Pension performance update: March 2023

Stay informed with our global investment market and Penfold pension plans performance update for March and how your savings may be affected.

Murray Humphrey

18 April 2023

6 min read

You may wonder why we give monthly updates for pensions, which are a long-term investment. We use them to ease customer concerns about financial headlines that may impact their pensions.

Despite the world feeling a little unstable currently with a year-long war, high inflation and interest rates, and economic uncertainty, global stock markets have actually had a positive first quarter this year.

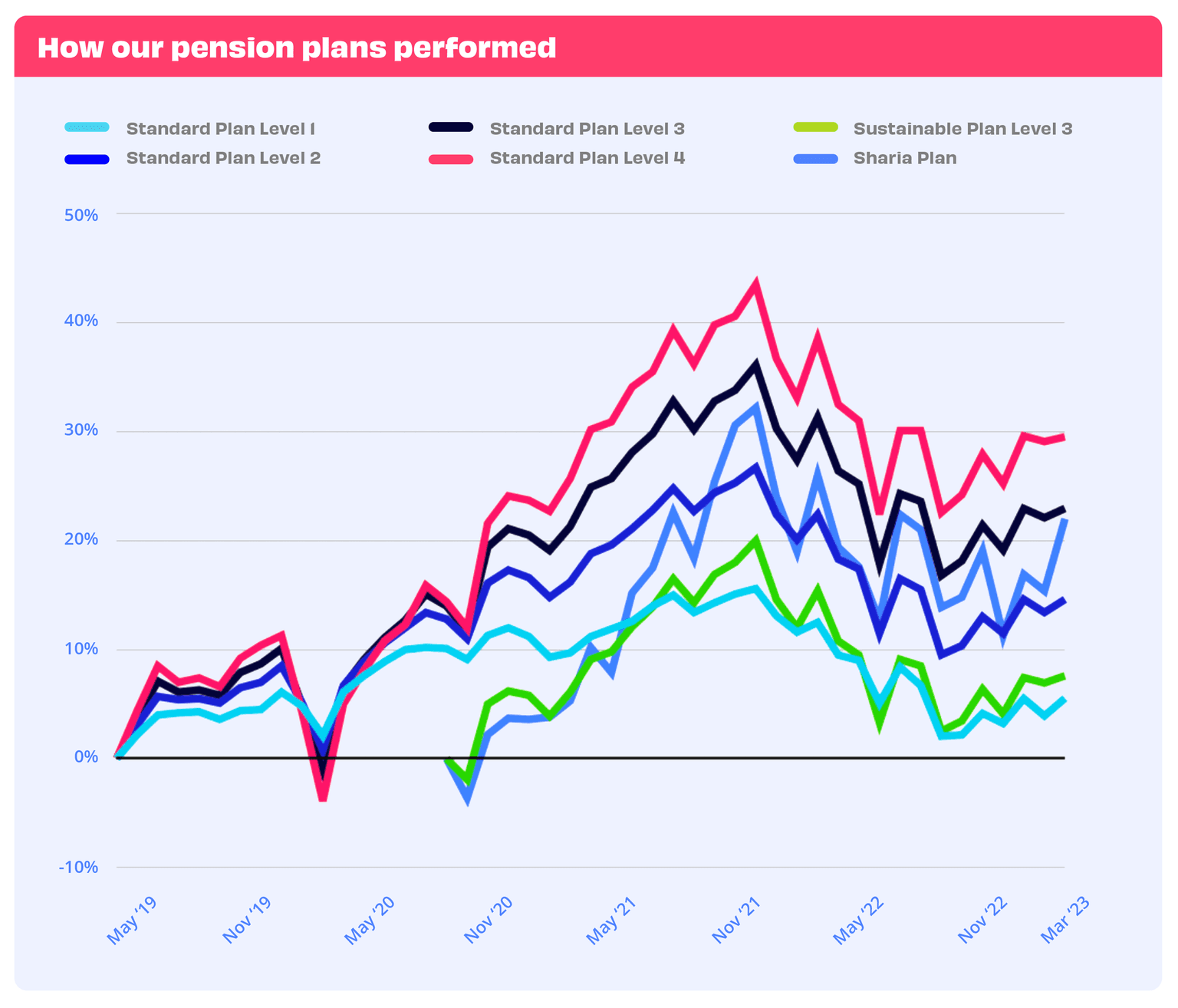

Penfold’s pension plans remained resilient despite a challenging period for the banking sector, the UK stock market and the global economy as a whole (more of which below).

After the slight decline experienced in February, our plans increased their value by an average of 1.74%, and the Sharia plan over performed all others, growing 5.75% in a month.

*Performance gross of fees

How was it possible? Because Penfold's funds are composed of well-diversified portfolios, with investments spreading across different countries, sectors and asset classes. This highlights the benefits of diversification, which is an effective way to reduce the overall risk exposure, minimise potential losses and improve overall investment performance.

Remember, you can check the performance of your Penfold pension at any time with our app. Just tap ‘Your Plan’ at the bottom of the app screen for an instant view of your plan performance.

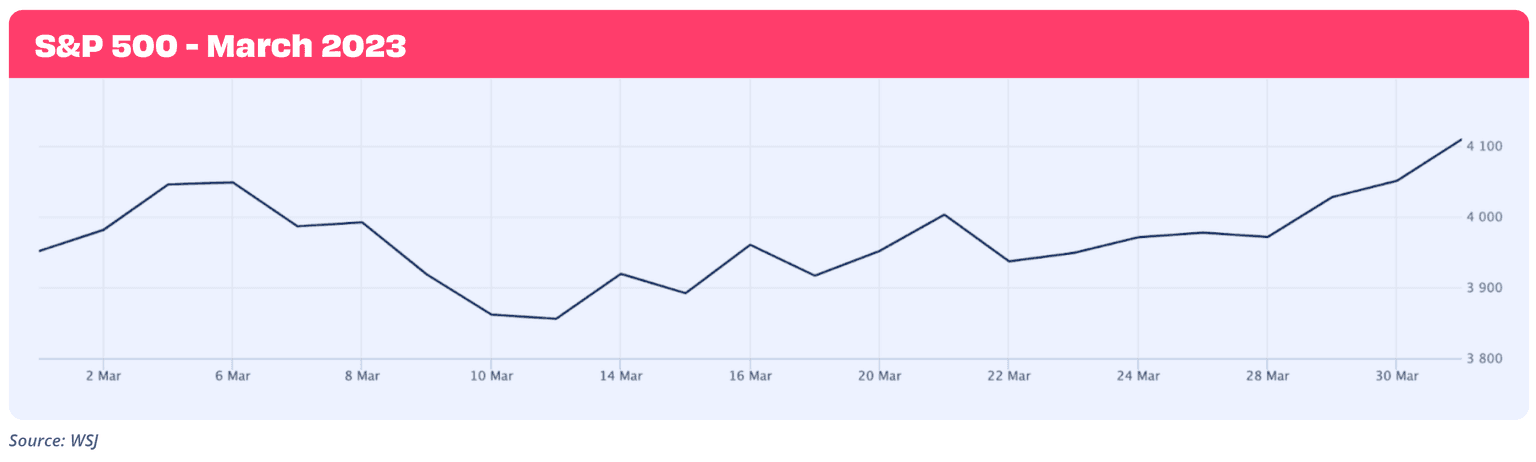

The S&P 500, an index including the 500 largest corporations in the United States, ended March with a 3.51% gain, bringing its year-to-date return to 7.03%.

The financial sector largely shrugged off the collapse of Silicon Valley Bank (SVB) at the start of the month. US stocks initially dipped sharply before recovering to finish the month higher as investors concluded the systemic risk was minimal.

With that said, banks were much in the news during March. SVB and Signature Bank are both gone (with the US government stepping in to guarantee 100% of the money people deposited with them) while commercial bank First Republic's stock price fell 89%. March also saw UBS acquiring Credit Suisse to curb further panic about the stability of the banking industry.

Meanwhile, the Federal Reserve (Fed) raised interest rates twice, making borrowing money more expensive. But with inflation cooling (prices of goods and services are not increasing as fast as before), expectations that the Fed might stop raising rates reasonably soon grew.

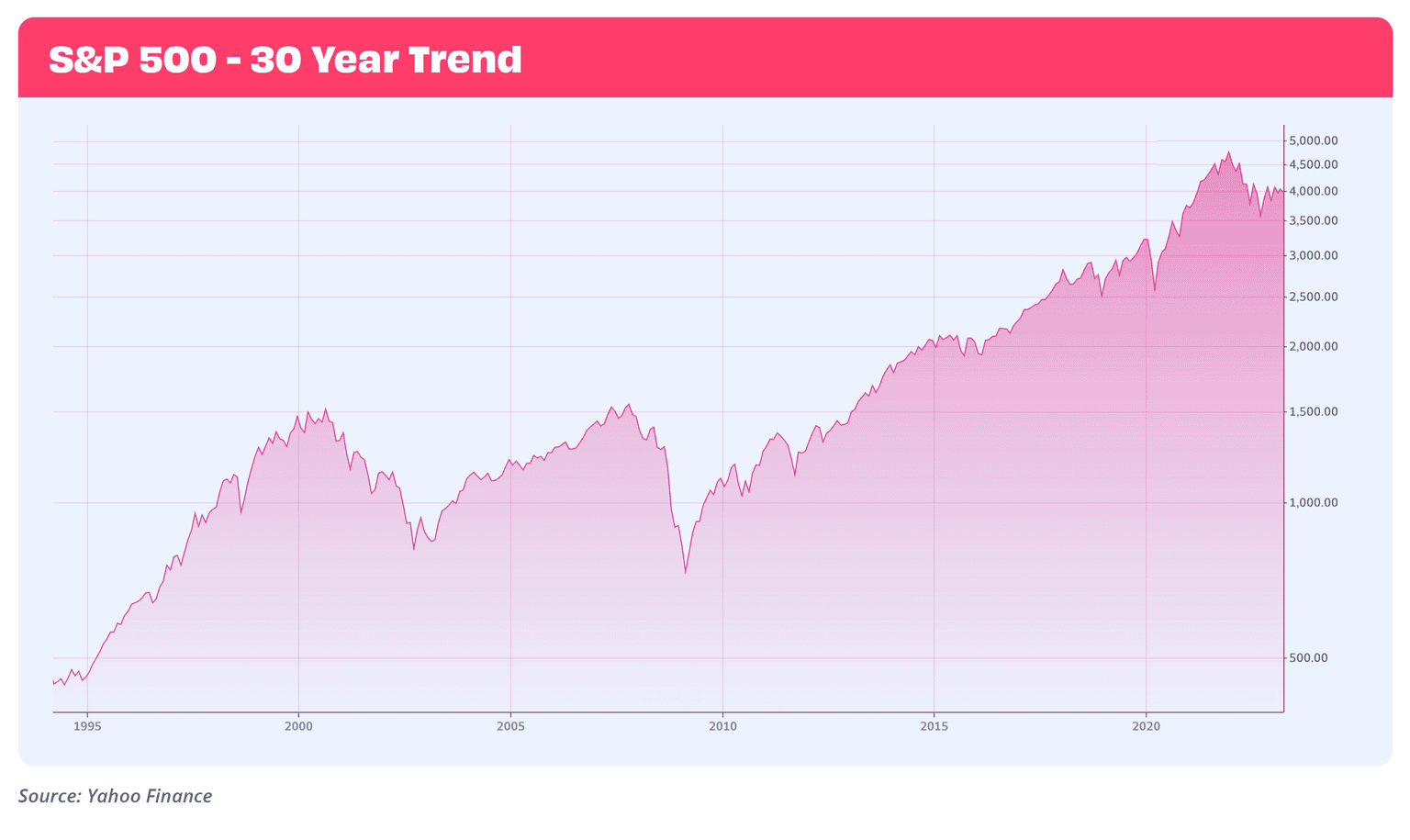

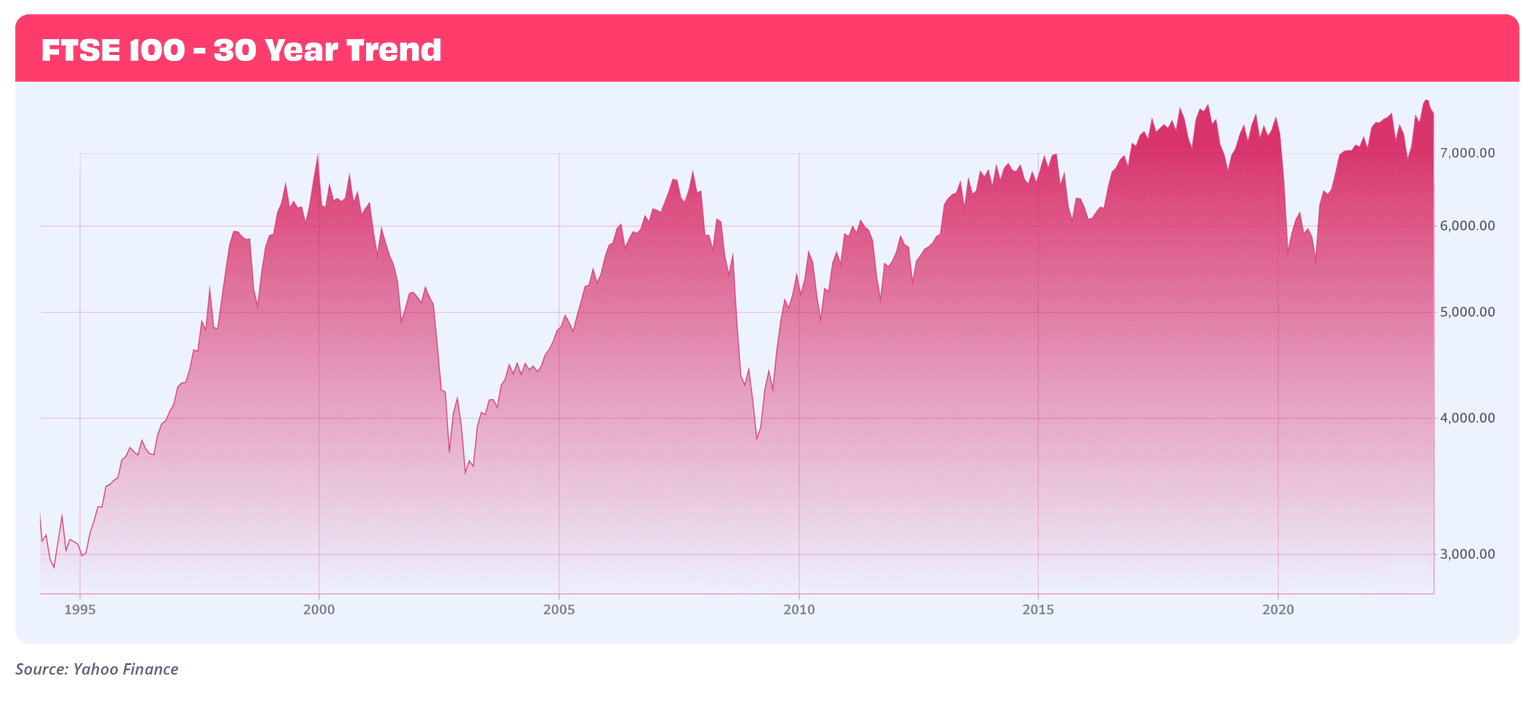

The S&P 500’s gain perfectly illustrates how financial events can cause monthly fluctuations against the backdrop of more long term growth that will ultimately grow pension pots. Here's what the 30 year trend looks like:

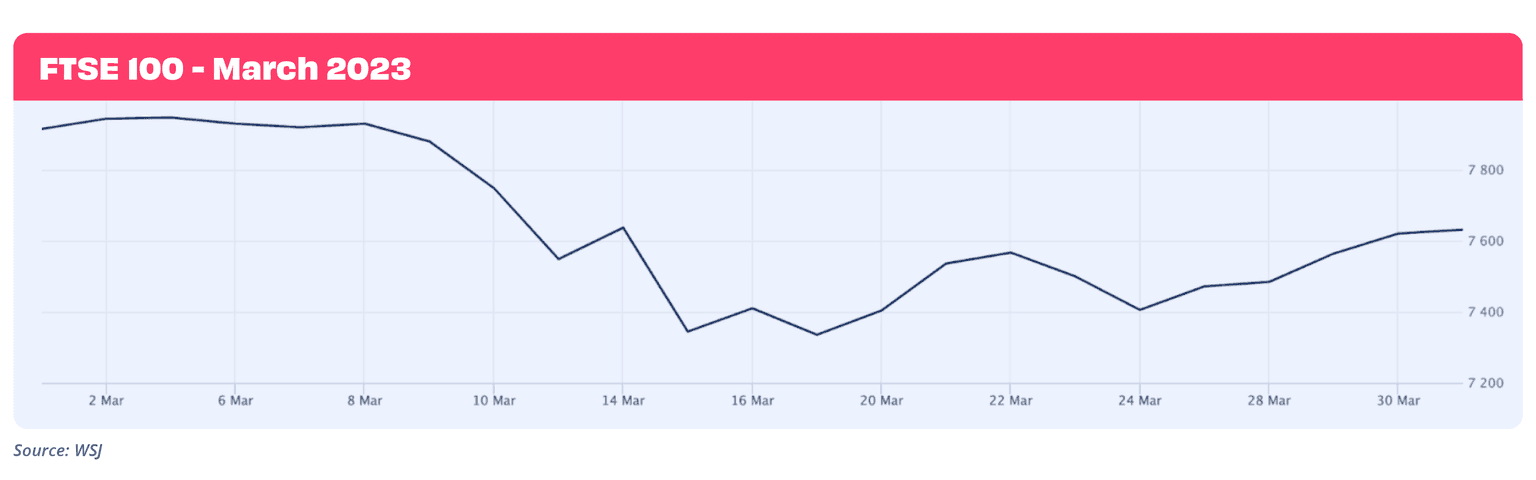

For the time being, the UK’s economy has been able to avoid a recession, with investors reacting well to the positive news from the US concerning inflation and interest rates. Although long-term FTSE growth is expected, March saw a little bump in the road.

UK stocks dropped in March but remained in positive territory for the first quarter of the year thanks to the gains made in February. The FTSE 100, the benchmark for Britain’s largest companies, lost 3% during the month (the worst March performance since 2020) but closed Q1 up +2.4%.

In fact, the UK stock market performance in March was heavily affected by the 13.5% drop in the banking sector caused by the bankruptcy of the US regional banks mentioned above. Stocks wobbled as investors started to worry that it could have created problems for banks all over the world.

This shouldn’t be something to worry about. A single month of poor performance isn’t going to be critical when you’re saving for 20, 40 or 50 years. Investing has consistently delivered a net gain for savers.

If UK stocks in the financial sector had a difficult March, healthcare and consumer staples like food and beverages and household products performed better and helped to close Q1 with a gain despite all these challenges. By the end of the month, share prices were heading back to the value they started March with.

It’s a good idea to take a long-term perspective when managing your pension, even if you are nearing retirement age. We always want to be as transparent as possible with our customers which make frequent ups and downs like the ones described above more visible.

Despite inflation and the challenging dynamics of the banking crisis, the EU stock market had a positive month to close a robust first quarter.

Eurozone inflation experienced a decline and reached a one-year low in March. Specifically, consumer prices rose by 6.9%, a significant drop from the 8.5% increase in February.

In both February and March, the European Central Bank increased interest rates by 0.5%. These raises are expected to slow down in the upcoming months, given the encouraging inflation trajectory (raising interest rates is a monetary policy central banks use to contain inflation).

In March, the EU stock market saw growth primarily in the technology, consumer products, and communication services sectors, while real estate and energy represented the sectors that performed worse.

Some good news also came from the newly announced UK budget for 2023, with which the annual Tax Free Allowance (TFA) has been increased from £40,000 to £60,000.

What does it mean for you? It means that if you can afford to invest more in your pension funds yearly, you can save more money from your taxes.

Previously, contributing £32,000 to your pension every year would give you a tax relief of £8,000, making the total amount you could put in £40,000. Now, with the TFA increase, you can contribute up to £48,000 and receive tax relief of £12,000, totalling £60,000.

This also means that if, for example, you’re already contributing £32,000 to your pension annually, you can increase that payment by £16,000 and make an extra £4,000 from HMRC.

Just one more reason to grow your Penfold pension funds contribution!

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice and past performance is not a reliable indicator of future performance.