The perfect pension for your director clients

Get your clients set up in minutes and help them grow their savings in a tax-efficient way.

Penfold offers flexible, digital pensions built for limited company contributions that are simple to manage and quick to get set up.

As with all investments, capital is at risk.

What's in it for your clients?

By setting your director clients up with a modern and flexible pension, they can:

Make tax-free contributions: Pension contributions from a limited company are classed as a business expense, so your director clients won't pay any tax on these contributions.

Save between 19-25%: Business contributions are deductible from corporation tax bills. If your client's business makes a profit below £50,000 they can save the small profits rate of 19%. Therefore £1,000 paid into their pension cuts their tax bill by £190.

Use your allowance: For most people, pension contributions are capped at £60k or their yearly salary, whichever is lower. As a limited company director, your client's business can contribute into their pension without the salary restriction.

Tax treatment depends on individual circumstances and may be subject to change in the future.

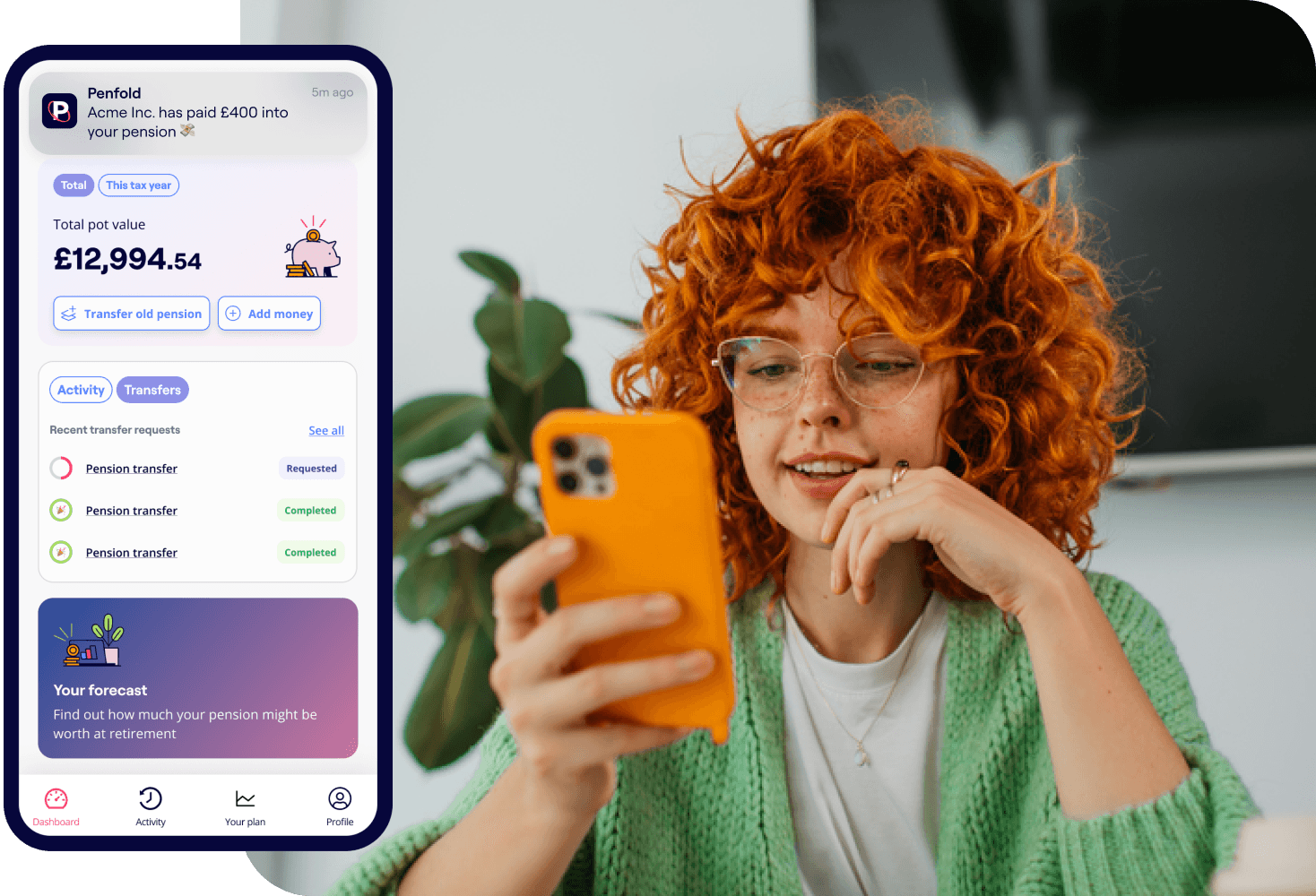

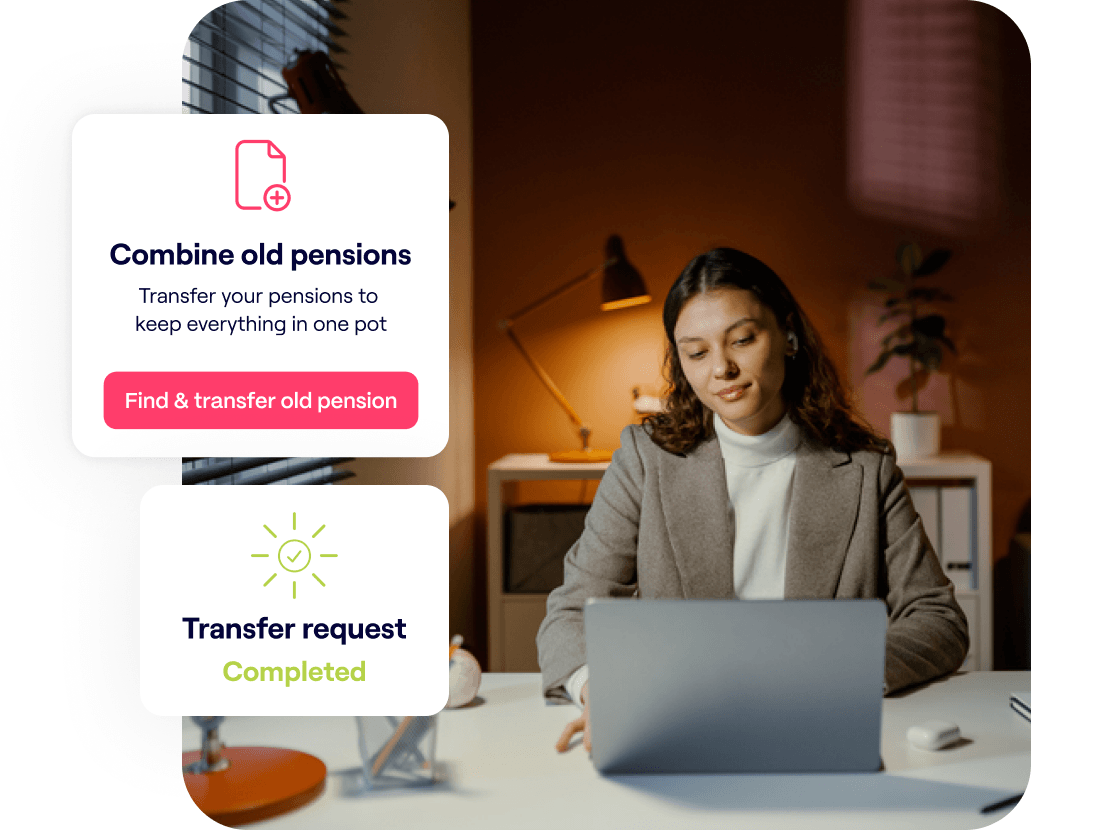

Combine old pensions

Transferring pensions to Penfold is easy, free of charge, and our expert team will manage it on behalf of you and your clients.

Got old pension pots? Transfer and combine in a couple of taps by entering the policy provider name and account number. Our team of pension transfer specialists will do the hard work for you.

Missing pension details? Use our Find My Pension service to find the provider and contact details, all we need is the name of your previous employer.

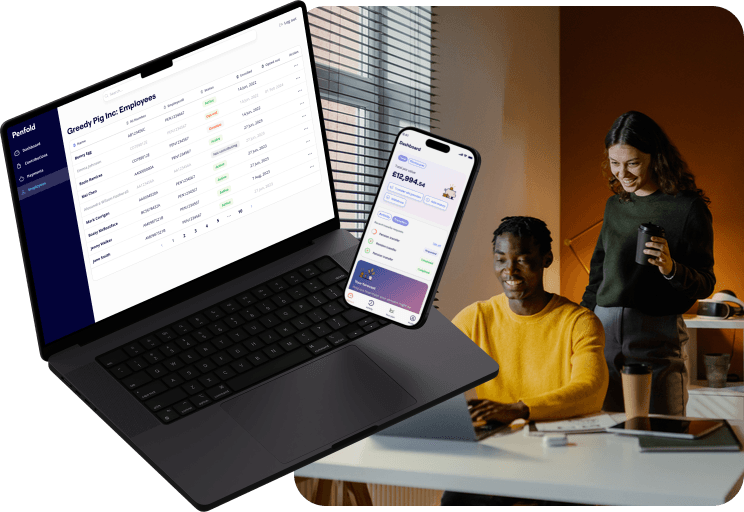

Set up your clients

It’s important to compare providers’ fees and any guaranteed benefits when deciding on whether to transfer, and be sure that the investments available are suitable for you. If your employer is paying into your pension currently, transferring that pot may mean you lose out on their contribution.