Trusted by thousands of UK businesses

From fast-growing startups to established employers, businesses across the UK trust Penfold to manage their workplace pension.

What makes the best workplace pension?

Many workplace pensions offer similar core functionality. The difference is how they support employers and employees day-to-day.

The best workplace pension providers make pensions easier to understand, easier to manage and more valuable for everyone involved.

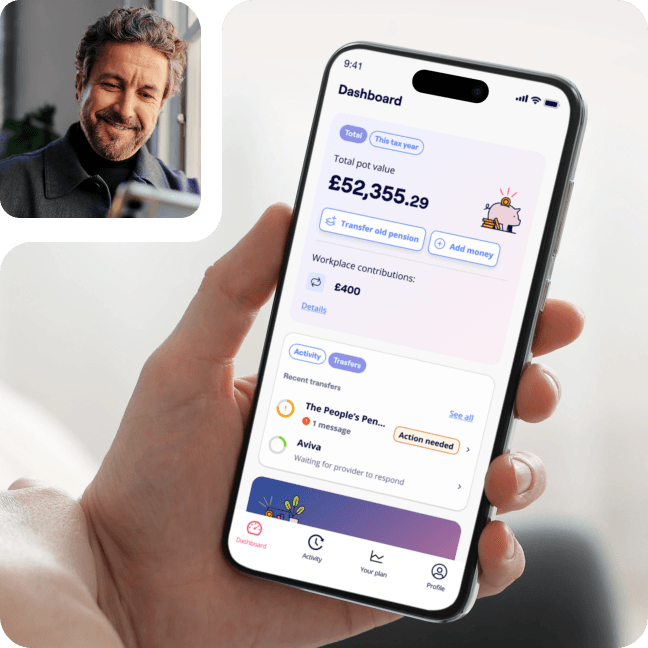

A workplace pension people actually use

Most workplace pensions are ignored.

Penfold is designed to help employees understand, engage with and value their pension.

50%

£1.4 billion

140,000+

Why employers choose Penfold

Employee engagement

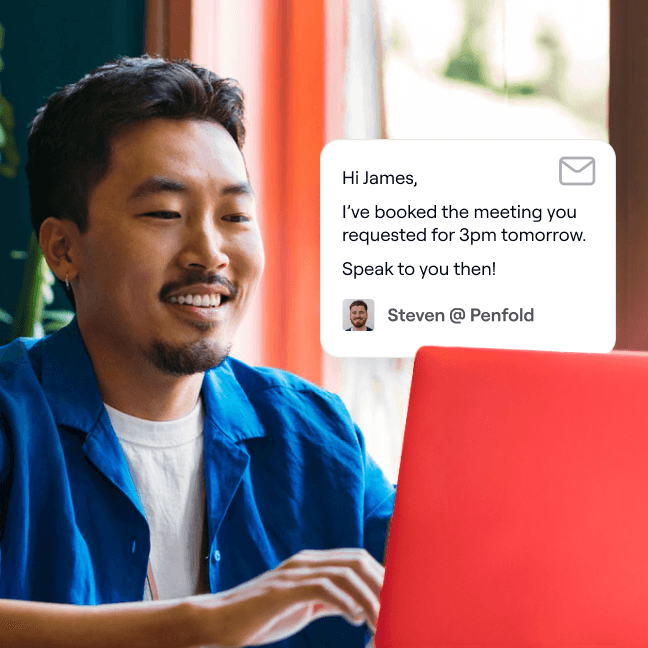

Simple administration

Expert support

Salary sacrifice savings

Investment quality

Easy switching

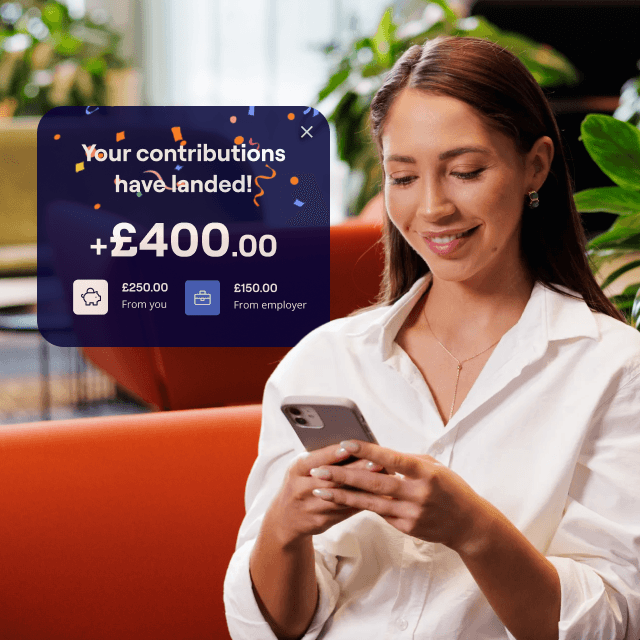

A pension that’s genuinely a benefit

Most workplace pensions are something employees rarely think about.

Penfold helps employees understand what they’ve saved, what it means for their future and what they can do next.

The result is a pension people engage with, rather than ignore.

How does Penfold compare?

Strong investments matter too

While employee engagement, support and ease of administration are often the biggest factors when choosing a workplace pension provider, investment performance remains an important consideration.

Penfold offers carefully selected investment options managed by leading investment managers, with competitive fees and strong long-term performance.

Returns are shown on an annualised basis, based on performance over the past five years to 31 December 2025.

Figures are net of investment fees but gross of provider fees. Past performance, actual or simulated, is also not a reliable indicator of future returns. All investments carry risk and your investment value can go up or down. Returns may increase or decrease as a result of currency fluctuations.

Figures for the Penfold Plan are based on a simulation, provided by BlackRock, of how the portfolio might have performed had these building blocks of the plan existed together over the last five years. It’s important to note that it cannot be definitively said exactly how this plan would have performed in the past. Simulations should not be taken as a guarantee of expected past or future performance, but are designed to be illustrative only. A full list of the assumptions made to generate the simulations is available and should be carefully considered.

The figures shown represent a weighted average of performance across 30 age cohorts (ages 36-65) to provide an overall view of member outcomes. Individual returns will vary depending on fund allocation at different points in a member’s investment journey, as well as personal fee structures. For consistency in comparison, returns have been estimated based on a typical pot size of £10,000 and an average salary of £30,000. Actual returns may differ due to factors such as specific employer-negotiated fees, individual pot sizes, and salary levels.

Returns are based on data collected by investment advisors DWA from a variety of sources, including individual providers and data published on Morningstar. Where possible, actual return data has been used; however, some assumptions were made based on underlying fund data due to availability limitations. The impact of charges has been applied on a monthly basis, which may create minor discrepancies with actual experience depending on the charging structure. DWA is happy to review and correct any discrepancies should further evidence be provided.

Why businesses choose Penfold

Penfold is dramatically better than anything we’ve worked with before and has helped me by removing all of the admin that comes with pensions. ‘Saving time’ is one of the key benefits that encourages me to recommend it to others. Penfold’s been a huge success at Cuvva, with 88% of the company logging into the app to view their pensions.