Is Salary Sacrifice Worth It?

Discover the pros and cons of salary sacrifice, plus ways employees can benefit from lower taxes & employers can save on National Insurance contributions.

Frankie Dewar

23 July 2025

5 min read

💡 Looking to reduce your business’ National Insurance bill?

Penfold offers free salary sacrifice setup and support—with zero hassle.

Talk to our team or Get started now

Thinking about setting up salary sacrifice for your company? Here’s what you need to know before diving in. Salary sacrifice can help your employees take home more pay while helping your business cut down on National Insurance contributions (NICs). But is it right for you?

In a nutshell, salary sacrifice is where an employee agrees to swap part of their salary for a non-cash benefit. This lowers their annual pre tax salary, the ‘sacrificed’ earnings are then used to fund another benefit provided by the company. One of the most popular ways of using this scheme is with a salary sacrifice pension scheme.

Traditionally employees pays into their pension from their pre-tax earnings. With salary sacrifice, employees reduce their salary - instead contributions come entirely from the employer.

The result is that employees take-home pay is lower 'on paper'. This means the amount of salary National Insurance applies to is also lower. They also benefit from tax relief on their pension contribution.

As the employer, you'll also make savings on the National Insurance owed for your employees.

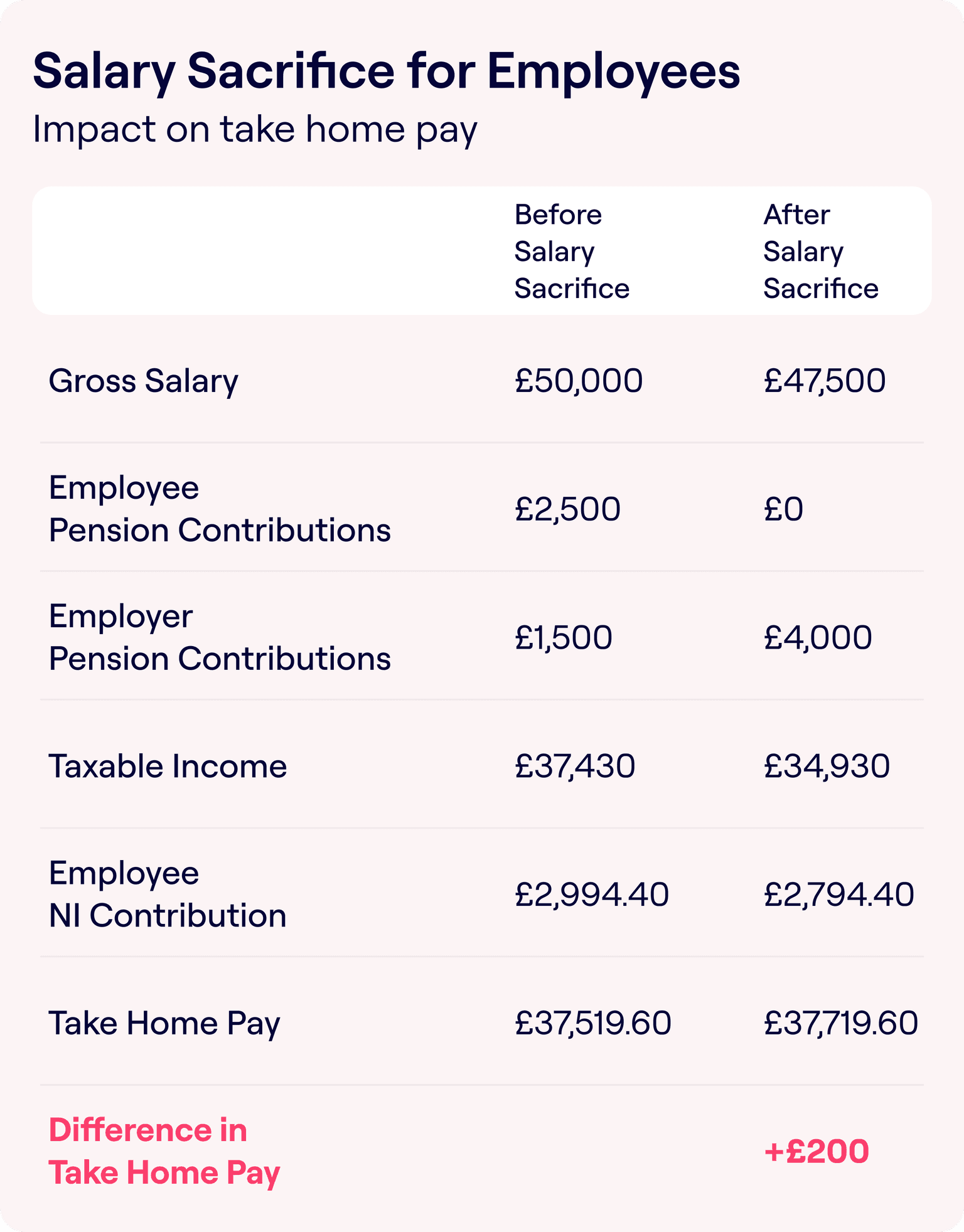

This example shows the difference salary sacrifice makes for an employee with an annual salary of £50,000.

Before salary sacrifice:

After salary sacrifice:

The table below shows how much an employee earning £50,000 a year would save by switching to a salary sacrifice pension.

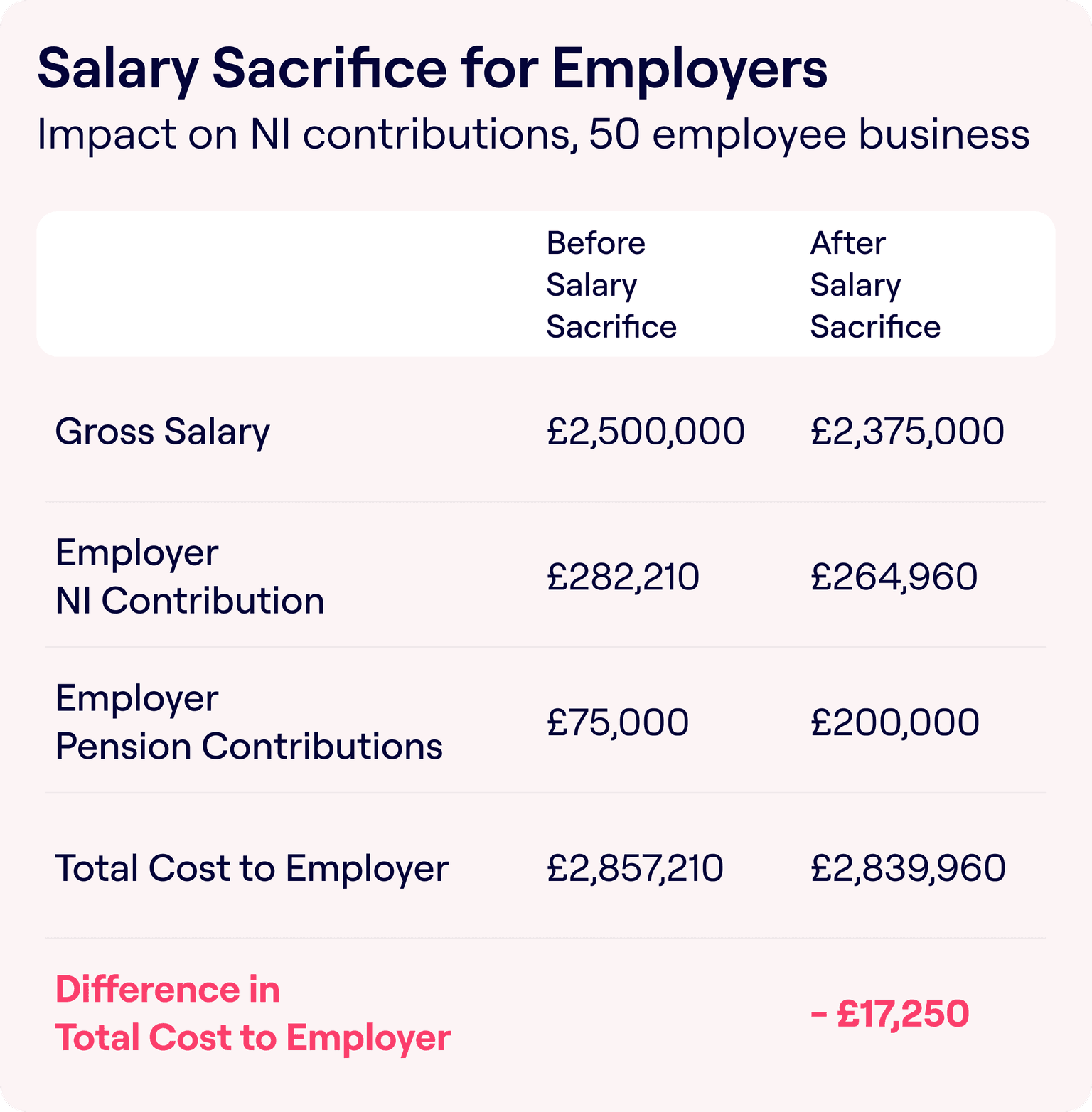

In some cases, employers add their National Insurance savings from salary sacrifice into the employee’s workplace pension as well. This increases their overall contribution and gives their employees a boost on the way to retirement.

The table below shows the employer impact of switching to a to a salary sacrifice pension. Of course, the more employees a business has, the larger the savings will be.

Non-cash benefits such as pension contributions and cycle-to-work schemes are exempt. This is because employers pay National Insurance on gross salaries.

See how much your business and employees could save by using our salary sacrifice calculator.

Further benefits depend on the benefit but include:

Employers can switch to salary sacrifice by updating their employment contracts. Any changes will need to be agreed by their employees first.

The most popular use of a salary sacrifice scheme involves workplace pensions. However, employers can offer a range of other non-cash employee benefits. Here are a few examples:

The primary advantages of a salary sacrifice scheme are:

Employees benefit from keeping hold of more of their earnings and trimming their tax bill.

While there are several benefits, salary sacrifice can also have a few negative consequences. Here are some key factors to keep in mind that could affect your final decision.

As an employer, you could encounter increased administration costs when you implement a salary sacrifice scheme. These typically include:

Of course, the savings you make from switching to salary sacrifice could help to cover this initial cost. Penfold can also take care of this for you, making the entire process effortless.

It's also worth noting that any employees on a low income may not be eligible to join. This is the case if salary sacrifice results in their income falling below the national minimum wage.

Additionally, there can be an impact on an employee's salary based benefits and ability to borrow money. Again this is because salary sacrifice leads to a lower overall income. In particular, it could have a knock-on affect on:

It’s important to note that salary sacrifice contributions are considered solely employer contributions.

Contributions via salary sacrifice are unlikely to be refunded if an employee wants to opt out of auto enrolment. This is the case whether they are part of a defined benefit or defined contribution pension scheme.

For employees: Absolutely. Higher take-home pay and boosted pension savings with no extra cost.

For employers: Yes – if your provider supports it. It’s a highly efficient way to reduce tax and offer stronger benefits.

Penfold offers free salary sacrifice setup and support:

Book a free consultation or learn more about salary sacrifice.