Benefits of Paying Into Your Pension Before Tax Year End

Paying into a pension before tax year end could boost your savings and cut your tax bill. See who benefits and why acting now matters.

Murray Humphrey

11 February 2026

6 min read

If the end of the tax year is approaching and you’re wondering whether it’s worth paying into your pension now, here’s the short answer: For most people, yes – and waiting could cost you real money. A pension contribution before the tax year ends can:

This won’t take long to read, but it could make a meaningful difference to both your take-home position today and your future finances.

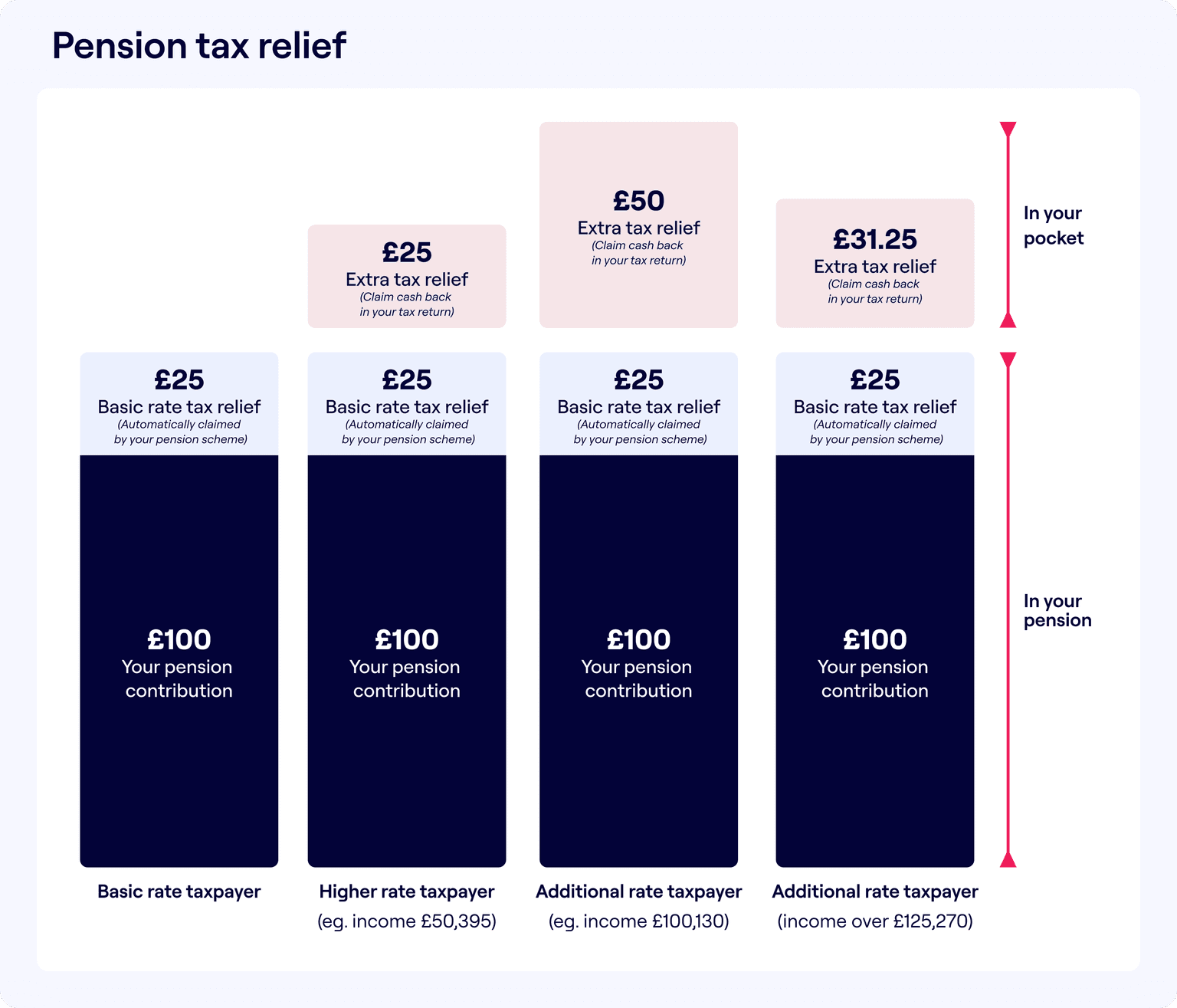

The government wants people to save for retirement so it actively rewards you for doing it. That reward comes in the form of pension tax relief, which effectively means: Some of the money you would have paid in tax goes into your pension instead.

Tax year end pensions planning is all about maximising the tax relief available:

Basic rate taxpayers: Every £1,000 you contribute gets a £250 government top-up and you don’t need to claim anything back yourself.

Higher or additional rate taxpayers: You can claim even more tax back via your Self Assessment as long as the contribution hits your pension before the pension tax year ends.

You don’t need to claim anything – we do it automatically for you.

This extra relief can be worth thousands, but it’s only available if the contribution is made before the tax year ends.

👉 If you want to understand exactly how this works, we explain it clearly in our Pension tax relief explained guide.

If you’re self-employed, a pension contribution before tax year end can be one of the simplest ways to cut your tax bill. You can contribute:

And you’ll still benefit from the 25% government top-up. That means money that would otherwise be lost to tax is instead:

The key thing to remember is that the £60,000 limit applies across all your pensions combined, not per account.

👉 Full details here: How much can self-employed people pay into a pension?

If you run a limited company, paying into a pension before tax year end is often more tax-efficient than taking money as salary or dividends. Here’s why directors often choose pensions:

In simple terms: Putting company profits into a pension can save you up to 25p in tax for every £1 contributed. That’s why many directors use pensions deliberately as part of their year-end planning.

👉 Learn more here: How much can a company contribute to a director’s pension?

This is the part many people underestimate. Once the tax year ends:

Acting now means:

If you’re already planning to save for the future, doing it before the deadline is usually the smarter move.

The official tax year ends on 5th April, but pension contributions don’t always work right up to that deadline.

Most pension providers set their own processing cut-off dates to make sure payments have time to clear and be allocated correctly. That means if you wait until the last minute, your contribution could end up counting towards the next tax year instead.

Before the tax year ends, it’s worth checking:

Missing a provider’s cut-off, even by a day, can mean losing valuable tax relief for this year, with no way to claim it back later.

If you’re planning a top-up, acting a little earlier gives you peace of mind that your contribution will count for the current tax year.

You don’t need to overhaul your finances or make a long-term commitment today. For many people, tax year end is simply about:

Contributing to your pension now isn’t just about retirement – it’s about keeping more of your money working for you.

Take a moment to review your pension before the tax year ends.

It’s a small action today that your future self will genuinely thank you for.

Here’s what to prioritise before the tax year ends:

Missing the official pension tax year end cut-off could mean losing valuable tax relief that you can’t reclaim once the year closes.

Finally:

Tax year end pensions planning isn’t just about saving for retirement, it’s about keeping more of your money working for you today. The earlier you review your pension position and confirm the pension contribution cut off date, the better your chances of claiming every bit of tax relief you’re entitled to before the pension tax year ends.

A Penfold pension helps you keep more of what you earn and secure your financial future. Learn more about our award-winning pension today.