How does pension tax relief work if I’m self-employed?

Learn how self-employed pension tax relief works, how much HMRC adds to your pension, how higher-rate relief is claimed, and how much you can pay in.

20 April 2026

10 min read

One of the biggest benefits of paying into a pension is tax relief. But when you’re self-employed, it’s not always obvious how pension tax relief works, how much HMRC adds, or how you claim anything extra back through your tax return.

The good news is that pension tax relief can make saving for retirement much more affordable. In most cases, when you pay into a personal pension or SIPP, HMRC adds basic-rate tax relief automatically. If you’re a higher-rate or additional-rate taxpayer, you may be able to claim more tax relief yourself.

In this guide, we’ll explain how self-employed pension tax relief works, how much you can get, what you need to claim through Self Assessment, and how much you can usually contribute each year.

A self-employed pension is usually a personal pension or Self-Invested Personal Pension (SIPP) used by people who work for themselves. This includes freelancers, sole traders, contractors, consultants and some small business owners.

Unlike employees, self-employed people do not usually have an employer setting up a workplace pension or paying employer contributions on their behalf. That means it’s your responsibility to choose a pension, decide how much to pay in, and keep your retirement savings on track.

The upside is flexibility. A personal pension can move with you as your work changes, and you can usually increase, reduce, pause or restart contributions depending on your income.

Pension tax relief is a government top-up on your pension contributions.

With most personal pensions, including Penfold, contributions are made using what’s known as relief at source. This means you pay money into your pension from your take-home income, and your pension provider claims basic-rate tax relief from HMRC on your behalf.

That tax relief is then added to your pension.

The easiest way to think about it is this:

For every £80 you pay into your pension, HMRC adds £20, turning it into a £100 gross pension contribution.

Or, put another way:

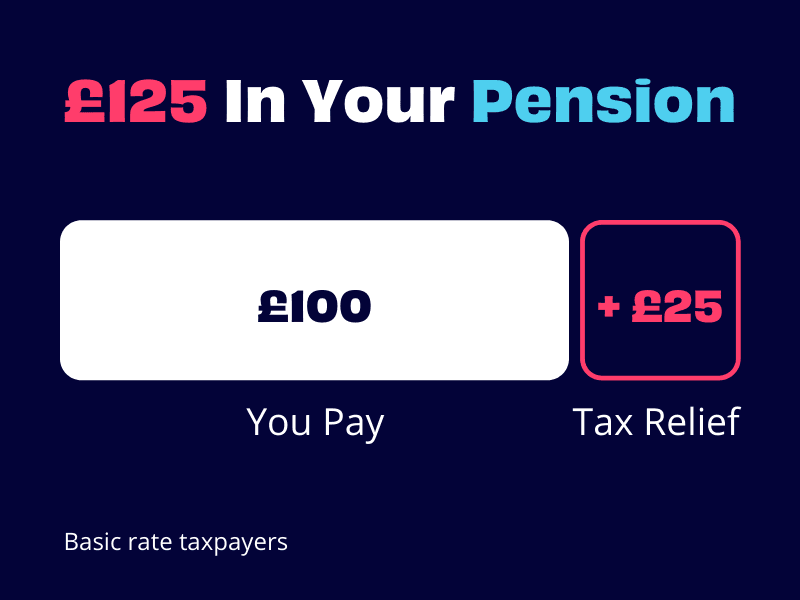

Every £100 you personally pay in becomes £125 in your pension after basic-rate tax relief is added.

This is why pension tax relief is often described as a 25% top-up. The tax relief itself is 20% of the gross contribution, but because it is added on top of your net payment, it feels like a 25% boost.

Let’s say you’re self-employed and pay £100 into your pension.

Your pension provider claims basic-rate tax relief from HMRC.

HMRC adds £25.

Your pension receives £125 in total.

So your £100 contribution becomes £125 before any investment growth.

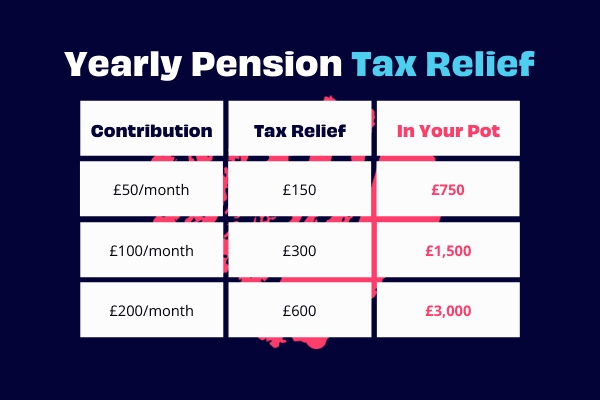

Over a year, that can make a big difference:

This basic-rate tax relief is normally claimed automatically by your pension provider, so you do not usually need to do anything extra to receive it.

Basic-rate pension tax relief is usually added automatically if your pension uses relief at source.

That means your pension provider claims the tax relief from HMRC and adds it to your pension. You do not need to claim basic-rate relief separately through your Self Assessment tax return in most cases.

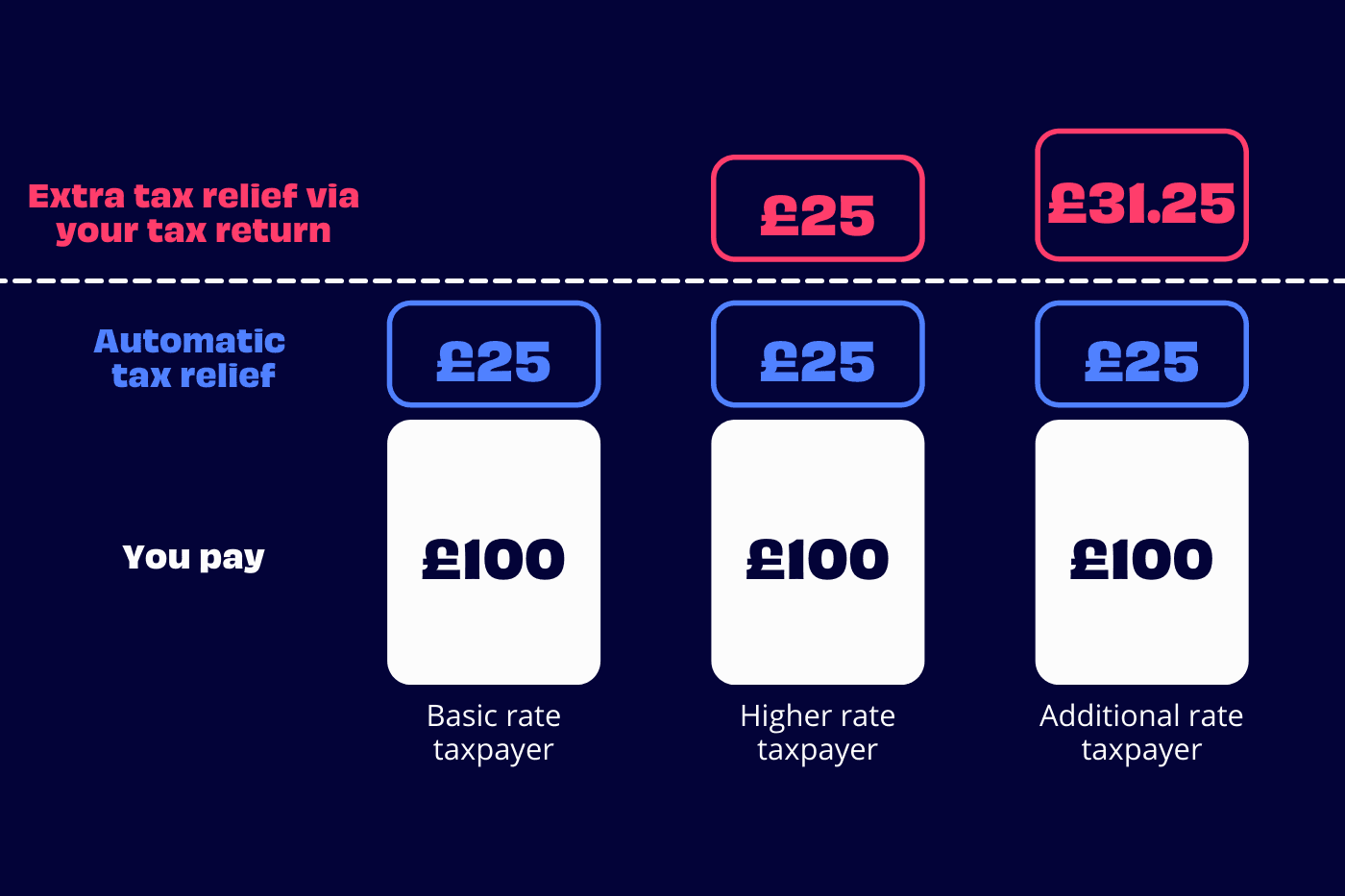

However, if you pay tax above the basic rate, you may need to claim the extra tax relief yourself.

If you’re self-employed and pay higher-rate or additional-rate income tax, you may be able to claim higher-rate pension tax relief.

Your pension provider will usually only claim basic-rate tax relief for you. Any extra relief is claimed by you, usually through your Self Assessment tax return.

For example, if you’re a higher-rate taxpayer:

You pay £800 into your pension.

HMRC adds £200 basic-rate tax relief.

Your pension receives £1,000 in total.

Because you pay 40% income tax, you may be able to claim a further 20% tax relief on the gross contribution.

That could reduce your tax bill by up to £200, depending on your income and circumstances.

So a £1,000 gross pension contribution could effectively cost you £600 after all available tax relief.

If you’re an additional-rate taxpayer, you may be able to claim even more relief.

Your pension provider still usually claims the first 20% basic-rate relief from HMRC. You then claim the additional relief yourself, normally through Self Assessment.

For a 45% additional-rate taxpayer, total pension tax relief can be worth up to 45% of the gross contribution, depending on your income, contribution level and available allowances.

If you complete a Self Assessment tax return, you can usually claim higher-rate or additional-rate pension tax relief by entering your pension contributions on your return.

You’ll normally need to include the gross pension contribution. This is the amount you personally paid in plus the basic-rate tax relief added by HMRC.

For example:

You pay £800 into your pension.

HMRC adds £200.

Your gross pension contribution is £1,000.

The £1,000 figure is the amount you would usually include on your tax return.

If you’re unsure, check your pension statement or provider dashboard, as this should show your contributions and tax relief.

Usually, no.

If you’re a sole trader, your personal pension contributions are not normally treated as an allowable business expense. Instead, they receive tax relief through the pension tax relief system.

That means you usually make contributions personally, your pension provider claims basic-rate relief, and you claim any higher-rate or additional-rate relief through Self Assessment.

This is different from limited company pension contributions.

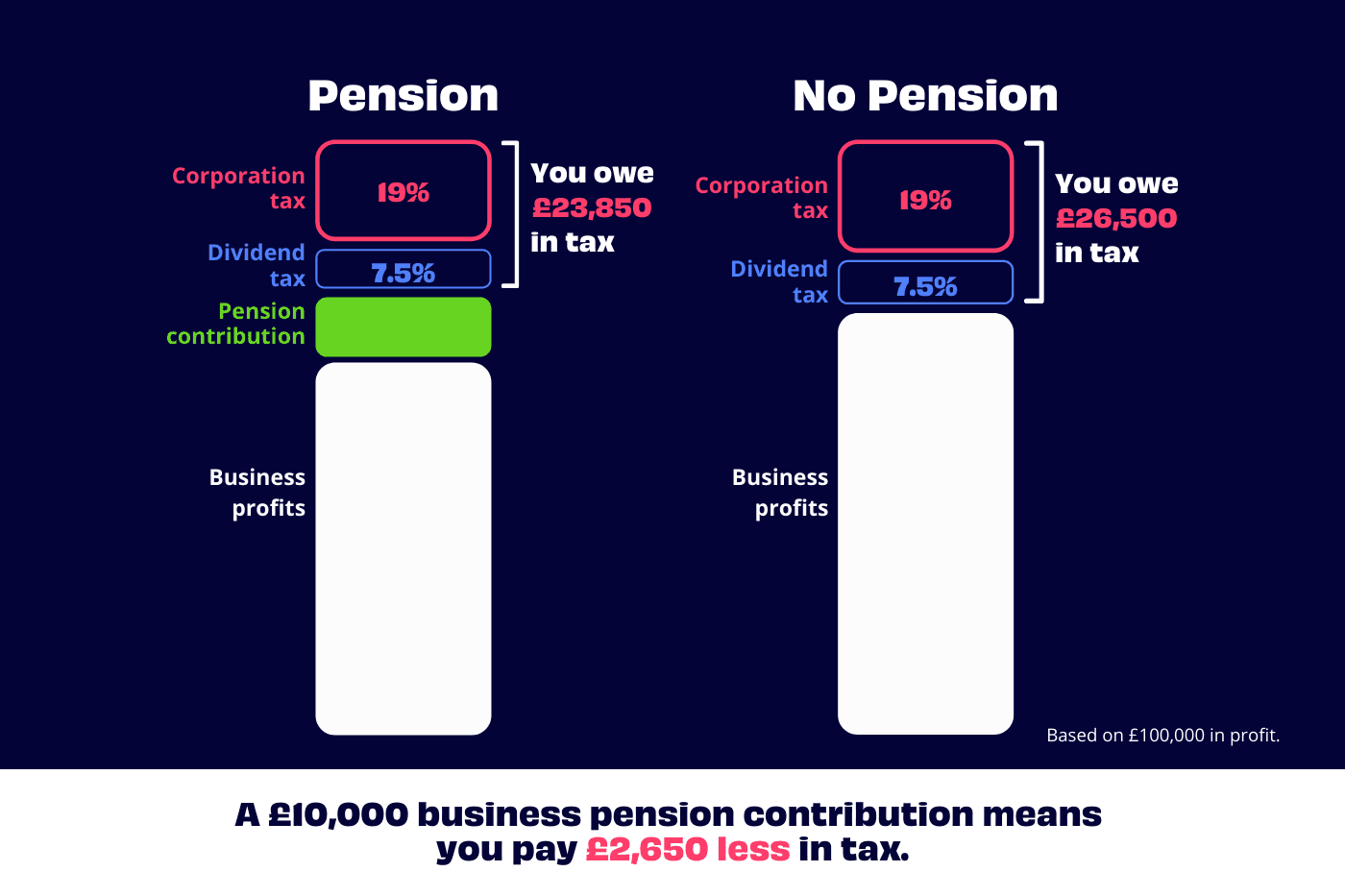

If you run your own limited company, pension contributions can work differently.

Instead of paying personally into your pension, your company may be able to make employer pension contributions directly from the business account.

These contributions can usually be treated as an allowable business expense, provided they meet HMRC’s rules. This means they may reduce your company’s taxable profits and therefore its corporation tax bill.

Company pension contributions can also be more tax-efficient than taking money out of the business as salary or dividends and then making personal contributions.

However, company contributions need to be handled correctly, and the rules can depend on your circumstances. It’s worth speaking to an accountant before deciding the best approach.

There are two main limits to think about:

In most cases, you can receive tax relief on pension contributions up to 100% of your relevant UK earnings, subject to the annual allowance.

For self-employed people, relevant UK earnings usually means taxable profits from your trade, profession or vocation.

The standard annual allowance is currently £60,000. This includes your own contributions, tax relief added by HMRC, and any employer contributions.

So if you’re a sole trader with taxable profits of £40,000, your tax-relievable pension contributions will usually be limited by your earnings rather than the £60,000 annual allowance.

If you’re a higher earner, your annual allowance may be reduced by the tapered annual allowance. If you’ve already accessed some of your pension flexibly, you may also be affected by the money purchase annual allowance.

Even if you have little or no relevant UK earnings, you can usually still pay up to £2,880 net into a pension each tax year.

HMRC then adds basic-rate tax relief of £720, giving you a total gross pension contribution of £3,600.

This can be useful if you’re taking time out, have a quieter trading year, are starting a new business, or want to keep contributing while your income is lower.

Yes. Self-employed pension contributions are usually flexible.

You can contribute monthly, make one-off payments, or do both. You can also pause or change contributions as your income changes.

This flexibility is important when you work for yourself because your income may not be the same every month.

For example, you might choose to:

With Penfold, you can make contributions by Direct Debit or debit card, giving you control over how and when you save.

You can pay into your pension at any point during the tax year.

Some self-employed people prefer regular monthly contributions because it builds the habit of saving. Others prefer lump-sum contributions once they have a clearer picture of their annual profits and tax bill.

A common approach is to review your pension contributions before the end of the tax year, especially if you’ve had a strong year and want to make use of available tax relief.

The tax year runs from 6 April to 5 April, so contributions usually need to be made before the deadline to count for that tax year.

For many self-employed people, a pension is one of the most tax-efficient ways to save for retirement.

That’s because:

The main trade-off is access. Pension money is designed for retirement, so you usually cannot withdraw it until later life. That means it’s important to balance pension saving with cash savings, emergency funds and money set aside for tax.

Yes. Self-employed people can usually get tax relief on personal pension contributions, provided they meet HMRC’s rules. Basic-rate tax relief is normally added automatically by the pension provider, while higher-rate and additional-rate relief may need to be claimed separately.

Most people get basic-rate tax relief added automatically. This means every £80 you pay in becomes £100 in your pension. Higher-rate and additional-rate taxpayers may be able to claim extra relief through Self Assessment.

If you’re a basic-rate taxpayer and your provider has already claimed tax relief, you may not need to claim anything extra. But if you’re a higher-rate or additional-rate taxpayer, you’ll usually need to include pension contributions on your Self Assessment tax return to claim the extra relief.

You’ll usually enter the gross contribution. This is the amount you paid in plus basic-rate tax relief. For example, if you paid £800 and HMRC added £200, the gross contribution is £1,000.

If you’re a sole trader, personal pension contributions are not usually treated as a business expense. They receive tax relief through the pension tax relief system instead. If you run a limited company, employer pension contributions made by the company may be treated as a business expense.

In most cases, you can receive tax relief on pension contributions up to 100% of your relevant UK earnings, subject to the annual allowance. The standard annual allowance is currently £60,000, although this may be lower for some high earners or people who have already accessed their pension flexibly.