How to Avoid the 60% Tax Trap

Earning over £100,000? Learn why part of your income is taxed at 60% – and how pensions and salary sacrifice can help you avoid it.

Murray Humphrey

19 January 2026

4 min read

Earning £100,000+ is a huge milestone and one that should feel rewarding. But for many people, crossing into six figures comes with an unpleasant surprise: part of your income can effectively be taxed at 60%. This isn’t a special tax band. It’s the result of how the UK tax system claws back your Personal Allowance once your income exceeds £100,000.

The good news? With the right pension strategy, this “60% tax trap” is largely avoidable.

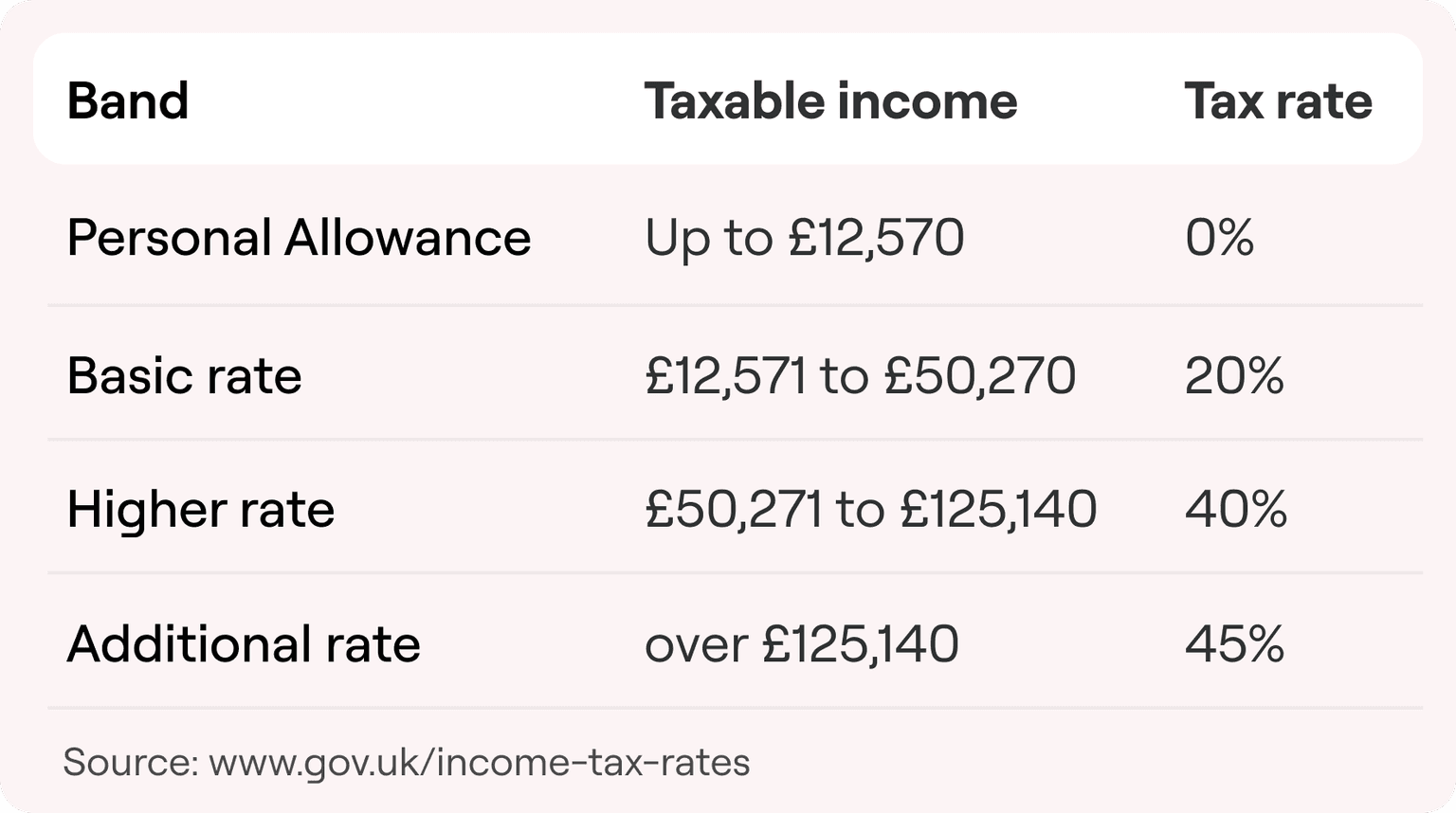

Everyone in the UK can earn a certain amount tax-free each year – known as the Personal Allowance, currently £12,570. Here are the current tax bands.

Once your income exceeds £100,000, that allowance is gradually withdrawn:

By the time your income reaches £125,140, your Personal Allowance is reduced to zero. See GOV.UK Income Tax rates and Personal Allowances

Between £100,000 and £125,140, two things happen at once:

Combined, this creates an effective marginal tax rate of 60% on income in that range (before National Insurance). In simple terms: For every £1 you earn in this band, you may only keep around 40p.

The key to avoiding the 60% tax trap is reducing your adjusted net income back below £100,000. Pension contributions do exactly that. Money paid into a pension:

This means money that would have gone to HMRC can instead be working for your future.

The most effective way to avoid the 60% tax trap is through salary sacrifice.

Instead of:

You agree with your employer to:

Let’s look at the principle. If you earn £110,000 and do nothing:

If instead you salary sacrifice £10,000 into your pension:

The result is:

This is why pensions are often described as the cleanest escape route from the 60% band.

You can usually contribute up to £60,000 per tax year into your pension without triggering a tax charge. This includes:

Many people also have access to carry forward, allowing unused allowances from previous years to be used.

The Lifetime Allowance charge was removed from April 2023. This means:

(There are still limits on the tax-free lump sum, but these are separate and don’t undermine the core strategy.)

For high earners regularly contributing large amounts, this change has made pensions significantly more attractive.

For most people earning between £100,000 and £125,140, yes absolutely. Using a pension (and especially salary sacrifice) can:

Instead of losing money to the least generous part of the tax system, you’re redirecting it to your future.

The 60% tax trap isn’t obvious, and many people fall into it accidentally after a pay rise or bonus. But with the right setup, it’s also one of the easiest tax inefficiencies to fix.

If you’re earning over £100,000 and not using your pension strategically, there’s a strong chance you’re paying more tax than you need to.

The goal isn’t just to earn more – it’s to keep more of what you earn.

This article is for information only and isn’t personal financial advice. Tax and pension rules depend on individual circumstances, so consider seeking advice before acting.