The flexible pension for freelance parents

Being a freelancer or running your own business can be stressful. Arranging a pension falls entirely on your shoulders and it can be difficult to make contributions with an unstable income.

Solve these headaches with Penfold's easy-to-use pension plan. Contribute flexibly, get automatic tax relief and use our specialist transfer service to combine old pensions for you.

Sign up below and get a £25 bonus from us.

As with all investments, your capital is at risk.

Earn a £25 bonus

Frankie & Steve have been friends with Penfold since the beginning. To thank them, we're offering their friends and the entire DIFTK community a £25 bonus to kickstart their Penfold pension.

To get your bonus simply set up your contribution - finish setting up your Penfold pension with a contribution, either through Direct debit or bank transfer. We'll add a £25 bonus into your pension once your first payment ha been completed.

Rewarding, simple and easy to understand - we take the stress out of saving for later.

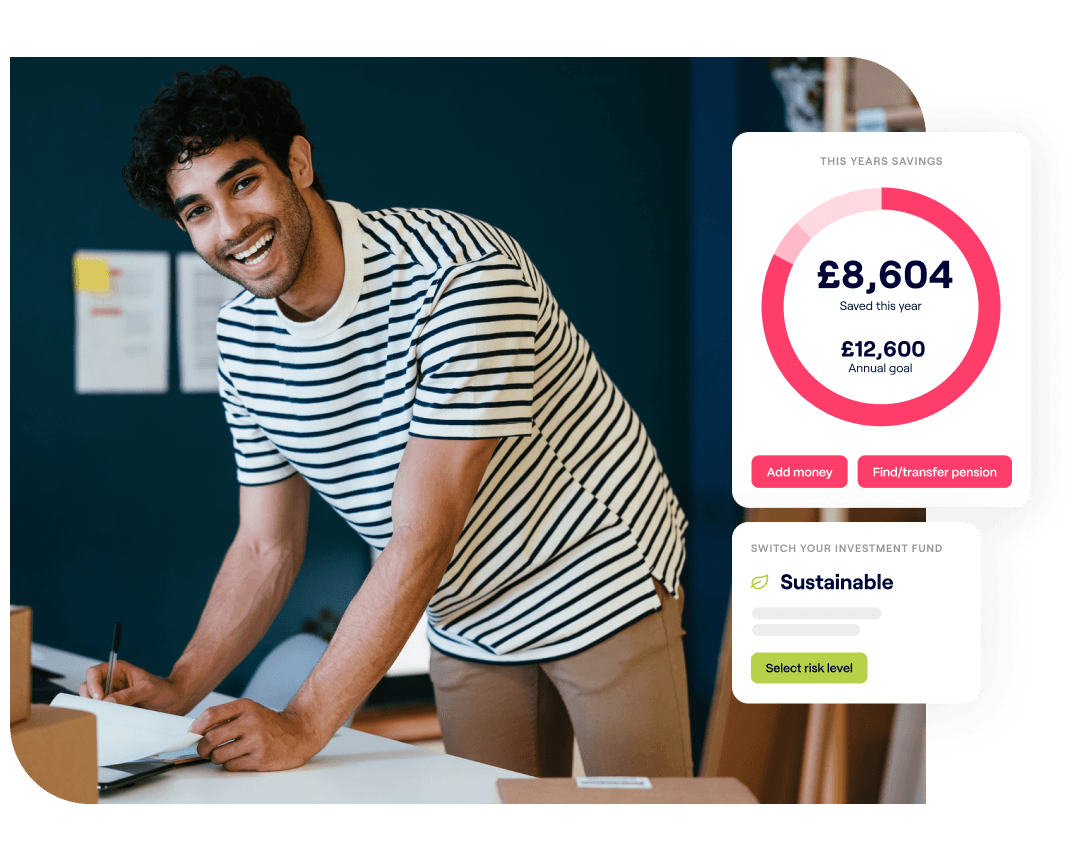

Simplified savings

Running a business likely leaves you short on time, research says that only 14% of self employed people are saving into a pension. You might be focused on the day to day needs of your business, but it’s important to think about the future too.

Employees reap the tax rewards of a pension automatically, thanks to pre-tax contributions from their employer. What many don't realise is that the self-employed can take advantage too - you just need to start your own pension first.

That’s why we built a modern pension that takes only 5 minutes to set up and is effortless to use. Contributions can be made whenever you like, we automatically apply tax relief and you can choose four high performing funds to grow your savings.

Flexible contributions

Whether you’re a freelancer, sole-trader, contractor or business owner your earnings probably aren’t easy to forecast.

Penfold is designed to adjust to your finances. Once you’re set up you can change, top-up, or pause payments instantly and at any time. If you’re unsure about how much to contribute, our pension calculator will help you decide how much to save to get the retirement you want.

Even better - self-employed workers get a 25% tax relief top-up on contributions. We organise this for you, automatically adding it to your pension. Subject to annual allowance. Tax treatment depends on individual circumstances and may change in the future.

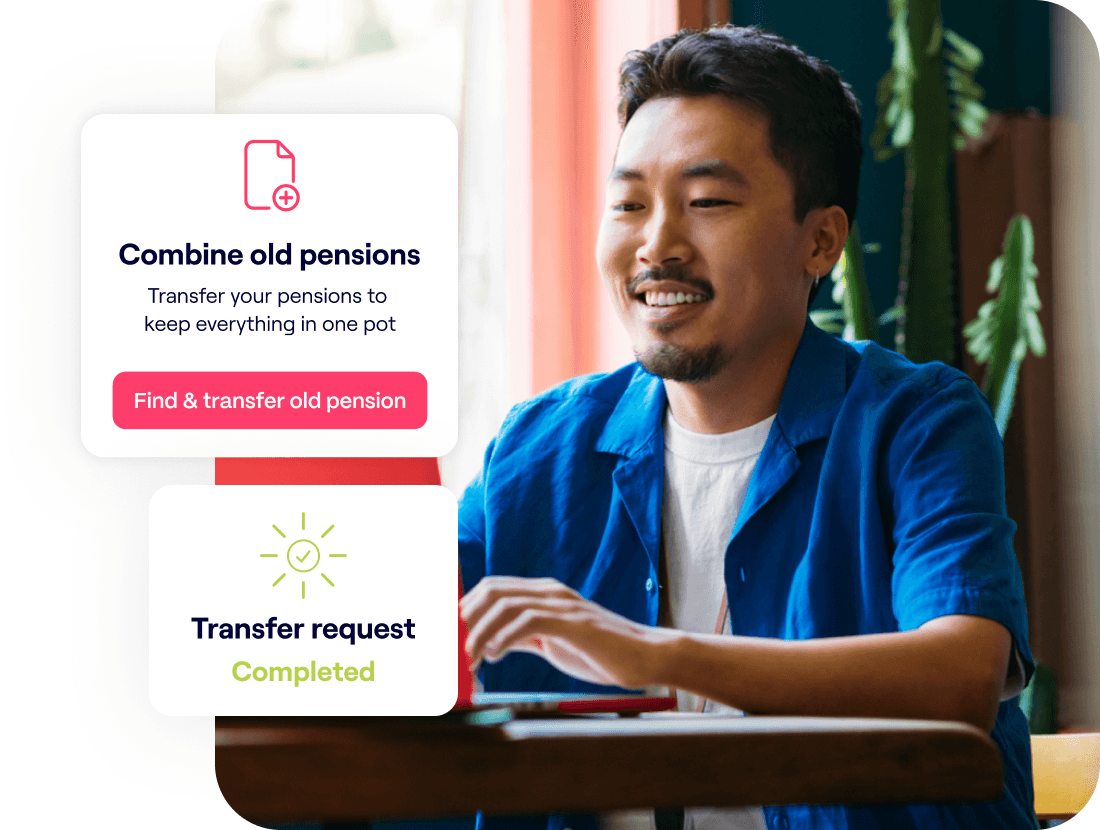

Transfer and combine

Previously worked as an employee? You probably have old workplace pensions that make it difficult to understand how much you have saved, and need to save, for retirement. There's the added stress of managing multiple old accounts and your savings may be invested in poor performing funds by default.

Combine your old pensions into a single Penfold account and you'll easily be able to see the total value of your savings and have access to our top performing funds. Transferring is free and our specialist team will manage it for you.

Once you've requested a pension transfer, we'll contact your previous providers and do the hard work for you. You'll be able to stay up to date with progress any time on your Penfold dashboard.

It’s important to compare providers’ fees and any guaranteed benefits when deciding on whether to transfer, and be sure that the investments available are suitable for you. If your employer is paying into your pension currently, transferring that pot may mean you lose out on their contribution.

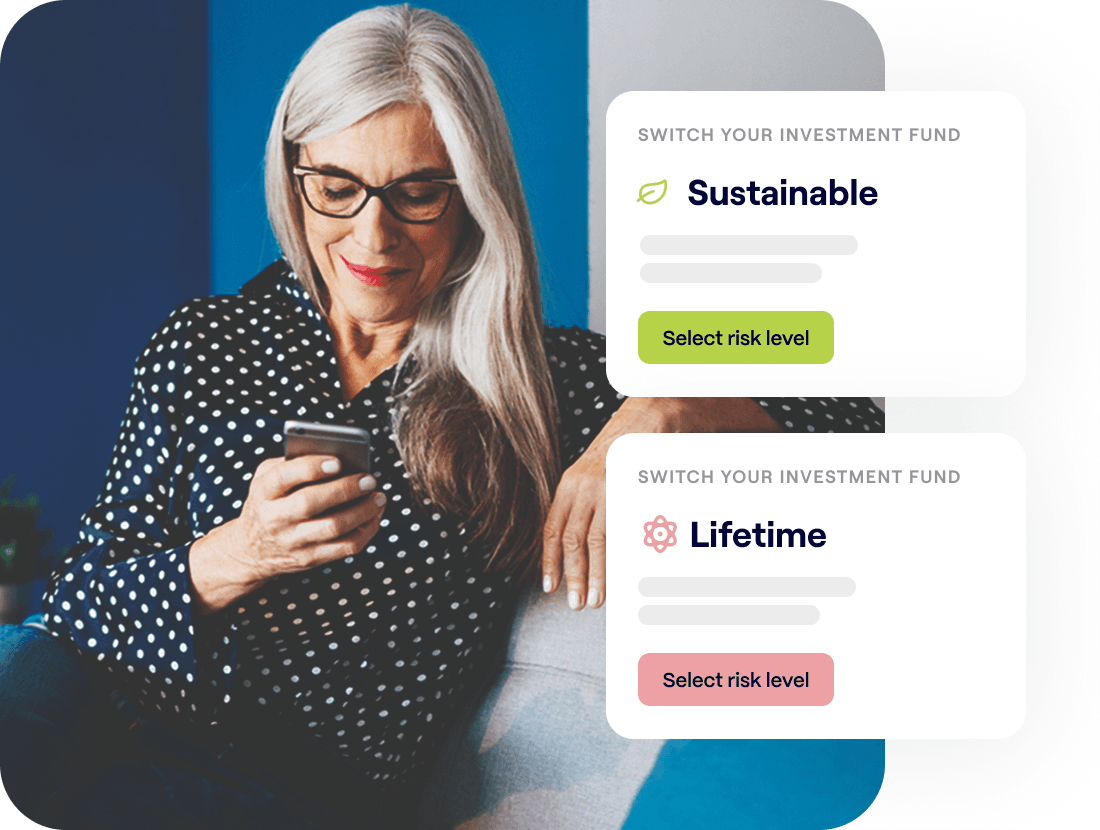

Hand-picked fund selection

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice and past performance is not a reliable indicator of future performance.

Your new pension

Once set up you'll get access to our modern online account and app.

Find out how your pension is performing in real time

See details of our other investment plans and switch easily

Easily withdraw via drawdown, an annuity or even taking a lump sum

If you have any questions our friendly team of pension experts will be happy to help. Simply message us on our in-app chat, email or call - we promise no jargon!