Do pensions rise with inflation?

The cost of living in the UK is rising. Do our pensions rise with inflation?

Murray Humphrey

26 April 2023

5 min read

You may have heard recently about the rising inflation rates in the UK. Today we're looking at what that means and how it might affect your pension.

Ok, first things first. What is inflation and why should you care?

Inflation is the decrease in purchasing power of your money. Essentially, it's why £10 in 1990 could buy a lot more than £10 today.

This happens due to the fact that, over time, the price of goods and services we use tends to increase. To help track the real value of our money, economists monitor a select group of these goods and services that are commonly used in most households.

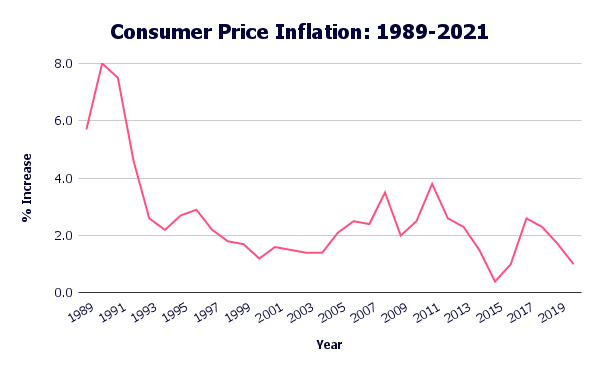

The Office for National Statistics uses a basket of around 700 of these essential items to create the Consumer Price Index (CPI). This includes things like food, fuel, insurance, clothes and more. If the average cost of this group of items rises over time, it means the cost of living has gone up. This is inflation.

Source: Office for National Statistics

The chart above shows how much the prices of these key good has increased by each year. As you can see, each year the costs of these vital goods and services go up, ranging from a small increase to large jumps. On average, inflation tends to hover around the 2.5% mark - or put another way, £100 is worth £97.50 a year later.

As of the end of 2021, inflation in the UK is currently set to 4.2%.

If inflation means our money doesn't go as far year after year, what can we do to help protect the value of our earnings? One of the best answers lies within your pension.

The best way to beat inflation is to put your money somewhere where it can grow. By investing your money in a diversified, long-term pension fund, the return on investment that comes from your pension could outstrip inflation, helping preserve the value of your hard-earned money and leaving you with more than you began with.

Of course, investing can be a little scary. Saving into a pension involves risk, and the value of your pot can go down as well as up, more so in the short term. But that doesn't mean people should be put off investing their money. Truth is that leaving your money in a current account or (perish the thought) under your mattress isn't as safe as it might first seem. In fact, you're actually losing money as inflation eats away at your savings.

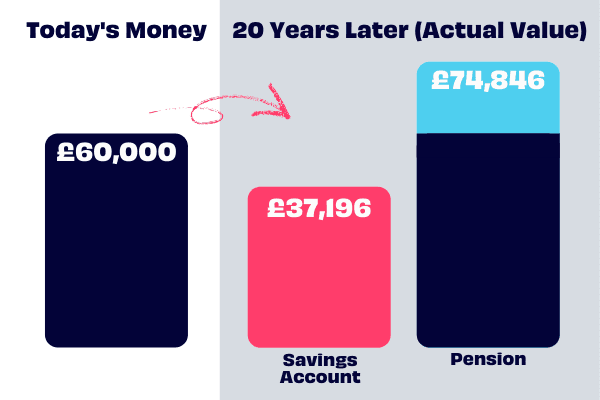

Let's look at a couple of scenarios to explain this. Two people are saving for their future and can both afford to tuck away £250 a month. Let's assume inflation is roughly the same as the last 20 years, around 2.8%.

Put another way, just putting £250 a month in a pile for 20 years would leave you £60,000. By saving into an account with such low interest, effectively you've lost more than £20,000 in value.

Another impact of the rate of inflation is on the State pension. If the value of money goes down each year, doesn't this mean State pension payments are also becoming less valuable?

This is where the triple lock comes in. To protect the value of the State pension against the rising cost of living, the government has established a three-stage guarantee to keep pension payments in line with inflation. Each year, State pension payments increase by the highest of:

In theory, this means that no matter how much the cost of living rises, income from your State pension will keep pace. Of course, there have been exceptions to the triple lock in the past.

Unlike the State pension, withdrawals from your private pension will not be protected by the triple lock. Anything you take out from your private (or workplace) pension is affected by inflation. This is another reason why it can be a good idea to keep part of your pot invested, even when you retire.

Many people like to take out a large sum from their pot each year to cover their expenses. However, this can leave you liable to lose value from your money as inflation begins eating into your withdrawal.

By keeping as much of your savings pot invested as possible, the value of your pension won't stagnate and may continue to see growth from your investments. It may also be a good idea to speak to a financial adviser about how much you should be withdrawing and when.