The perfect pension for directors

Running your own business can be stressful and leaves you short on time. Arranging a pension falls entirely on your shoulders and it can be difficult to make contributions with an unstable income.

Solve these headaches with Penfold's fast to set up, easy-to-use pension. Make tax-efficient contributions flexibly, in line with company cash flow. That's why we're Trustpilot's top rated retirement scheme.

With investments, your capital is at risk.

Optimise your finances

If you're a director or run a limited company you can make tax efficient pension contributions.

- Tax-free

Pension contributions from your limited company are classed as a business expense, so you won't pay any tax on these payments.

- Save up to 25%

Business contributions are deductible from your corporation tax bill. £1,000 paid into your pension cuts your tax bill by £190 to £250 depending on your Corporation Tax Rate.

- Maximise your allowance

Business pension contributions can be made without the tax-free salary restriction that most people are subject to.

Tax treatment depends on individual circumstances and may change in the future.

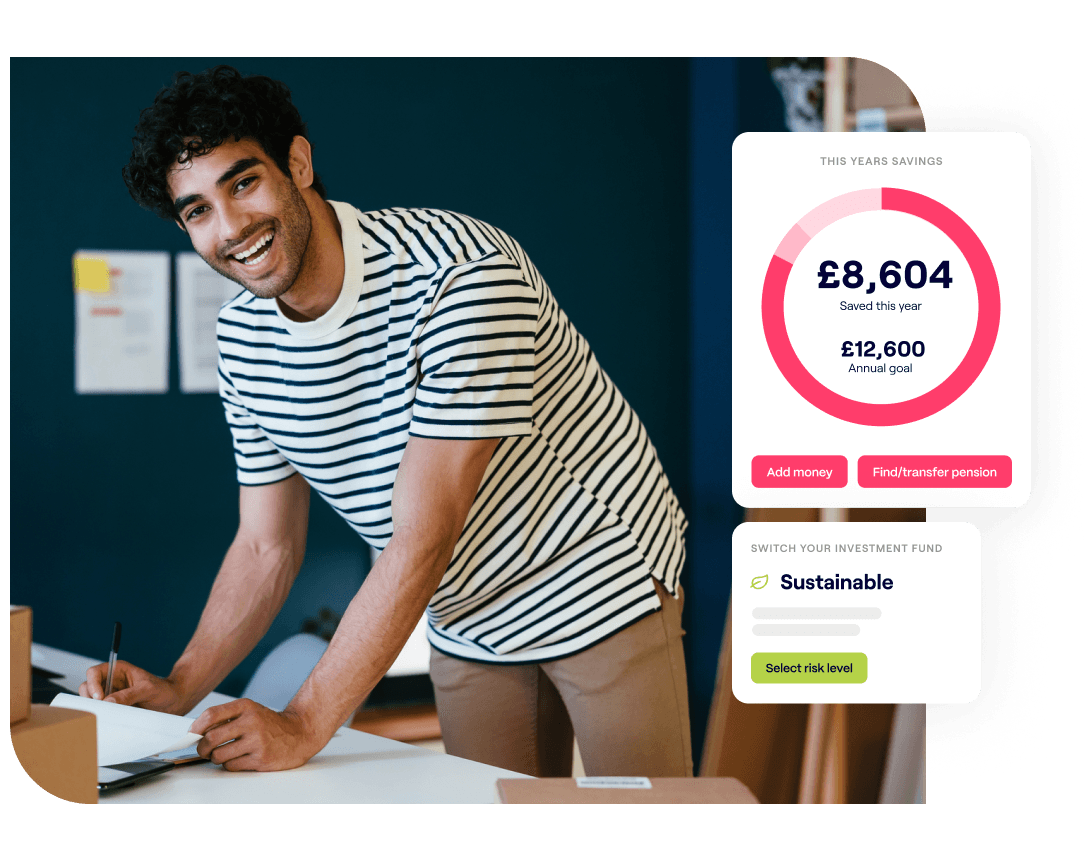

Flexible contributions

Whether you’re a freelancer, sole-trader, contractor or business owner your earnings probably aren’t easy to forecast.

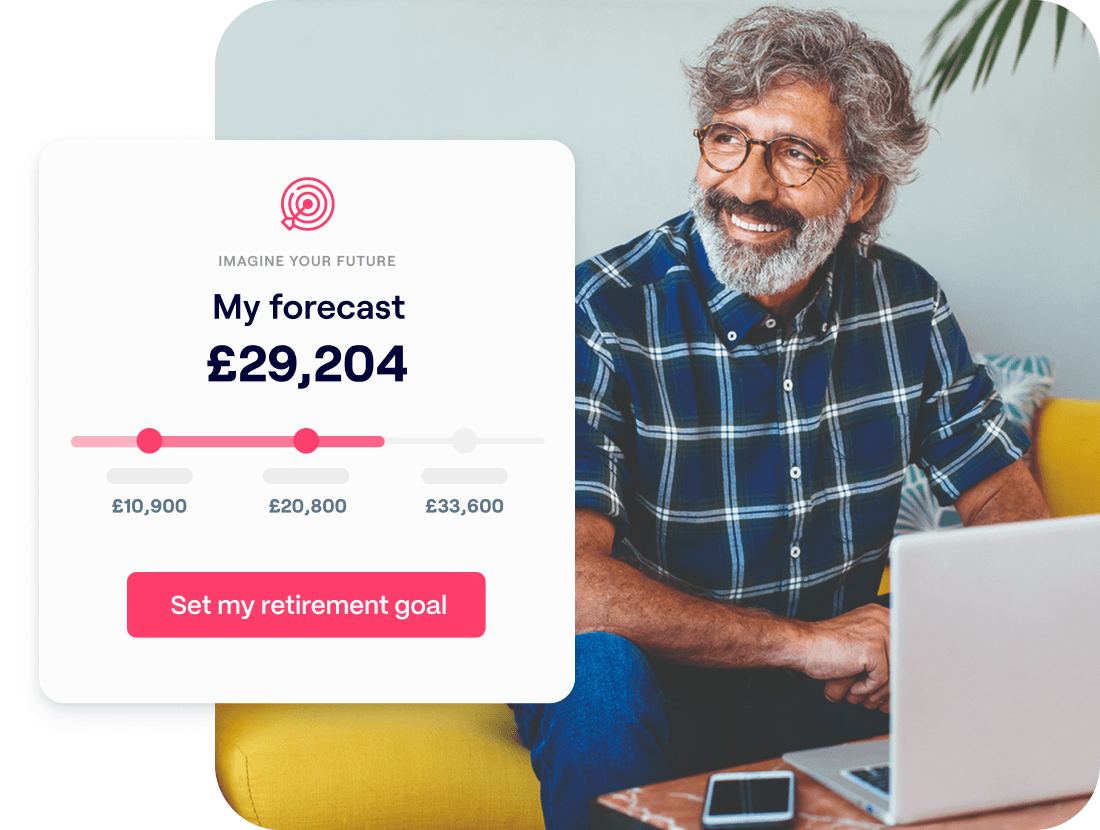

Penfold is designed to adjust to your finances. Once you’re set up you can change, top-up, or pause payments instantly and at any time. If you’re unsure about how much to contribute, our pension calculator will help you decide how much to save to get the retirement you want.

Even better - self-employed workers get a 25% tax relief top-up on contributions. We organise this for you, automatically adding it to your pension. Subject to annual allowance. Tax treatment depends on individual circumstances and may change in the future.

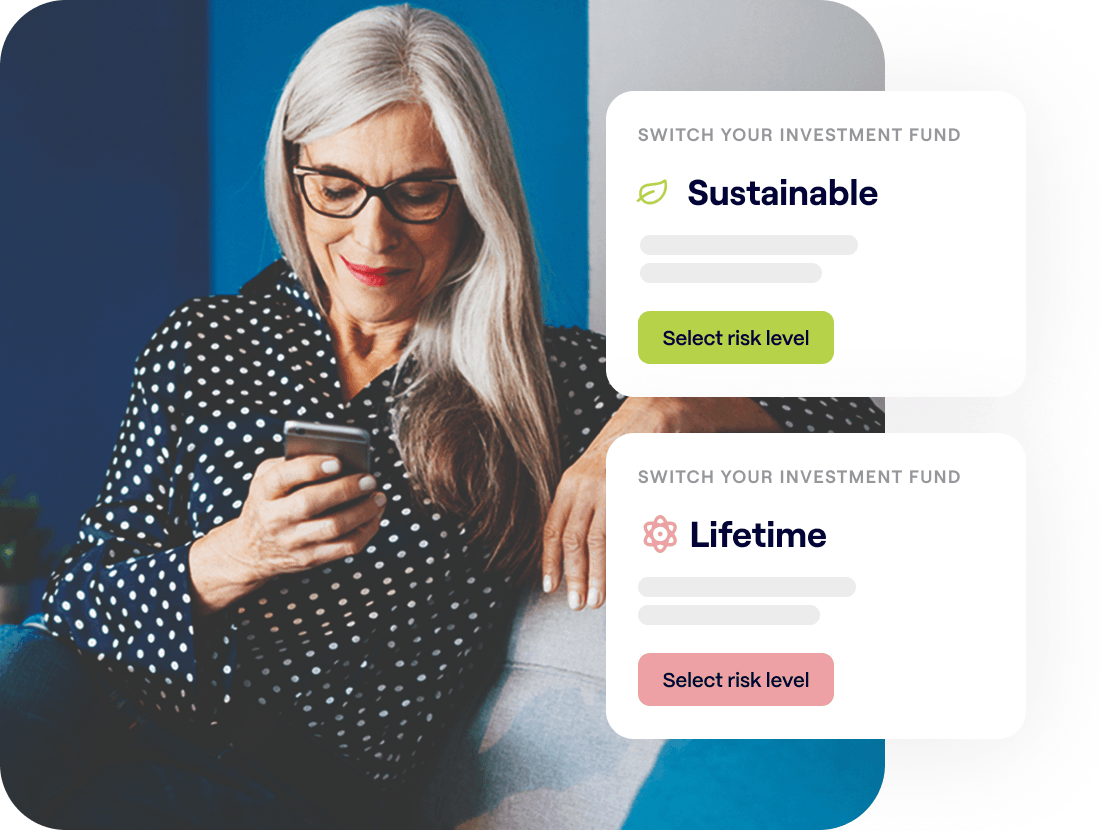

Hand-picked fund selection

With investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice and past performance is not a reliable indicator of future performance.

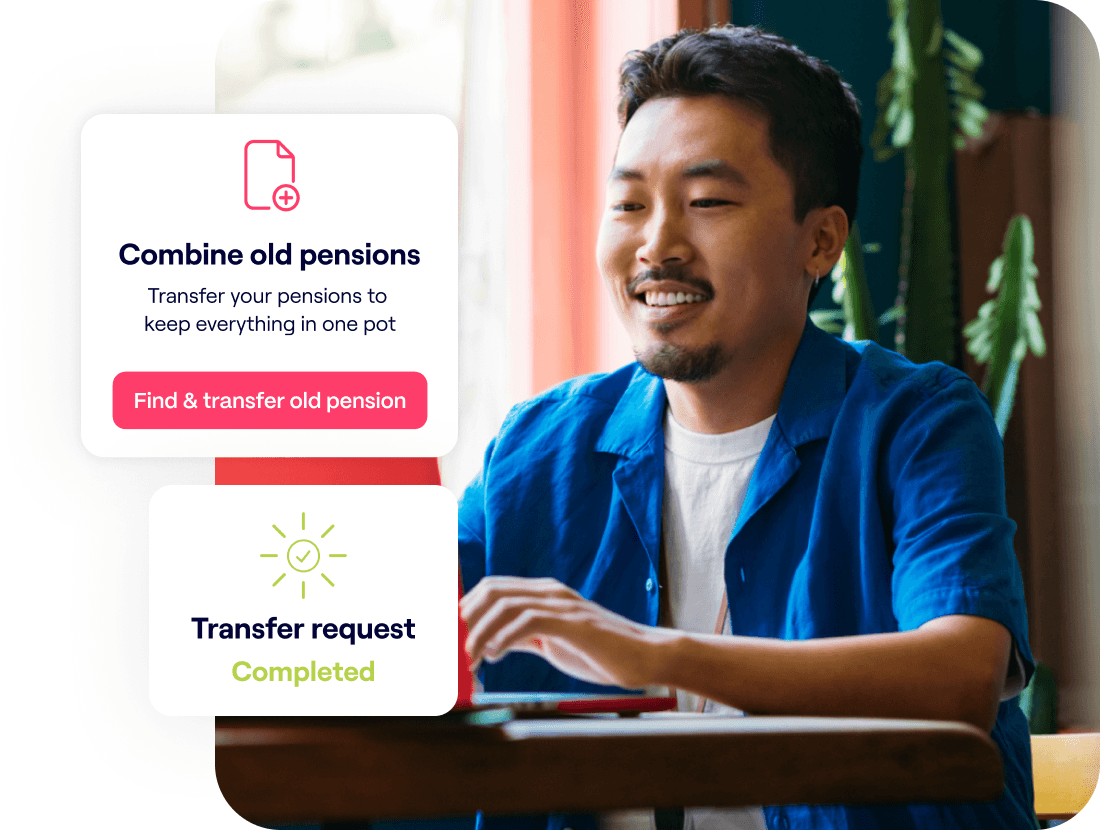

Transfer and combine

Previously worked as an employee? You probably have old workplace pensions that make it difficult to understand how much you have saved, and need to save, for retirement. There's the added stress of managing multiple old accounts and your savings may be invested in poor performing funds by default.

Combine your old pensions into a single Penfold account and you'll easily be able to see the total value of your savings and have access to our top performing funds. Transferring is free and our specialist team will manage it for you.

Once you've requested a pension transfer, we'll contact your previous providers and do the hard work for you. You'll be able to stay up to date with progress any time on your Penfold dashboard.

It’s important to compare providers’ fees and any guaranteed benefits when deciding on whether to transfer, and be sure that the investments available are suitable for you. If your employer is paying into your pension currently, transferring that pot may mean you lose out on their contribution.

Your new pension

Once set up you'll get access to our modern online account and app.

Find out how your pension is performing in real time

See details of our other investment plans and switch easily

Easily withdraw via drawdown, an annuity or even taking a lump sum

If you have any questions our friendly team of pension experts will be happy to answer them. They've helped thousands of directors and business owners with their pension arrangements. Simply message us on our in-app chat, email or call - we promise no jargon!