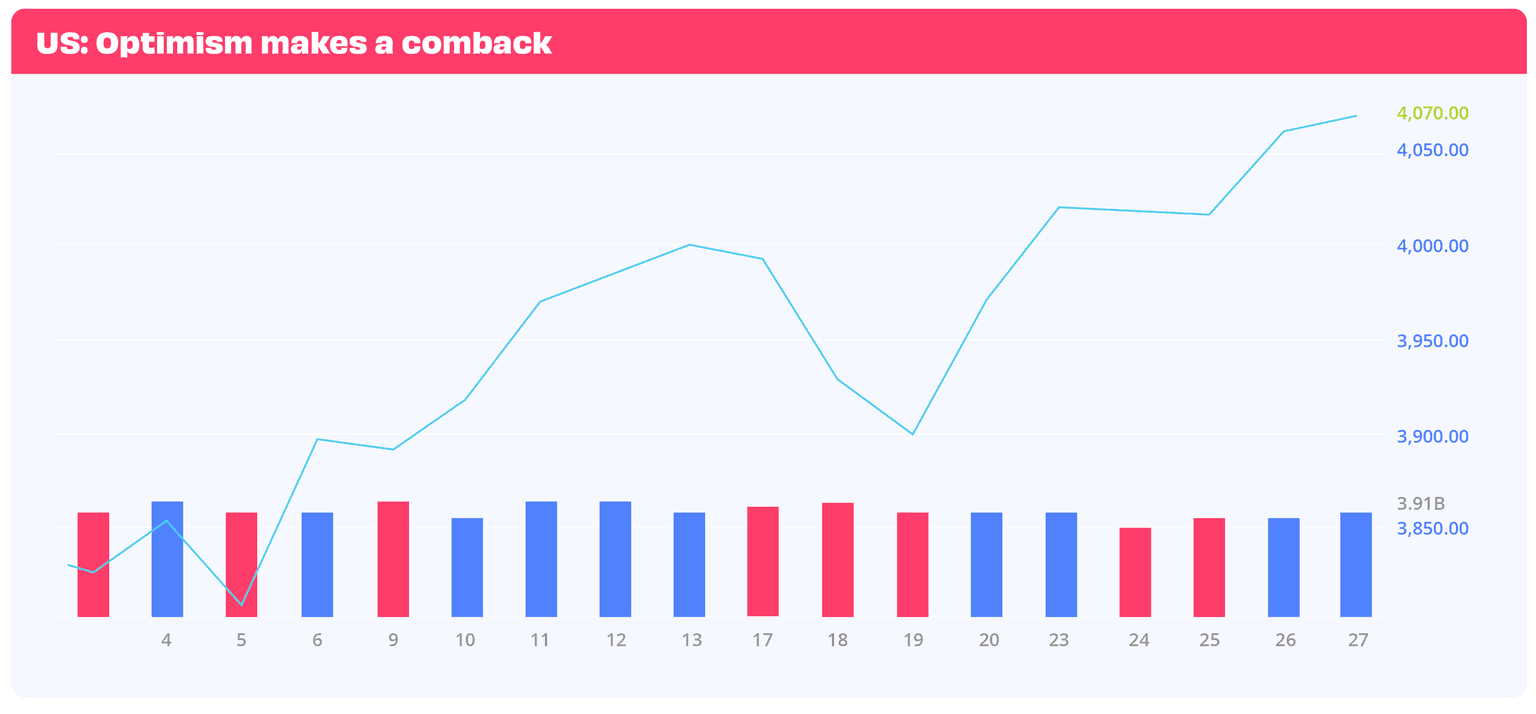

In January, the stock market in the US saw robust gains, with the S&P 500 closing the month at 6.18% higher. Investors have been encouraged by the decrease in inflation, for the sixth consecutive month, with the moderation of energy and food costs, which led to expectations of slower rate increases from the Federal Reserve (Fed).

Most market sectors showed growth, with substantial returns in the technology and consumer discretionary sectors and the travel and automotive industries. The lower-than-expected jobless claims, at 186,000, and the higher-than-anticipated GDP growth, of 2.9%, further supported the positive market sentiment.

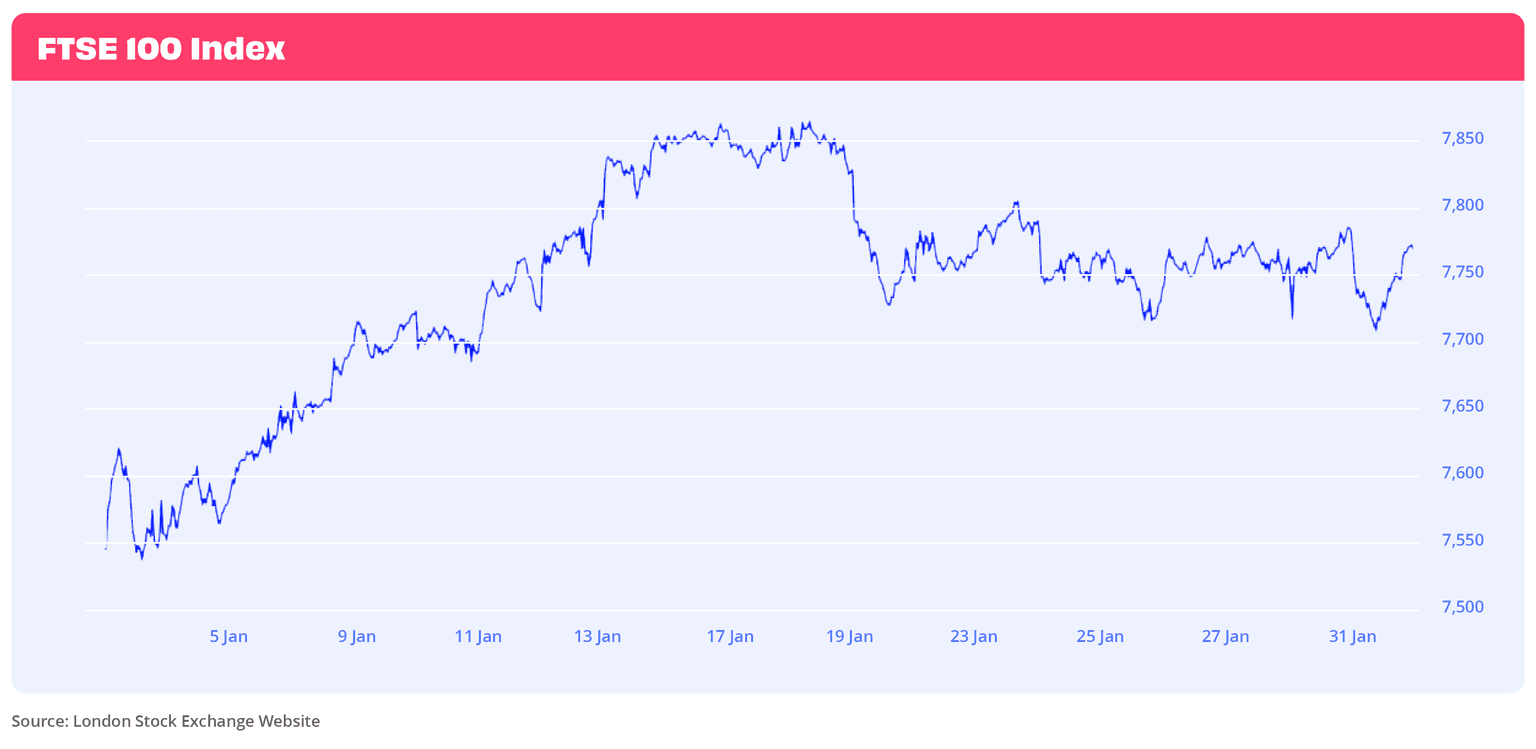

The beginning of 2023 saw a positive trend in the UK stock market, although not as much as in other regions, but better than anticipated. The FTSE 100 index experienced a 4.3% increase from the end of December 2022 to the end of January 2023, with consumer discretionary and financial as the top-performing sectors. Also, UK small and mid-cap equities did particularly well due to strong performance from domestically focused consumer stocks and banks.

Overall, January's increase is connected to the improving situation with US inflation and the hope that the Fed might cut interest rates later in the year, with other central banks following that path.

In fact, recent economic data showed the UK economy held up better than predicted, growing by 0.1% in November, raising hopes for a shallower recession in the coming months.

If things are looking good for UK and US markets, the year started even better for EU stocks. One key contributor to this success was the strong performance of luxury goods stocks, driven by China's decision to relax its strict zero-Covid policy and reopen its economy.

Again, inflation has been declining here as well, from 10.2% in November to 9.2% in December, raising hope that the European Central Bank (ECB) will soon stop raising interest rates, with positive effects for investors. Furthermore, while the economic growth is slowing down, from 0.3% in Q3 to 0.1% in Q4, indicators and forecasts suggest that the Eurozone may avoid a recession entirely.

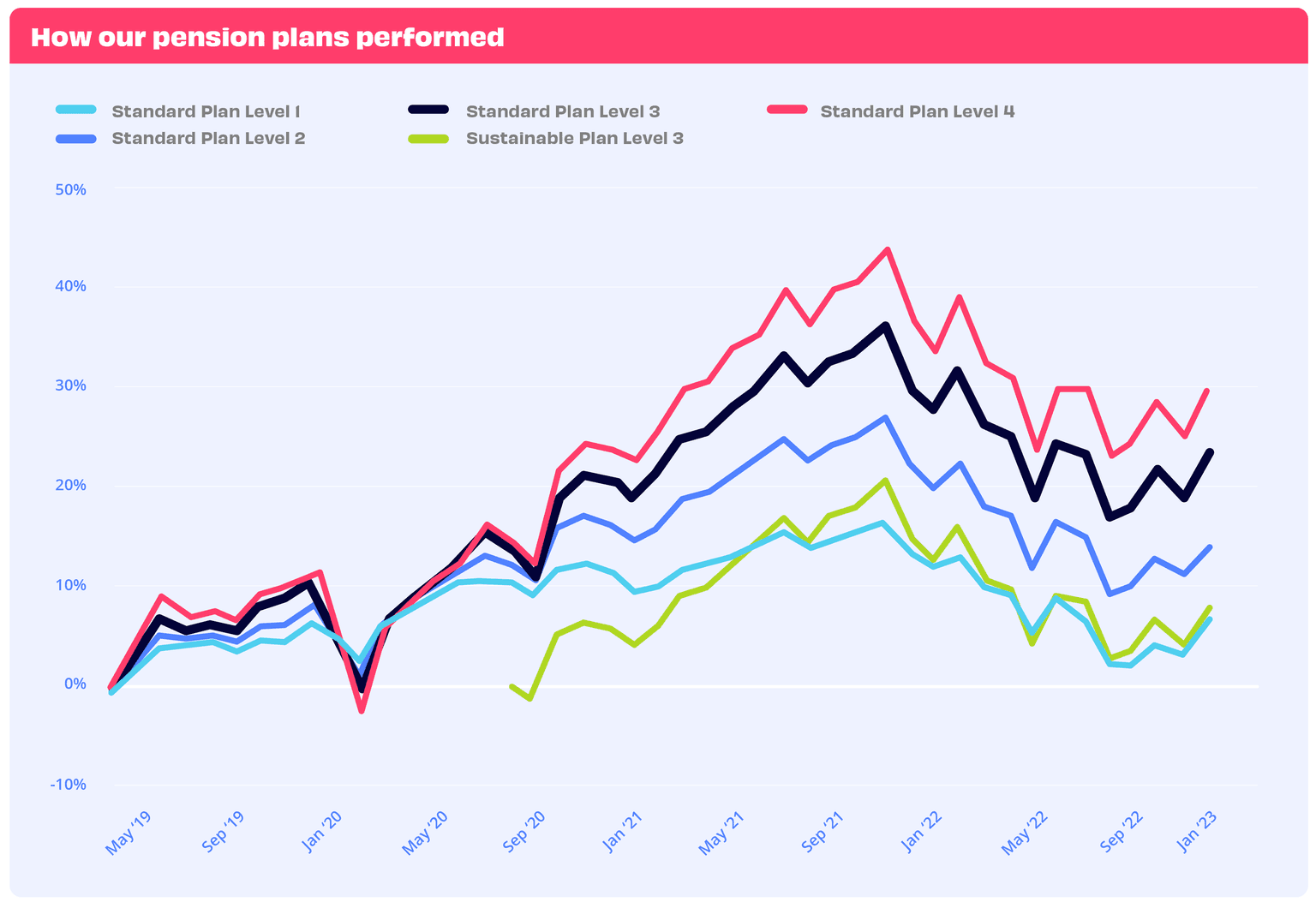

Our plans also had a positive start to the year, experiencing good growth and returns - bouncing back firmly and overcoming December's setback. The chart below shows that despite the monthly fluctuations, the general trend visibly improved starting from the last quarter.

While it is encouraging news that our plans have had such a rebound, it is essential to bear in mind that the global situation remains challenging and the financial markets will likely stay unpredictable and turbulent for the foreseeable future.

With our pension plans, we aim to strike a balance between risk control and good returns. To achieve this goal, our funds consist of a diversified range of investments across various geographies and industries, which helps reduce your savings' exposure to market volatility.

With that in mind, we continue to monitor the markets closely with the goal of providing you with the peace of mind that your pension plans are well-managed and on track to help you achieve your long-term financial goals.

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice and past performance is not a reliable indicator of future performance.