Complete guide to workplace pensions

This comprehensive guide walks through everything needed to set up & successfully run a workplace auto-enrolment pension scheme, plus some key tax benefits

25 May 2023

13 min read

In this comprehensive guide, we’ll walk you through everything you need to set up and successfully run your own auto-enrolment pension scheme. We’ll also cover a few of the benefits of pensions, including how you can trim your company’s tax bill and help your employees keep more of their monthly earnings.

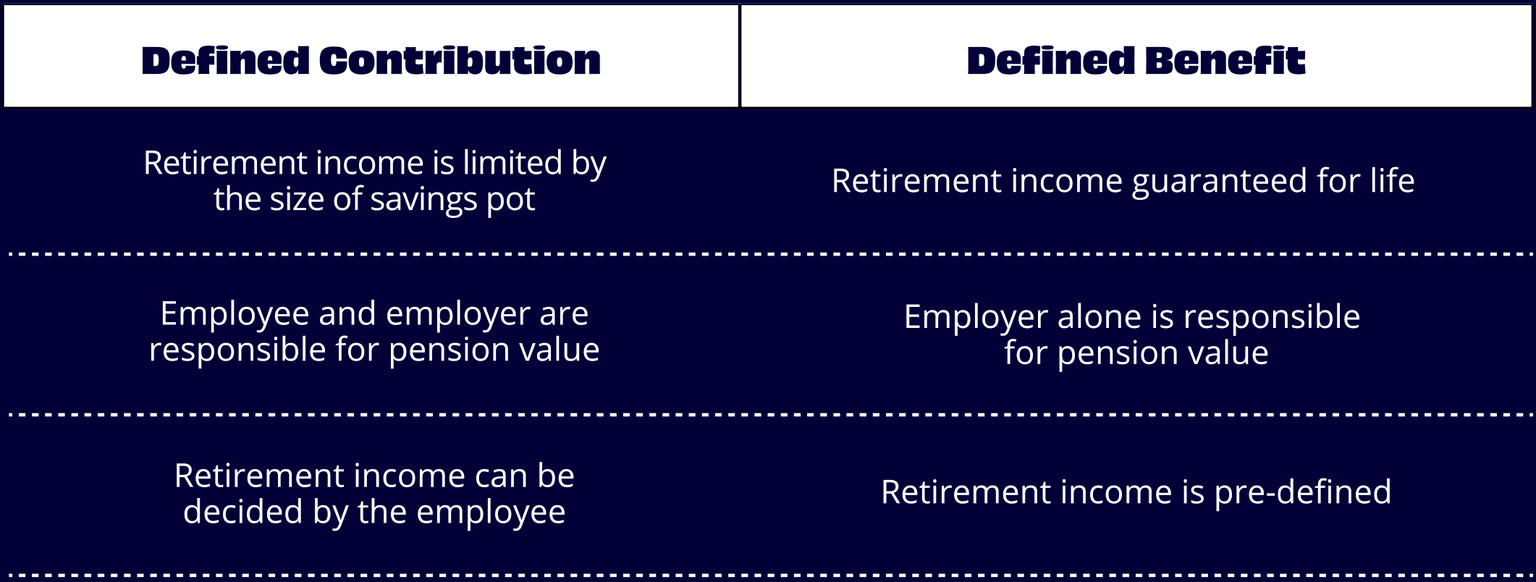

First a quick note. This guide will mainly focus on defined contribution pension schemes. For defined benefit schemes, we recommend speaking to your pension provider directly. Don’t worry if you aren’t sure if this affects you - we’ll go over the difference very shortly.

At its most basic, a workplace pension is a pension arranged by you, the employer, for your employees.

In most instances, both you and the employee pay a portion of the employee’s salary into their pension, helping them save for later life. You may see this type of pension referred to as “occupational”’, “works”, “company”, “employer” or “work-based” pensions. They all mean the same thing. Since 2018, it has been a legal requirement for all companies in the UK to offer some form of pension scheme to all eligible employees.

As an HR professional, it’s likely your responsibility to set up and help manage your workplace pension. You’ll need to choose a pension provider and make sure your company contributes a percentage of each employee’s salary into their pension every month.

Exactly how this works will depend on the type of scheme you offer. Let’s take a look at the different schemes available. Broadly speaking, there are two main types of employer pension scheme:

Defined contribution

If you’re looking to set up a workplace pension for your company, you’re most likely looking for a defined contribution scheme. This means you and your employees BOTH pay into their pension every month for as long as they’re employed.

Employee contributions will come straight from their salary - company contributions are also added before or after tax, depending on your scheme. Everything added to an employee’s savings pot will then be invested into a pension fund.

The pension fund invests their savings into financial markets - usually a mix of stocks and shares, government and corporate bonds, real estate and more. The value of an employee’s defined contribution pension comes from the total contributions how much you and your employer have paid as well as how well the pension fund has performed.

Defined benefit pensions

Some companies (particularly in the public sector) offer defined benefit pensions - also called a ‘final salary scheme’. Here, the size of an employee’s pension in retirement comes from their salary and how long they’ve worked for your company, among other things.

Defined benefit schemes are very expensive - as you are agreeing to pay a portion of an employee’s salary when they retire until they pass away. The table below summarises the differences between defined contribution and defined benefit pensions.

For help on setting up a defined benefit scheme, we recommend speaking to a pension provider directly.

What is auto-enrolment?

You may also see workplace pensions referred to as auto-enrolment. This simply refers to the fact that government legislation requires all eligible employees to take part (or ‘enrol’) in their company pension scheme automatically. If they don’t wish to take part, they’ll need to opt out manually. We’ll cover how this works in a later section.

Here’s the main takeaway: whenever you see auto-enrolment, just think workplace pension.

Right now in the UK, the minimum an employer needs to contribute to a workplace pension scheme is 3% of the employee’s pre-tax salary.

To qualify for this, the employee will normally need to contribute 5% of their pre-tax salary themselves. This is to reach the minimum legal pension contribution of 8% of an employee’s pensionable earnings. More on that very shortly.

What’s the maximum amount a company can contribute?

There is no upper cap on how much an employer can pay into their employees’ pension each month. Some employers offer to match employee contributions up to an agreed limit - for example, if an employee pays in 7% of their earnings each month, so will the company.

Ultimately, how much your company wishes to pay is up to you - just remember there are limits to how much pension tax relief is available. As of January 2022, each employee will only enjoy tax relief on the £40,000 of contributions (or 100% of their earnings, whichever is lower). Anything you add above this amount may be subject to tax.

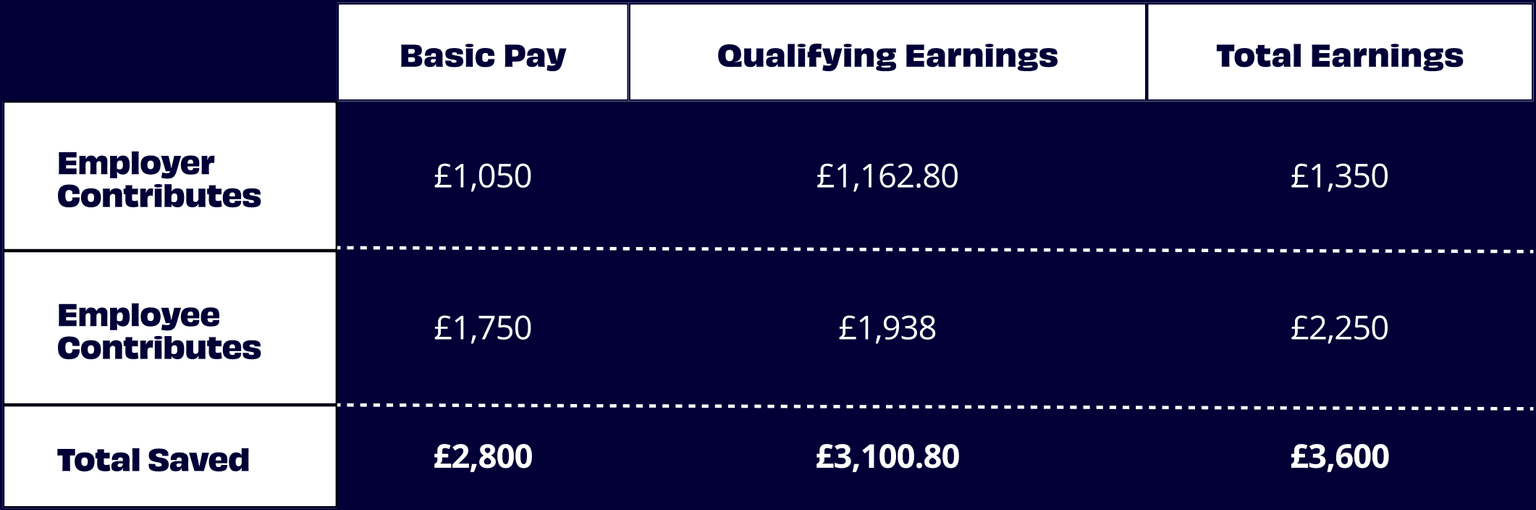

What qualifies as pensionable earnings?

That 8% figure depends on how you work out an employee’s ‘pensionable earnings’. Whichever method you decide to use, it’s important to make it clear to your employees via their pension documentation. There are three ways to approach pensionable earnings:

1. Basic pay

The easiest way to calculate pensionable earnings is the "Basic Pay" approach. Here, you'll use an employee's salary BEFORE any added commission or bonuses.

For example, if an employee earns £35,000 yearly basic but receives £10,000 in bonuses, only the £35,000 salary counts as pensionable earnings. Together, you and the employee will need to contribute a minimum of 8% of their annual salary. In our example, that means your company must pay in £1,050 a year.

2. Qualifying earnings

Another way of calculating pensionable pay is something called "qualifying earnings". In this approach, you'll use any earnings between £6,240 and £50,270 as the basis for contributions. This also includes:

Using the same employee earning £35,000 (with a £10,000 bonus) as above, your company will now need to contribute £1,162.80 over the year.

3. Total earnings

Finally, you can also use an employee's total earnings as the basis for their pensionable earnings. This is simply their basic pay plus all the extras outlined above. Again, for our worker earnings £35,000 a year with a £10,000 bonus, your company would have to contribute £1,350 into their pension.

Here’s how that all compares for an employee earning £35,000 with a £10,000 annual bonus.

By law, you are only required to enrol 'eligible employees' in your workplace pension scheme. An eligible employee means:

Additionally, there are a few other things that may disqualify an employee from your pension scheme. These include:

Can employees opt out?

While every eligible employee needs to be enrolled automatically in your workplace pension scheme, they can 'opt out' if they don't want to take part. They can do this by sending you a formal opt-out request by letter or email.

If they have been paying into your pension scheme previously, their savings pot will remain where it is until they reach retirement age, or decide to transfer to a new pension provider. The company will no longer need to contribute into their pension pot unless they choose to opt back in.

It's important to know that even if an employee has opted out, you as the employer legally must offer them the chance to rejoin the scheme at least once a year.

Further, you'll need to automatically re-enrol them back into the company pension scheme after three years (assuming they are still eligible). If the employee still does not wish to take part, they'll need to manually opt-out again.

When you contribute to an employee's pension, both the company and your employees benefit from tax relief on contributions.

How this works (and how much tax you'll save) depends on how you decide to process your contributions. You have three options for arranging pension contributions:

It's up to you to decide which method you prefer. In the next section, we'll outline how each of these approaches works.

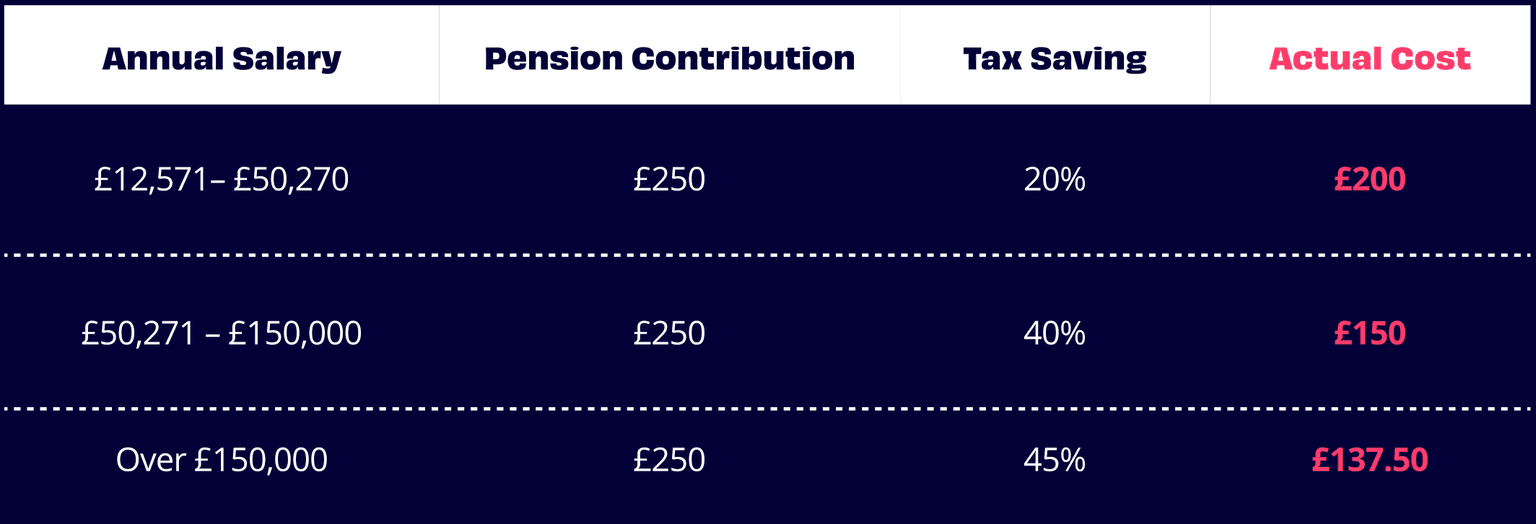

Net pay

With Net Pay, you'll take out your employee's pension contribution from their monthly wage before they pay any income tax. When you run payroll, each employee will receive their regular salary minus their pension contribution. Your company's contribution will be added separately and will show up on their payslip as ‘Employer Pension’ or ‘ER Pension’.

Because the contribution is taken from their gross (pre-tax) pay, they get full tax relief automatically — no need to fill out forms or claim anything separately. It’s all sorted through payroll.

That means basic, higher, and additional rate taxpayers all get tax relief at their full rate straight away. The only exception is for employees who don’t earn enough to pay income tax — they won’t receive any tax relief through Net Pay.

Here’s what that looks like for a £250 contribution.

The Net Pay approach reduces your employee’s take-home pay — but only because they’re paying less tax. In the long run, they keep more of what they earn by saving into their pension.

Relief at source

Relief at Source means pension contributions are taken out of an employee's salary AFTER they've paid tax on their earnings.

Here's how it works. First, income tax and National Insurance will be deducted from the employee's salary as normal. You will then take the employee's pension contributions from their pay before it arrives in their bank account. After tax, but before it reaches your team. Again, contributions from your company happen separately. Your pension provider will then claim tax relief back from the government at the basic rate.

For anyone earning under £50,270, that means they'll save 20% tax on everything they pay in. It's worth noting that employees won't receive any tax relief on the employer contribution - more on this later. This automatic tax relief applies even to those who don't pay any income tax - making it a fantastic way to boost pension savings.

Let's say you want to add £100 into your pot. £80 will come from their salary, with the remaining £20 coming from the government as a tax top-up. Higher earners can claim even more back - but will need to do this themselves via a self-assessment tax return.

One more benefit is that any extra tax relief claimed from their tax return doesn't have to go into their pension. It can simply be removed from their tax bill or even taken as a tax rebate.

One final type of pension arrangement available is salary sacrifice. This is a government-backed scheme where employees can swap part of their salary for regular pension contributions. Instead of employees paying into their pension from their monthly earnings, the entire pension contribution will come from you, the employer.

They voluntarily 'sacrifice' a portion of their earnings, reducing their overall salary in favour of having more money in their pension. Essentially, this works the same way as the Net Pay approach with one key difference - the employee technically isn't contributing to their pension themselves. This also helps save on National Insurance.

Pension contributions don't just help employees pay less tax. They also benefit the employer.

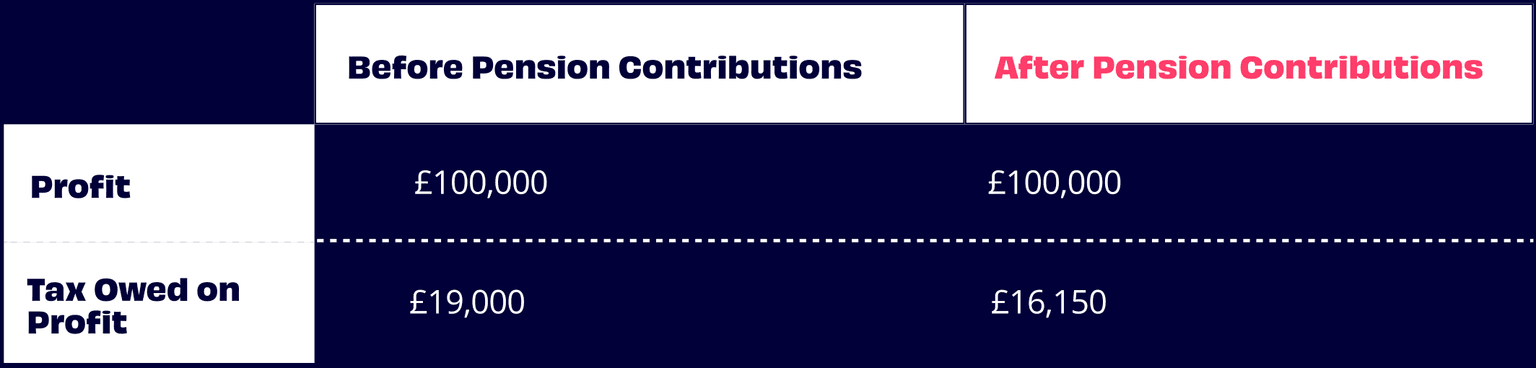

Employer contributions are an allowable business expense that can be deducted from any profit your company makes. This means that despite being a legal requirement, you can use pension contributions to reduce your company's profit and pay less corporation tax.

Let's say your company accounts show £100,000 profit for their year. Normally, your employer would owe 19% corporation tax on that figure - totalling £19,000. If your company contributions total £15,000 for the year. You can add this as an expense, meaning you'll now only owe £16,150 on your £100,000 profit. Just by deducting your pension contributions, you've saved £2,850 on your tax bill.

Another way to maximise tax relief from your workplace pension is by setting up a salary sacrifice scheme as outlined earlier. As the entire pension contribution comes from the company, you’ll benefit from more tax relief on National Insurance per employee. You’re contributing more, so you’re saving more.

Ok, now we know more about how workplace pensions work, you're ready to organise your own pension scheme.

How do you actually go about setting up a workplace pension for your employer?

1. Pick your pension provider. First of all, you'll need to choose your workplace pension provider. This is a third party company that will manage your pension for you. They'll collect all your company pension contributions and make sure each employee's savings are invested in line with their wishes. They'll also help your employee with pension withdrawal when they reach retirement age.

2. List your eligible employees. Next up, you'll need to work out who you're going to enrol. Using this guide as well as resources from the government, you can filter your workforce so you know who you'll need to add to your pension scheme. Save the list and send it to your new provider.

3. Let your team know. Once your pension scheme is ready to go, you'll need to let your employees know the details, including:

Your pension provider should be able to help with this.

4. Declare your compliance. Finally, you'll need to let the Pensions Regulator know your auto-enrolment scheme is fully compliant. Again, your pension provider should lend a hand but it's your responsibility to send your declaration of compliance within five months. If not, you could face a fine.

If you're still unsure about how to get started or have any questions, we'd love to help. Request information and we'll be more than happy to help you get your scheme up and running.