Start 2025 right… with all your pensions in one place

One thing you don’t want to carry into the new year? Scattered pension pots.

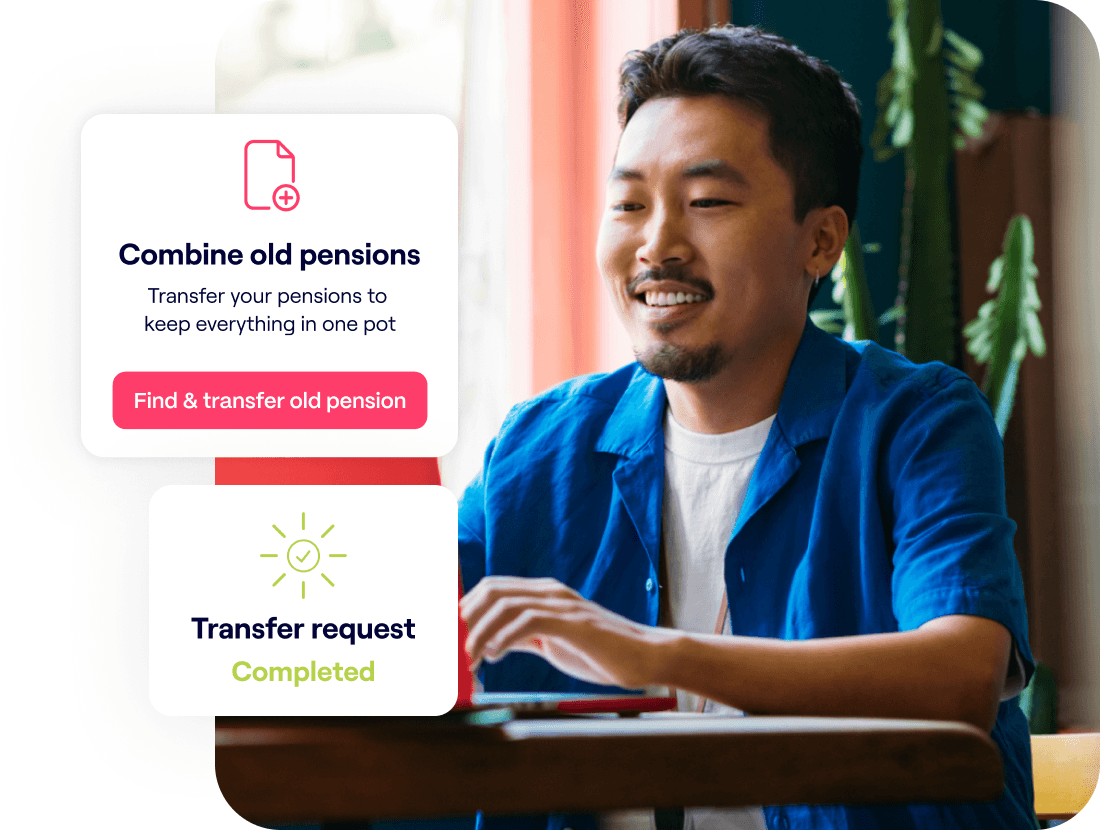

The solution? Combining your pensions.

Figure out if a pension transfer is right for you. Once decided, take just five minutes to make a transfer request in the Penfold app – and start 2025 with all your pensions in one, easy-to-manage place.

Capital at risk. Check for loss and benefits and exit fees.

Consider these things

- Pension transfer fees

We won’t charge you if you transfer your pension to us. However, your existing pension provider might have an exit charge. Be sure to check with them first

- Guarantees and benefits

Some pensions also offer special benefits or guarantees which you might lose if you transfer your pension. Check with your provider

- Potential loss of value

Your savings will be taken out of the market to be moved. So, there is a risk you could lose out on market growth and have less than you had before

It’s important to compare providers’ fees and any guaranteed benefits when deciding on whether to transfer, and be sure that the investments available are suitable for you. If your employer is paying into your pension currently, transferring that pot may mean you lose out on their contribution.

We cannot accept defined benefit pension transfers. If you decide to close your Penfold account and the value of your pot has gone down, the amount returned to the provider may be less than what you originally transferred.

With investments, your capital is at risk. Pensions can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice and past performance is not a reliable indicator of future performance.

*Returns are based on data collected by investment advisors DWA from a variety of sources including individual providers and data published on Morningstar. These are annualised returns are based on data in the 5 years to 30 September 2024. Returns for Penfold are based on a customer being invested in our default Standard Lifetime plan. Competitor returns are based on customers invested in their default plans.

DWA have estimated the Gross Returns based on available information for a member with a typical pot size of £10,000 and an average salary of £30,000. DWA have estimated the Net Returns net of all costs and charges based on available information for a member with a typical pot size of £10,000 and an average salary of £30,000.

Actual returns may vary depending on a variety of factors including specific costs negotiated by a member's employer, actual pot size and actual salary. Where possible we have used actual return series available, though in assumptions have been made based on the underlying funds because of poor data availability and this may also result in some variance. The effect of charges have been applied to the return series on a monthly basis via a subtraction/addition of the proportionate amount, this may create small discrepancies with actual experience depending on charging structure. DWA are happy to correct any discrepancies should evidence be provided.

Helpful resources

Our carefully crafted blog posts and guides are designed to help you understand if you should combine your pension pots and how you can do it.