Do I pay tax on my pension?

Pensions are tax-efficient savings subject to income tax upon withdrawal. Find out what that means in our simple guide to pensions and tax.

10 May 2026

5 min read

Pension tax rules can be confusing. This is particularly frustrating when you remember a pension is essentially a tax-efficient way to save.

In this article, we'll look at everything you need to know about paying tax on your pension.

Pensions and tax - the two go together like bangers and mash. And, while you'll get to enjoy tax relief as you're paying into your pot, you may be wondering if you have to pay tax back when it comes time to take money out.

The short answer? Yes. You'll need to pay income tax on your pension when you're ready to access your pot. How much tax you pay depends on your total annual income. But that's only part of the story.

Withdrawals from your pension may be taxed as income.

How much income tax you'll pay on withdrawals depends on the type of pension, as well as how you choose to withdraw from your pot. Let's look at how it all works.

Ok, so now we know you may need to pay tax to access your savings, you're probably asking yourself: how much tax do I pay on my pension? Let's start by looking at lump sums.

25% of your pension pot can be taken out tax-free

The good news is, you can usually take out 25% of your total pot without paying a penny in tax. This is called the tax-free lump sum.

For most, this 25% is a one-and-done deal. Once you've taken it out, the rest of the money you take from your pension will be taxed as income, like a salary from a regular job. That means the amount you owe in tax depends on the size of your pot and how much you'd like to withdraw.

The only exception to this rule is something called uncrystallised lump sums. This is where instead of taking one big tax-free payment from your pension in one go, you take the tax off of each withdrawal on an ad-hoc basis.

Using this method, 25% of each withdrawal is tax-free, with the remaining 75% being taxed as normal.

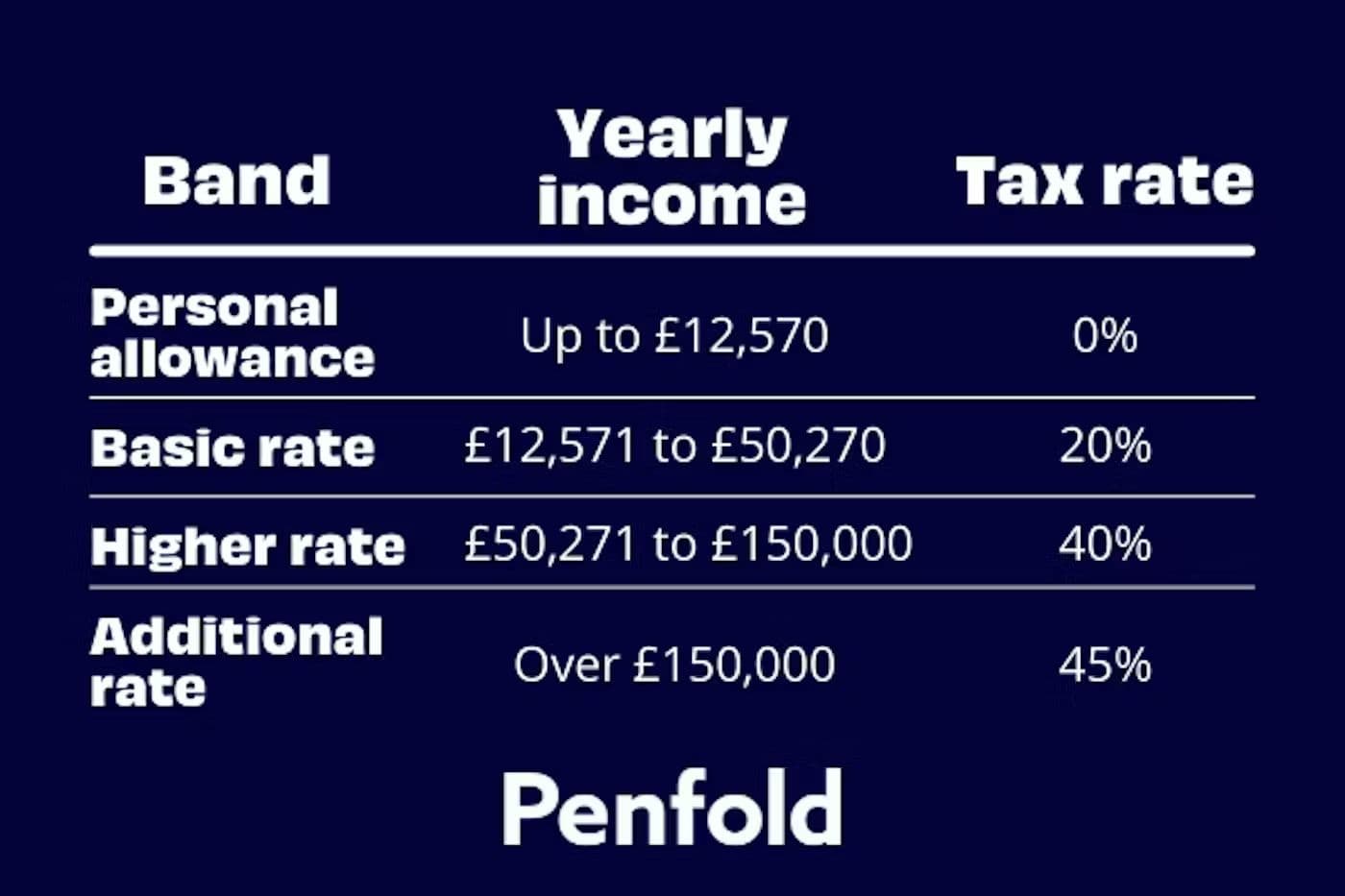

The first £12,570 each year comes under your Personal Allowance. This is the amount a pensioner can earn before they have to pay tax.

Anything you withdraw that puts your total annual income above this threshold however will be liable to income tax. At the basic rate, this means you'll need to pay 20% back to the government yourself.

Withdrawing higher amounts may also push your income into the higher and additional tax bands. Here's a reminder of the limits.

When you're ready to access your pot, you need to be aware of all the pension withdrawal tax rules to save yourself any surprise pension savings tax charges.

The other thing to keep in mind is how you're accessing your pot. Choosing to take your pot at regular intervals, known as drawdown, will incur pension drawdown tax, payable as income like we outlined above.

Or, if you'd like to pass your pot on to a beneficiary, you'll need to check what happens with pension inheritance tax.

No, you don't need to pay any National Insurance contributions on any withdrawals from your pension. Payments from your pension scheme only require you to pay income tax.

As with any private or workplace pensions, any payments from your State pension are liable to income tax.

Unlike a salary from a job, your State pension payments without any have tax deductions beforehand.

As we outlined above, the amount you'll owe back will depend on your total annual income. You'll need to look at your total annual income (including private and workplace pensions) to work out how much you owe.

Now we know how pension tax works, let's look at how you can keep your pot tax efficient.

The fundamental rule is this: the more you withdraw from your pot, the more you'll owe in tax. But is there any way you can reduce how much of your pension goes on tax? Is there such a thing as a tax-free pension?

As we touched on earlier, 25% of your pot is available as soon as you withdraw, completely tax-free. This is a great way to get your hands on a nice chunk of your savings right away.

However, it's worth remembering that each withdrawal you make after this initial lump sum will be taxed as income.

So, if you're looking to trim the tax you'll have to pay on your pension, your best option is to keep your withdrawals as low as possible. Work out how much you need each year for a comfortable retirement and stick to this amount.

This is where income drawdown can come in handy. You can change how much you take from your pot each year to match what you think you'll need. That way, more of your pot will go to good use, rather than be wasted on tax.

For example, let's say you take £25,000 out of your pension in year 1 to pay for a new car and a well-earned holiday. You'll owe £2,486 as income tax. If you take the same amount the. next year but only spend £20,000, you've essentially overpaid tax by £1,000. That's why it's usually best to only take out what you need.

Alternatively, if you'd like to only dip into your pot on a less regular basis, you may want to explore taking a series of uncrystallised pension fund lumps sums.

If you think you've overpaid on a pension withdrawal, you'll need to ask the government for a pension tax refund.

Thankfully, this is a (fairly) straightforward process. You'll need to head here, fill in a P53 or P53Z form and send it off. The government will then process your application and get back to you as soon as they can.